Getting an offer accepted on a home is extremely exciting. But if you want your home purchase to go smoothly, there’s a lot to do between when you get your offer accepted and when you close on your home.

So the question is, if you’re navigating a home purchase, what, exactly, do you need to do before closing?

A recent article from realtor.com outlined all the checklist items buyers need to get done before closing on a house, including:

Take care of contingencies. If your home sale agreement has any contingencies, you’ll need to get them done before closing (as the name suggests, the sale of the home is contingent on their completion). Make sure you take care of any contingencies (like the home inspection and appraisal) by the deadlines set forth in your agreement, often a few days or weeks after you come to an agreement.

Get your mortgage approved. If you’re buying a home with a mortgage, your loan needs to go through the underwriting process and get approved before you can close on your property. This will also have a due date prior to the closing date. While you only have so much control over how long it takes the lender to approve the loan, make sure you get the mortgage company everything they need to approve it (for example, financial documentation) as quickly as possible.

Do a final walk-through. Before you close on your home, you want to make sure that the property is in the condition you agreed upon (for example, that the sellers made any repairs they agreed upon following the inspection)—so aim to do a final walk-through within 24 hours of the closing.

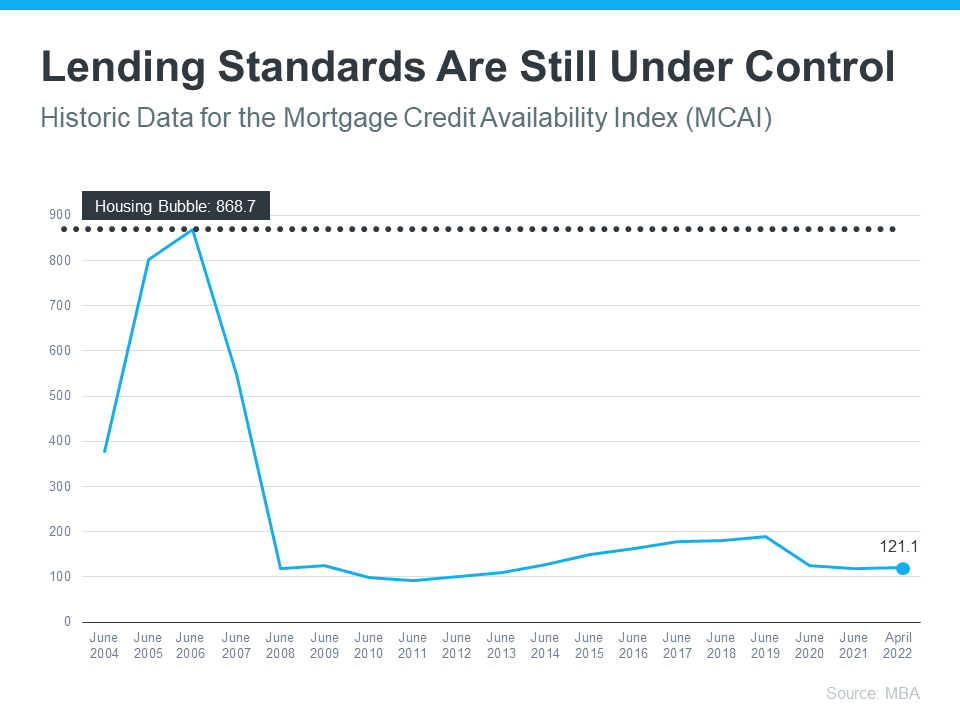

In today’s housing market, many are beginning to wonder if we’re returning to the riskier lending habits and borrowing options that led to the housing crash 15 years ago. Let’s ease those concerns.

Several times a year, the Mortgage Bankers Association (MBA) releases an index titled the Mortgage Credit Availability Index (MCAI). According to their website:

“The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is . . . a summary measure which indicates the availability of mortgage credit at a point in time.”

Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

Why Did the Index Get out of Control During the Housing Bubble?

The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan.

An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICO explains:

“A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.”

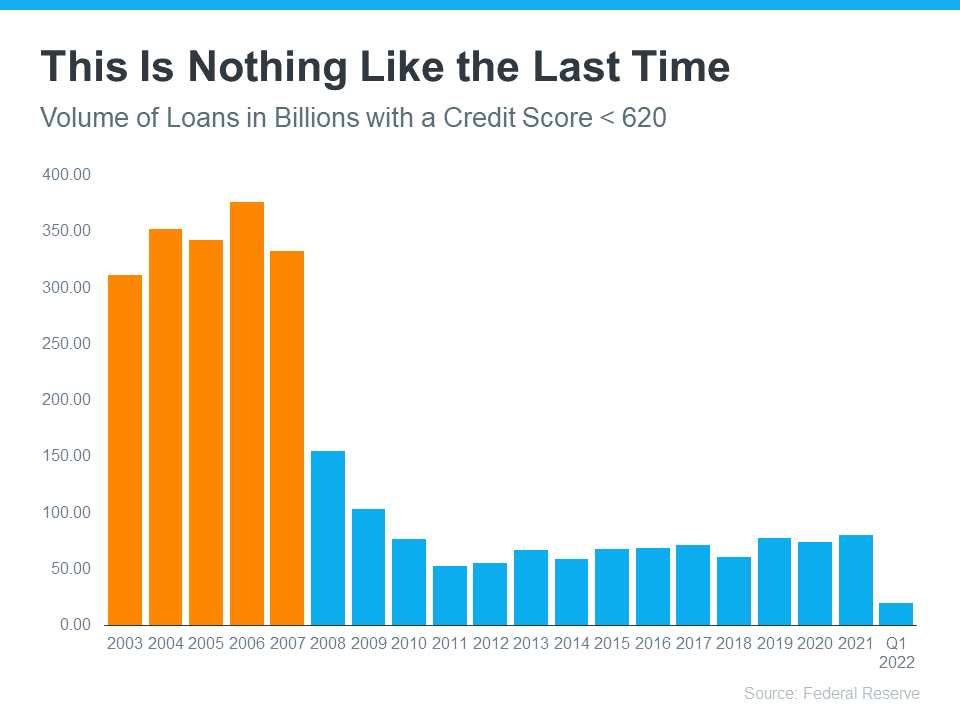

During the housing boom, many mortgages were written for borrowers with a FICO score under 620. While there are still some loan programs that allow for a 620 score, today’s lending standards are much tighter. Lending institutions overall are much more attentive about measuring risk when approving loans. According to the latest Household Debt and Credit Report from the New York Federal Reserve, the median credit score on all mortgage loans originated in the first quarter of 2022 was 776.

The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

Bottom Line

In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, and today is nothing like the last time.

If you’re thinking of buying or selling a house, you’re at an exciting decision point. And anytime you make a big decision like that, one thing you should always consider is timing. So, what does the rest of the year hold for the housing market? Here’s what experts have to say.

The Number of Homes Available for Sale Is Likely To Grow

There are early signs housing inventory is starting to grow and experts say that should continue in the months ahead. According to Danielle Hale, Chief Economist at realtor.com:

“The gap between this year’s homes for sale and last year’s is one-fifth the size that it was at the beginning of the year. The catch up is likely to continue, . . . This growth will mean more options for shoppers than they’ve had in a while, even though inventory continues to lag pre-pandemic normal.”

As a buyer, having more options is welcome news. Just remember, housing supply is still low, so be ready to act fast and put in your best offer up front.

As a seller, your house may soon face more competition when other sellers list their homes. But the good news is, if you’re also buying your next home, having more options to choose from should make that move-up process easier.

Mortgage Rates Will Likely Continue To Respond to Inflationary Pressures

Experts also agree inflation should continue to drive up mortgage rates, albeit more moderately. Odeta Kushi, Deputy Chief Economist at First American, says:

“… ongoing inflationary pressure remains likely to push mortgage rates even higher in the months to come.”

As a buyer, work with trusted real estate professionals, including your lender, so you can learn how rising mortgage rate environments impact your purchasing power. It may make sense to buy now before it costs more to do so, if you’re ready.

As a seller, rising mortgage rates are motivating some homeowners to make a move up sooner rather than later. If you’re planning to buy your next home, talk to a trusted real estate advisor to decide how to time your move.

Home Prices Are Projected To Continue To Climb

Home prices are forecast to keep appreciating because there are still fewer homes for sale than there are buyers in the market. That said, experts agree the pace of that appreciation should moderate – but home prices won’t fall. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Prices throughout the country have surged for the better part of two years, including in the first quarter of 2022. . . Given the extremely low inventory, we’re unlikely to see price declines, but appreciation should slow in the coming months.”

As a buyer, continued home price appreciation means it’ll cost you more to buy the longer you wait. But it also gives you peace of mind that, once you do buy a home, it will likely grow in value. That makes it historically a good investment and a strong hedge against inflation.

As a seller, price appreciation is great news for the value of your home. Again, lean on a professional to strike the right balance of the best conditions possible for both selling your house and buying your next one.

Bottom Line

Whether you’re a homebuyer or seller, you need to know what’s happening in the housing market, so you can make the most informed decision possible. Let’s connect to discuss your goals and what lies ahead, so you can pick your best time to make a move.

Warmer weather and longer days mean summer is almost here. Celebrate by upgrading to the home of your dreams so you can enjoy all the season has to offer.

When you list your house, you can capitalize on today’s sellers’ market to fuel your upgrade. Then, you can move to a home with the features you want, like space to entertain or rooms for work and play.

If you’re ready to upgrade to a home that matches your changing needs, let’s connect.

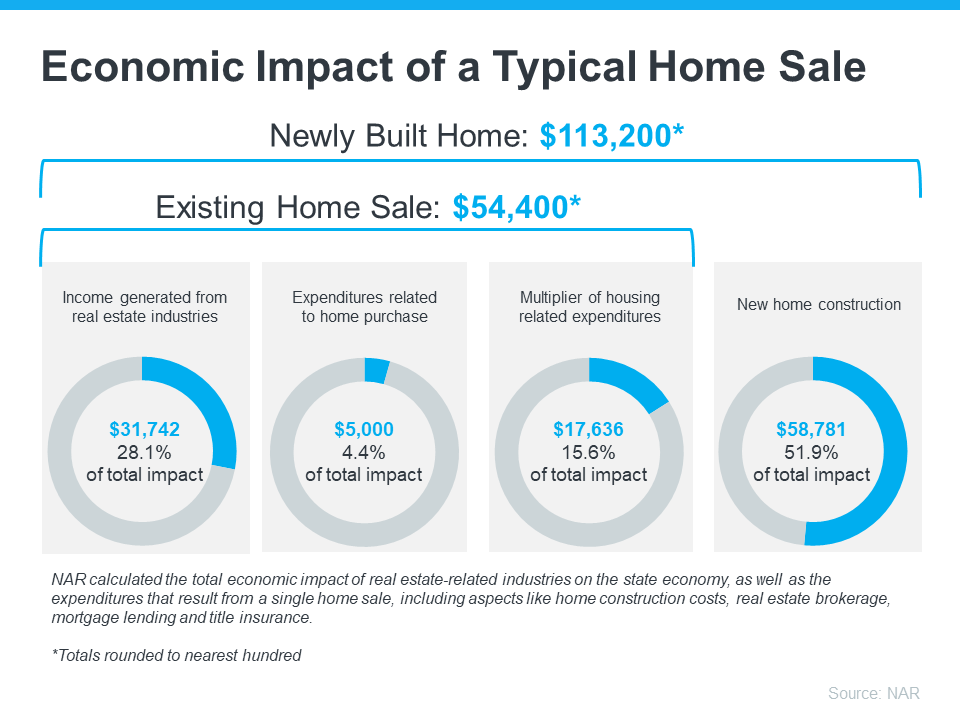

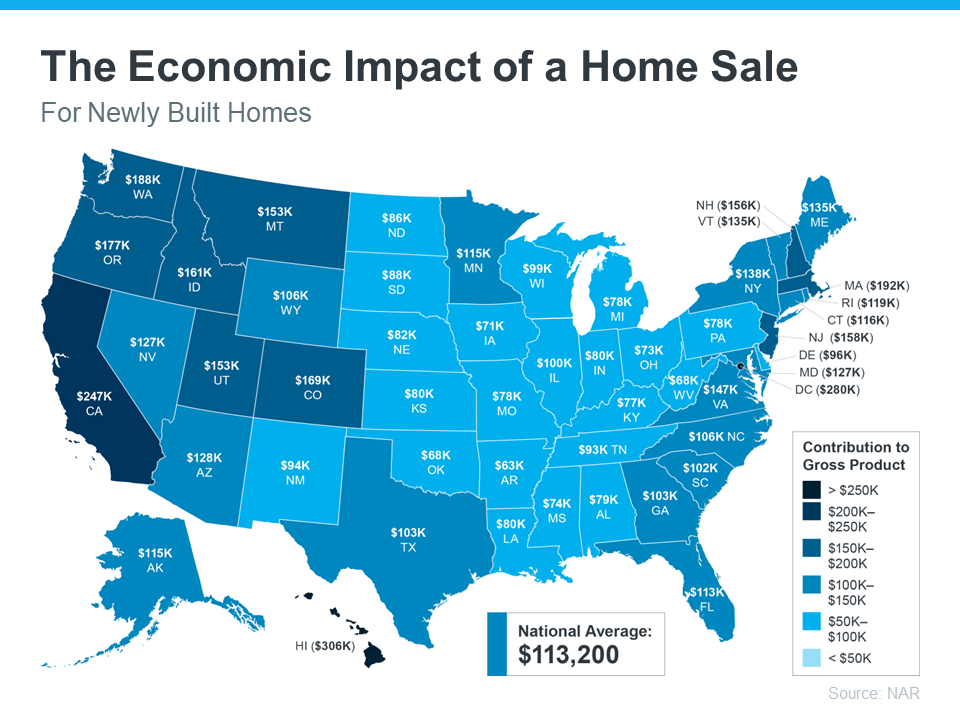

If you’re thinking of buying or selling a home, chances are you’re focusing on the many extraordinary ways it’ll change your life. But do you know it has a large impact on your community too?

To measure that impact, the National Association of Realtors (NAR) releases a report each year to highlight just how much economic activity a home sale generates. The chart below shows how the sale of both a newly built home and an existing home impact the economy:

As the visual shows, a single home sale can have a significant effect on the overall economy. To dive a level deeper, NAR also provides a detailed look at how that varies state-by-state for newly built homes (see map below):

You may be wondering: how can a single home sale have such a major effect on the economy?

For starters, there are multiple industries that play a role in the process. Numerous contractors, specialists, lawyers, town and city officials, and so many other professionals are all necessary at various stages during the transaction. Every individual you work with, like your trusted real estate advisor, has a team of professionals involved behind the scenes.

That means when you buy or sell a home, you’re leaving a lasting impression on the community at large. Let the knowledge that you’re contributing to those around you while also meeting your own needs help you feel even more empowered when you decide to make your move this year.

Bottom Line

Homebuyers and sellers are economic drivers in their community and beyond. Let’s connect so you have a trusted real estate advisor on your side if you’re ready to get started. It won’t just change your life; it’ll make a powerful impact on your entire community.

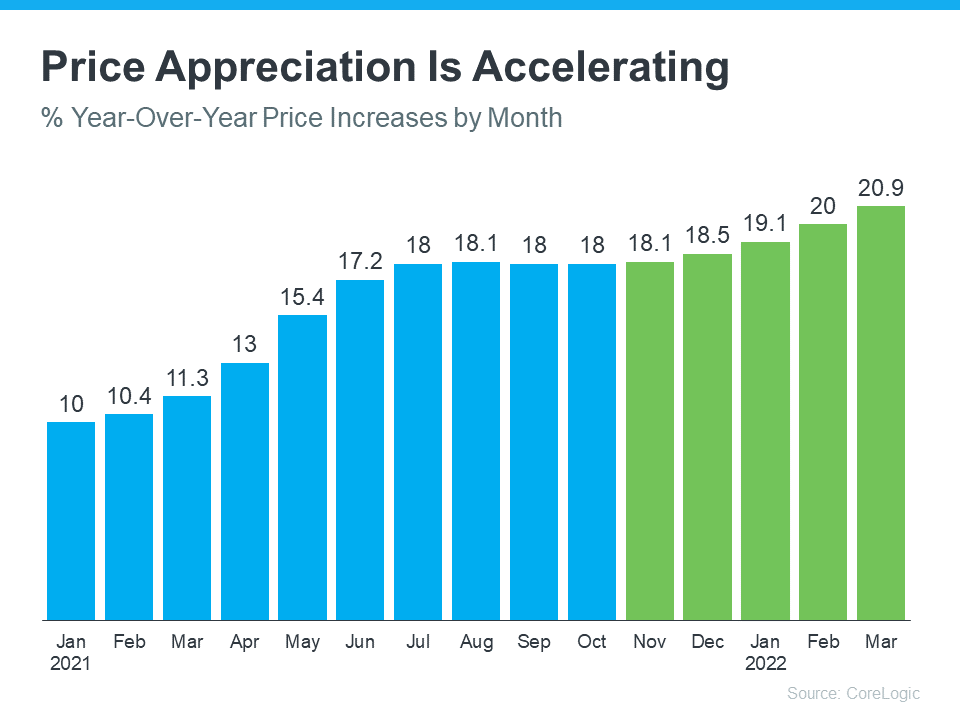

As mortgage rates started to rise this year, many homeowners began to wonder if the value of their homes would fall. Here’s the good news. Historically, when mortgage rates rise by a percentage point or more, home values continue to appreciate. The latest data on home prices seems to confirm that trend.

According to data from CoreLogic, home price appreciation has been re-accelerating since November. The graph below shows this increase in home price appreciation in green:

This is largely due to an ongoing imbalance in supply and demand. Specifically, housing supply is still low, and demand is high. As mortgage rates started to rise this year, many homebuyers rushed to make their purchases before those rates could climb higher. The increased competition drove home prices up even more. Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

“Home price growth continued to gain speed in early spring, as eager buyers tried to get in front of the mortgage rate surge.”

And experts say prices are forecast to continue appreciating, just at a more moderate pace moving forward. A recent article from Fortunesays:

“. . . the swift move up in mortgage rates . . . doesn’t mean home prices are about to crash. In fact, every major real estate firm with a publicly released forecast model . . . still predicts home prices will climb further this year.”

What This Means for You

If you’re thinking about selling your house, you should know you have a great opportunity to list your home and capitalize on today’s home price appreciation. As prices rise, so does the value of your home, which gives your equity a big boost.

When you sell, you can use that equity toward the purchase of your next home. And at today’s record-level of appreciation, that equity may be enough to cover some (if not all) of your down payment.

Bottom Line

History shows rising mortgage rates have not had a negative impact on home prices. Now is still a great time to sell your house thanks to ongoing price appreciation. When you’re ready to find out how much equity you have in your current home and what’s happening with home prices in your local area, let’s connect.

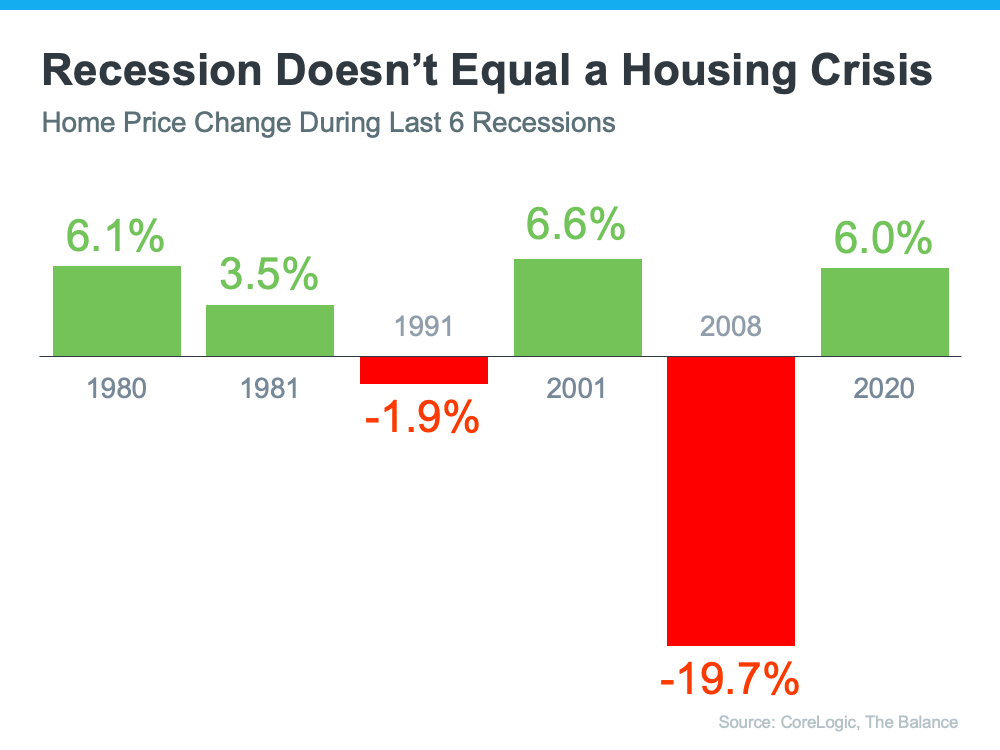

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession, and if true, an economic slowdown doesn’t mean homes will lose value.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

Bottom Line

We’re not in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

If you’re thinking about buying a home, you’ve probably heard mortgage rates are rising and have wondered what that means for you. Since mortgage rates have increased over two percentage points this year, it’s natural to think about how this will impact your homeownership plans.

Today, buyers are reacting in one of two ways: they’re either making the decision to buy now before rates climb higher or they’re waiting it out in hopes rates will fall. Let’s look at some context that can help you understand why so many buyers are jumping off the fence and into action rather than waiting to buy.

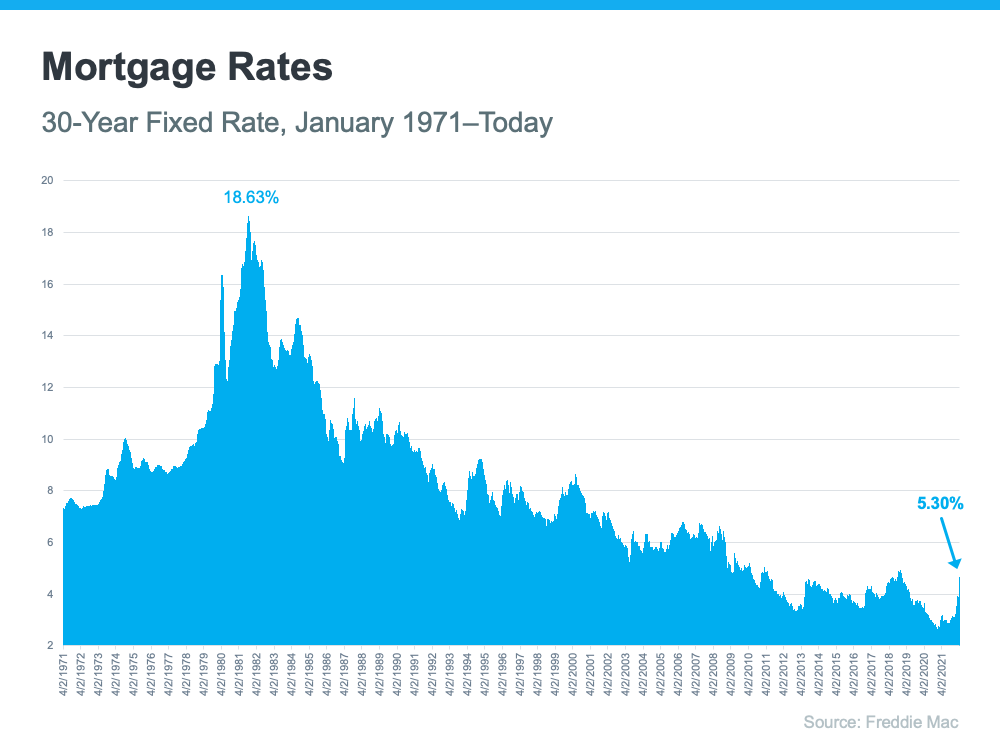

A Look Back: How the Current Mortgage Rate Compares to Historical Data

One factor that could help you make your decision to buy now is how today’s mortgage rates compare to historical data. While higher than the average 30-year fixed rate in recent years, the latest rates are still comparatively low when you look at the bigger picture of where rates have been since 1971 (see graph below):

Mark Fleming, Chief Economist at First American, explains it like this:

“. . . historical context is important. An average 30-year, fixed mortgage rate of 5.5 percent is still well below the historical average of nearly 8 percent.”

If you’re deciding whether to buy now or wait, this is important context to have. Today’s mortgage rate still gives you a window of opportunity to lock in a rate that’s comparatively lower than decades past.

A Look Ahead: What Happens if Rates Climb Further

The buyers who are springing into action now are also motivated to make their move because they know rates have risen steadily this year, and they’re eager to get ahead of any further increases.

Why? When mortgage rates climb, they impact the monthly mortgage payment you’ll have on the home you’re buying. Basically, it’ll likely cost you more to buy a home if you wait. Experts say mortgage rates will rise (although more moderately) in the months ahead. Odeta Kushi, Deputy Chief Economist at First American, explains:

“. . . ongoing inflationary pressure remains likely to push mortgage rates even higher in the months to come.”

So, if you’re ready and financially able to buy now, it may make more sense to get off the fence and make your purchase sooner rather than later. As Nadia Evangelou, Senior Economist at the National Association of Realtors (NAR), says:

“With even higher interest rates on the horizon, I don’t see any reason to hold off from purchasing a home right now. If you feel financially secure, you should start looking for a home.”

At the end of the day, there is no perfect advice on when to buy a home. What you should do depends on your goals, your finances, and your personal situation. Use this information with the help of local real estate professionals to make an informed decision on what’s best for you. The Mortgage Reportssums it up best:

“. . . if you’re on the fence about whether to buy now or wait for a better deal, buying sooner rather than later might be wise. That said, home buying is always a personal decision. Whether you should buy in 2022 depends on your financial situation and the local housing market where you live.”

Bottom Line

For many buyers, rising mortgage rates are motivating them to act now and make a purchase before rates rise higher. To decide what move is best for you, let’s connect so you have expert advice on your side.

In today’s housing market, homeowners have a great opportunity to sell their house and receive the best terms for their personal situation. That’s because there’s a limited number of homes for sale, which is creating competition among buyers. Right now, homebuyers want three things:

These buyer needs give you an amazing advantage – also known as leverage – when you sell.

What Does This Mean for Sellers Today?

You might already realize this enables you to sell at a good price, but you’re also in a great position to get the best terms to suit your needs.

According to the latest Realtors Confidence Index from the National Association of Realtors (NAR), the average home sold is receiving 4.8 offers. That’s why there’s a good chance you’ll get offers from multiple buyers who are willing to compete for your house. When you do, you should look closely at the terms of each offer to find out which one has the best options for you.

And if you have questions at any point in the process, remember your trusted real estate advisor can help. They’re experts who understand the fine print, know how to compare the terms of various offers, and will help you select the best one for your situation.

Bottom Line

If you’re thinking of selling your home, know buyer demand in today’s market gives you a great opportunity to get the best terms and price when you sell your house. Let’s connect today to discuss how much leverage you have as a seller in today’s market.

![Bright Days Are Ahead When You Move Up This Summer INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/26132018/20220527-MEM-1046x1913.png)

![Don’t Let Rising Inflation Delay Your Homeownership Plans INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/18153723/20220520-MEM-1046x2334.png)