In the second half of this year, the housing market surged with activity. Today, real estate experts are looking ahead to the winter season and the forecast is anything but chilly. As Lawrence Yun, Chief Economist for the National Association of Realtors (NAR), notes:

“It will be one of the best winter sales years ever.”

The typical winter slowdown in the housing market is simply not on the radar. Here’s why.

While today’s historically low mortgage rates are expected to remain low, they won’t be this low for much longer. This could be the last chance for homebuyers to secure such low rates, and they’re ready to take action. In a recent article, Bankrate explained:

“If you’re looking to buy a home…expect mortgage rates to remain low into 2021. However, the possibility of rates falling to 2.5 percent or lower has faded as the U.S. economy has rebounded.”

As long as we continue to see low interest rates, we’ll see hopeful buyers on the hunt for their dream homes. Yun confirmed:

“The demand for home buying remains super strong…And we’re still likely to end the year with more homes sold overall in 2020 than in 2019…With persistent low mortgage rates and some degree of a continuing jobs recovery, more contract signings are expected in the near future.”

The challenge, however, is the lack of homes available for sale. With that in mind, all eyes are on homeowners to see if they’ll sell this winter or wait until spring. Danielle Hale, Chief Economist for realtor.com, says it’s best for sellers to capitalize on this moment sooner rather than later:

“We currently see buyers sticking around in the housing market much later than we usually do this fall. If that trend continues, we will see more buyers in the market this winter, too. So, this winter is likely to be a good time to sell.”

With buyers ready to stay active this winter, sellers who want to close a deal on the best possible terms shouldn’t wait until spring to put their homes on the market.

Bottom Line

Experts agree the winter housing market could potentially be bigger than ever. Whether you’re ready to buy or sell, let’s connect today so you can be in your dream home by the new year.

In 2020, buyers got a big boost in the housing market as mortgage rates dropped throughout the year. According to Freddie Mac, rates hit all-time lows 12 times this year, dipping below 3% for the first time ever while making buying a home more and more attractive as the year progressed (See graph below):When you continually hear how rates are hitting record lows, you may be wondering: Are they going to keep falling? Should I wait until they get even lower?

The Challenge with Waiting

The challenge with waiting is that you can easily miss this optimal window of time and then end up paying more in the long run. Last week, mortgage rates ticked up slightly. Sam Khater, Chief Economist at Freddie Mac,explains:

“Mortgage rates jumped this week as a result of positive news about a COVID-19 vaccine. Despite this rise, mortgage rates remain about a percentage point below a year ago.”

While rates are still lower today than they were one year ago, as the economy continues to get stronger and the pandemic is resolved, there’s a very good chance interest rates will rise again. Several top institutions in the real estate industry are projecting an increase in mortgage rates over the next four quarters (See chart below):If you’re planning to wait until next year or later, Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), forecasts mortgage rates will begin to steadily rise:As a buyer, you need to decide if waiting makes financial sense for you.

Bottom Line

If you’re planning to buy a home and want to take advantage of today’s low rates, now is the time to do so. Don’t assume they’re going to stay this low forever.

There seems to be some concern that the 2020 economic downturn will lead to another foreclosure crisis like the one we experienced after the housing crash a little over a decade ago. However, there’s one major difference this time: a robust forbearance program.

During the housing crash of 2006-2008, many felt homeowners should be forced to pay their mortgages despite the economic hardships they were experiencing. There was no empathy for the challenges those households were facing. In a 2009 Wall Street Journal article titled Is Walking Away From Your Mortgage Immoral?, John Courson, Chief Executive of the Mortgage Bankers Association, was asked to comment on those not paying their mortgage. He famously said:

“What about the message they will send to their family and their kids?”

Courson suggested that people unable to pay their mortgage were bad parents.

What resulted from that lack of empathy? Foreclosures mounted.

This time is different. There was an immediate understanding that homeowners were faced with a challenge not of their own making. The government quickly jumped in with a mortgage forbearance program that relieved the financial burden placed on many households. The program allowed many borrowers to suspend their monthly mortgage payments until their economic condition improved. It was the right thing to do.

What happens when forbearance programs expire?

Some analysts are concerned many homeowners will not be able to make up the back payments once their forbearance plans expire. They’re concerned the situation will lead to an onslaught of foreclosures.

The banks and the government learned from the challenges the country experienced during the housing crash. They don’t want a surge of foreclosures again. For that reason, they’ve put in place alternative ways homeowners can pay back the money owed over an extended period of time.

Another major difference is that, unlike 2006-2008, today’s homeowners are sitting on a record amount of equity. That equity will enable them to sell their houses and walk away with cash instead of going through foreclosure.

Bottom Line

The differences mentioned above will be the reason we’ll avert a surge of foreclosures. As Ivy Zelman, a highly respected thought leader for housing and CEO of Zelman & Associates, said:

“The likelihood of us having a foreclosure crisis again is about zero percent.”

Today, on Veterans Day, we honor those who have served our country and thank them for their continued dedication to our nation. In the United States, there are many valuable benefits available to Veterans, including VA home loans. For over 75 years, VA home loans have provided millions of Veterans and their families the opportunity to purchase their own homes.

As we consider the full impact of VA home loans, it’s important to both understand these great options for Veterans and to share them with those we know who may be able to benefit most. For a variety of different reasons, many Veterans don’t use their VA home loan options, so being knowledgeable about what’s available and how they work may be a game-changer for many.

Facts about 2019 VA Home Loans (most current data):

624,546 home loans were guaranteed by the Veterans Administration.

306,879 VA home loans were made without a down payment.

2,055 grants totaling $118 million were provided to help seriously disabled Veterans purchase, modify, or construct a home to meet their needs.

No down payment options as long as the sales price isn’t higher than the home’s appraised value.

Better terms and interest ratesthan loans from other lenders.

Fewer closing costs, which may be paid by the seller.

Bottom Line

The best thing you can do today to celebrate Veterans Day is to share this information with those who can potentially benefit from these loan options. Let’s connect today to discuss your questions about VA home loan benefits. Thank you for your service.

As the current forbearance mortgage relief options come to an end, many are wondering if we’ll face a foreclosure crisis next year. This is understandable, especially for those who remember the housing crisis that began in 2008. The reality is, plans have been put in place through forbearance to ensure history doesn’t repeat itself.

This year, homeowners are able to request 180 days of mortgage relief through forbearance. Upon expiration of that timeframe, they’re also entitled to request 180 additional days, bringing the total to 360 days of deferred payment eligibility. As forbearance expires, homeowners should stay in touch with their lender, because creating a plan for the deferred payments is a critical next step to avoiding foreclosure. There are multiple options for homeowners to pursue at this point, and with the right planning and communication with the lender, foreclosure doesn’t have to be one of them.

Many homeowners are concerned that they’ll have to pay the deferred payments back in a lump sum payment at the end of forbearance. Thankfully, that’s not the case. Fannie Mae explains:

“You don’t have to repay the forbearance amount all at once upon completion of your forbearance plan…Here’s the important thing to remember: If you receive a forbearance plan, you will have options when it comes to repaying the missed amount. You don’t have to pay the forbearance amount at once unless you are able to do so.”

When looking at the percentage of people in forbearance, we can also see that this number has been decreasing steadily throughout the year. Fewer people than initially expected are still in forbearance, so the number of homeowners who will need to work out alternative payment options is declining (See graph below):This means there are fewer and fewer homeowners at risk of foreclosure, and many who initially applied for forbearance didn’t end up needing it. Mike Fratantoni, Senior Vice President and Chief Economist at the Mortgage Bankers Association (MBA), explains:

“Nearly two-thirds of borrowers who exited forbearance remained current on their payments, repaid their forborne payments, or moved into a payment deferral plan. All of these borrowers have been able to resume – or continue – their pre-pandemic monthly payments.”

For those who are still in forbearance and unable to make their payments, foreclosure isn’t the only option left. In their Homeowner Equity Insights Report, CoreLogic indicates:

“In the second quarter of 2020, the average homeowner gained approximately $9,800 in equity during the past year.”

Many homeowners have enough equity in their homes today to be able to sell their houses instead of foreclosing. Selling and protecting the overall financial investment may be a very solid option for many homeowners. As Ivy Zelman, Founder of Zelman & Associates, mentioned in a recent podcast:

“The likelihood of us having a foreclosure crisis again is about zero percent.”

Bottom Line

If you’re currently in forbearance or think you should be because you’re concerned about being able to make your mortgage payments, reach out to your lender to discuss your options and next steps. Having a trusted and knowledgeable professional on your side to guide you is essential in this process and might be the driving factor that helps you stay in your home.

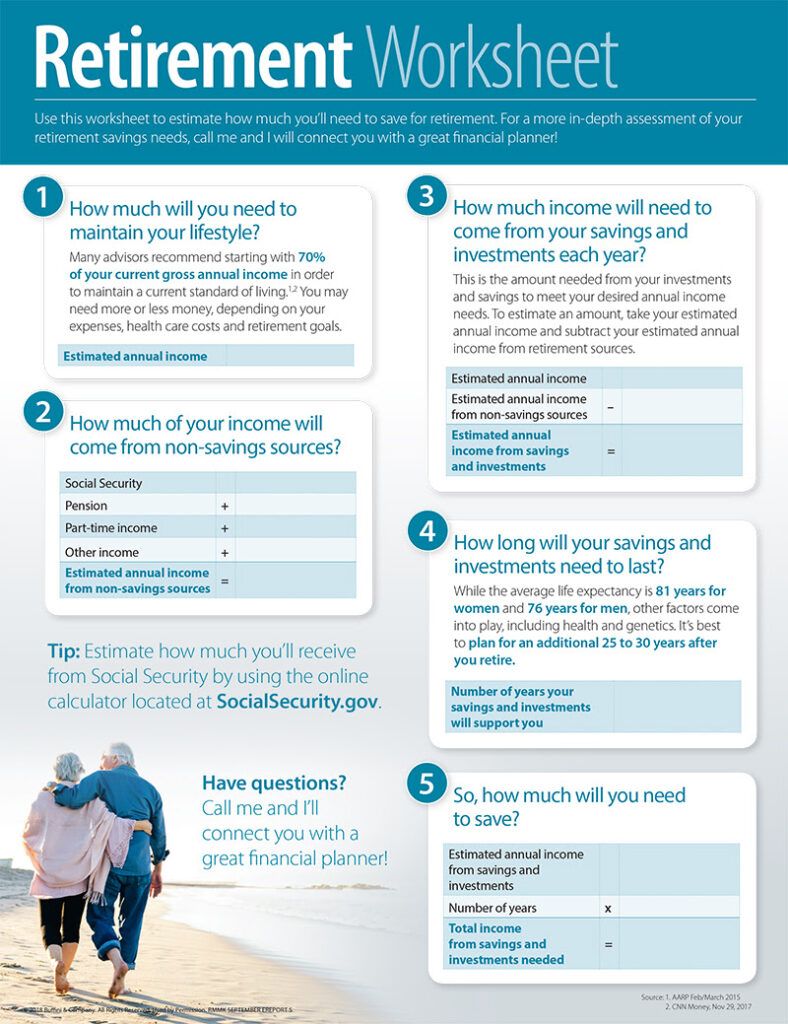

Want to know how much money you need to retire? Use the worksheet below to help you estimate. Although life circumstances may change, the worksheet can give you an idea of how much savings and investments you need to retire comfortably. If you’d like to speak to someone about financial planning, I can connect you with a professional in my network.

That small balance you keep on your credit card? Not helping at all

Forty percent of us think our credit score will climb if we carry a small balance (nope), and 52% don’t realize bad credit can increase the amount needed for deposits on utilities (it does!), according to a NerdWallet survey.

“There are quite a few myths and misinformation about credit scores,” says Ryan Greeley, author of the “Better Credit Blog.” “This stuff isn’t taught anywhere, so it’s something you have to dig into yourself.” The worst time to find out you’ve got a going-nowhere credit score is when you’re trying to buy a home.

Unless you have us to dig for you, that is. Here are seven top credit score myths, and the reality behind them.

Myth #1: Always carry a small balance on your credit card. Reality: The credit score gods want to know two main things: that you pay your bills on time, and that you don’t constantly max out the credit you have. And yes, one of the items they like to see you pay is your credit card bill — all of it. The only thing a running balance increases is the interest you owe. That’s why Erin Lowry, who writes the “Broke Millennial” blog, believes banks and credit card companies probably perpetuated this myth to boost their profits.

Myth #2: It’s OK to pay credit cards a day late if you pay them off in full. Reality: ”Missing a payment is the biggest way to hit your credit score,” Lowry says. “If you pay a student loan a day late, your score can go down as much as 100 points.” So much for that degree making you smarter. To maximize your score, always pay your installment loans (like car loans and mortgages) on time and in full. You know, like you’re supposed to. But also note that actual humans work for financial companies; if you need to pay late for a legit reason, call your lender — before the due date — and have a frank conversation. They’ll often help out.

Myth #3: Closing old cards will erase any negative history. Reality: If it was that easy, we’d all be driving Teslas. Credit-reporting companies keep information on your file for seven years, no matter what. And actually, the longer you’ve responsibly used a particular credit card, the better effect it has on your credit score. Remember, you’re judged by how much of your credit you’re using. Closing a credit card makes that percentage change for the worse.

Hand sketching Myths or Facts concept with white chalk on blackboard.

Myth #4: If you’ve never had credit, you have a perfect credit score. Reality: There’s no reason to save your credit virginity for that special something. If you’ve never used credit, it’s anyone’s guess how well you’ll handle it once you do. Credit reporting agencies call it a “thin file,” meaning there’s not enough information on you to create a credit score. So if you’re a newbie, get an itty-bitty card or loan, and starting fattening up that file.

Myth #5: Checking your credit score frequently will hurt your score. Reality: How else are you supposed to keep track of the darn thing? It’s true that several “hard” checks by companies can ding your score a few points. Hard checks generally happen when you are actually seeking a loan or line of credit, such as a mortgage or credit card.

If you check your own, it’s called a “soft” check, and it doesn’t hurt your score. So for Pete’s sake, check your score and credit report at least annually. It’s super easy these days, especially with websites like creditkarma.com, or use a banking app that lets you easily monitor your score. A sudden, unexplained dip could be a sign that identity theft or mistakes are hurting your credit (and keep hard checks to one or two a year).

Myth #6: Paying off a student loan or car loan early will hurt your credit. Reality: Ah, no. Credit report companies definitely do not punish you for paying off loans early. They might even throw you a parade. (Not really. Put away your princess wave.) While responsibly paying installment loans may be good, paying off those loans is way better.

Myth #7: Your age, sex, and other non-money issues affect your credit score. Reality: What century is it again? Federal law protects you from credit discrimination based on non-credit issues, like race, color, national origin, or sex. Sure, credit card companies or lenders can ask, but they can’t deny you credit based on your answers. Income, expenses, debts, and credit history are what matters.

Myth #8: My credit score can hurt/help my chances of landing a job.Reality: Actually, this one is partially true, depending on how fancy your job is. If it requires a security clearance or using a company credit card, an employer will want to know how you use credit, or if you’re in a financial mess that may make you bribe-able, Lowry says. But don’t worry, the employer will ask your permission before pulling your credit report, which is considered a soft pull and won’t hurt your score.

Buying a home is, for many people, an essential part of the American dream. But for people with a checkered financial history – and a less-than-perfect credit score – it can feel like a dream that’s out of their reach.

But just because you don’t have a perfect credit score or a pristine financial background doesn’t mean you can’t buy a home! While it may be a bit more challenging, you can find financing and buy the home of your dreams even if your credit score isn’t quite up to the level you’d like it to be.

Here are five tips for buying a house (even if you have a less-than-perfect credit score):

1. Make Sure Your Credit Report Is Accurate If you’re worried your financial past might prevent you from securing a mortgage, the first step is to go through your credit report with a fine-toothed comb to make sure everything is accurate and up-to-date.

Mistakes on credit reports are more common than you think. In fact, in 2016 alone, consumers lodged 43,000 complaints to the Consumer Financial Protection Bureau regarding inaccurate credit reporting, accounting for nearly a quarter of total complaints.

Inaccuracies on your credit report can contribute to a low score – and make it harder to secure a loan. Go through your entire credit report to check for inaccuracies and, if there are any, reach out to the credit agencies to have them removed. Even remove one or two inaccurate negative remarks on your credit score can have a big impact on your score and make it easier for you to secure a mortgage.

2. Pay Your Rent On Time For A Year When offering a loan to someone with a less-than-perfect financial history, lenders want to know you’re responsible and they can count on you to make your payments. And that’s why it’s SO important that you pay your rent – on time – for the entire year prior to applying for your mortgage.

Having a documented history of your rental payments that clearly shows you’ve made your payments on time for at least a year shows your lenders you’re able to pay your living expenses on time. And since you were able to pay your rent responsibly, they’ll be more likely to believe you will also pay your mortgage responsibly.

3. Apply for an FHA Loan The Federal Housing Administration (FHA) can be an excellent resource for potential homebuyers with a less-than-perfect financial history.

An FHA Loan is a mortgage that’s insured by the FHA. FHA Loans have more lenient requirements – these mortgages are available for potential buyers with a credit score of 580+ and at least a 3.5% down payment (500+ with at least a 10% down payment).

If you have some money to put down and are concerned your credit score could be holding you back from securing a mortgage, you’ll definitely want to explore an FHA Loan. Just keep in mind that in addition to your mortgage, you’ll need to pay insurance premiums (since the FHA is insuring your loan in case of default).

4. Find A Co-Signer If there’s any possible way to have a friend or family member with higher credit score and better financial situation, do it.

Having a co-signer can help you avoid all the negative aspects of applying for a loan with less-than-stellar credit, including sky-high interest rates. Over the course of the loan, securing a competitive interest rate can save you thousands to tens of thousands of dollars in interest.

But before you ask someone to cosign your loan, remember: a cosigner is taking legal responsibility for your debt. If you default on your mortgage, the lender can take legal action against both you AND your co-signer. Make sure you’re able to afford the mortgage and can manage the payments before letting someone co-sign your loan.

5. Make A Plan To Refinance If there’s no way to avoid a mortgage with a high-interest rate, it’s ok! Just because you’ve got a high-interest rate now doesn’t mean you’ll have a high-interest rate forever.

If you get stuck with a high-interest rate, make a plan for how you can better your financial situation so you can refinance and get a lower rate in the future. Set a date to refinance and strategize ways you can improve your credit score before then, like lowering your total credit card debt, paying all of your bills on time, or looking into credit consolidation options.

There’s no way around it – the better your credit score and financial history, the better (and less expensive) your mortgage will be. But financial mistakes don’t have to keep you from buying the home of your dreams. With determination, a bit of creativity, and these tips, you’ll be well on your way to buying your home – even if you don’t have a perfect credit score.