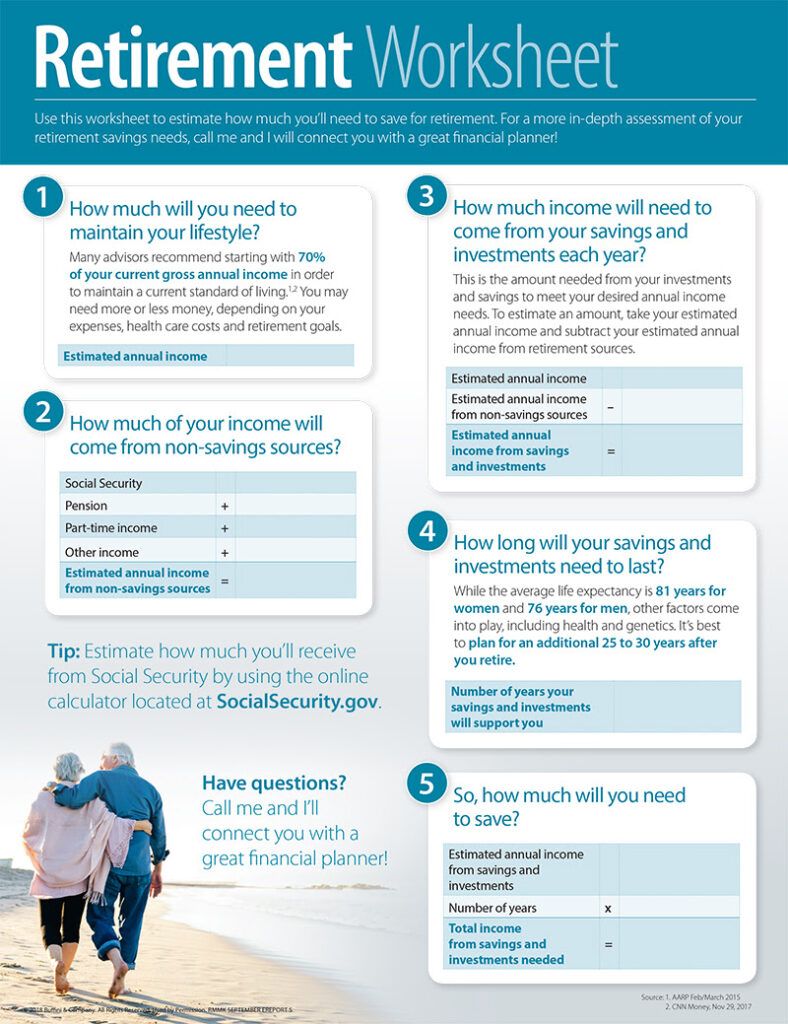

Want to know how much money you need to retire? Use the worksheet below to help you estimate. Although life circumstances may change, the worksheet can give you an idea of how much savings and investments you need to retire comfortably. If you’d like to speak to someone about financial planning, I can connect you with a professional in my network.

On Monday, the National Bureau of Economic Research (NBER) announced that the U.S. economy is officially in a recession. This did not come as a surprise to many, as the Bureau defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

Everyone realizes that the pandemic shut down the country earlier this year, causing a “significant decline in economic activity.”

Though not surprising, headlines announcing the country is in a recession will cause consumers to remember the devastating impact the last recession had on the housing market just over a decade ago.

The real estate market, however, is in a totally different position than it was then. As Mark Fleming, Chief Economist at First American, explained:

“Many still bear scars from the Great Recession and may expect the housing market to follow a similar trajectory in response to the coronavirus outbreak. But, there are distinct differences that indicate the housing market may follow a much different path. While housing led the recession in 2008-2009, this time it may be poised to bring us out of it.”

Four major differences in today’s real estate market are:

We must also realize that a recession does not mean a housing crash will follow. In three of the four previous recessions prior to 2008, home values increased. In the other one, home prices depreciated by only 1.9%.

Bottom Line

Yes, we are now officially in a recession. However, unlike 2008, this time the housing industry is in much better shape to weather the storm.

Because I am from Georgia, I have been hearing about using peach cobbler and vanilla ice cream as a marketing tool (don’t ask me, I don’t get it) for about two months. I’m not going to shove pie down your throat, BUT, these recipes REALLY do look delish. What do you think? Will you make them for your next family feast?

Peach Cobbler6 large fresh peaches, pitted and cut into eighths 1 lemon, zested and juiced Batter: 1/2 cup unsalted butter, at room temperature 1 1/4 cups white sugar 1 1/3 cups self-rising flour 1/3 cup rolled oats 2/3 cup whole milk Glaze: 1/4 cup white sugar 2 tablespoons cold water, or as needed to wet topping sugar Directions 20 m Cook 45 m Ready In 1 h 35 m Preheat oven to 375 degrees F (190 degrees C). Place a baking sheet on the rack under the middle rack to catch drips. Generously butter a 2-inch deep (2-quart) baking dish. Place peach sections into prepared baking dish. Sprinkle with lemon juice and zest. Stir butter and sugar together in a mixing bowl. Mix until creamed and resembles a sugary, buttery paste, 4 to 5 minutes. Add oats and flour; stir until flour and oats are incorporated into the butter-sugar mixture and mixture resembles coarse crumbs, 4 to 5 minutes. Pour in milk; stir until mixture is wet and creamy, like a thick spreadable batter, 3 to 4 minutes. Drop batter by spoonful on top of the peaches. Spread batter evenly over the surface of the peaches. Sprinkle 1/4 cup sugar on the batter. Spritz with water until sugar is wet and surface glistens. Bake in preheated oven on middle rack until browned and crispy, about 45 minutes. Let cool at least 30 minutes before serving.

Footnotes Chef’s Note: If you don’t have a water spritzer, you can use a pastry brush to moisten the sugar topping. Nutrition Facts Per Serving: 371 calories; 12.6 g fat; 62.3 g carbohydrates; 3.3 g protein; 33 mg cholesterol; 279 mg sodium.

‘Nilla Ice Cream Ingredients 1 1/2 cups heavy cream 1 cup whole milk 1/4 cup sugar A pinch of kosher salt 1/2 vanilla bean (or 1 teaspoon vanilla extract) 5 large egg yolks 1/4 cup sugar

Preparation Combine 1 1/2 cups heavy cream, 1 cup whole milk, 1/4 cup sugar, and a pinch of kosher salt in a medium saucepan. Split 1/2 vanilla bean lengthwise and scrape in seeds; add pod (or use 1 teaspoon vanilla extract). Bring mixture just to a simmer, stirring to dissolve sugar. Remove from heat. If using vanilla bean, cover; let sit 30 minutes. Whisk 5 large egg yolks and 1/4 cup sugar in a medium bowl until pale, about 2 minutes. Gradually whisk in 1/2 cup warm cream mixture. Whisk yolk mixture into remaining cream mixture. Cook over medium heat, stirring constantly, until thick enough to coat a wooden spoon, 2-3 minutes. Strain custard into a medium bowl set over a bowl of ice water; let cool, stirring occasionally. Process custard in an ice cream maker according to manufacturer’s instructions. Transfer to an airtight container; cover. Freeze until firm, at least 4 hours and up to 1 week.

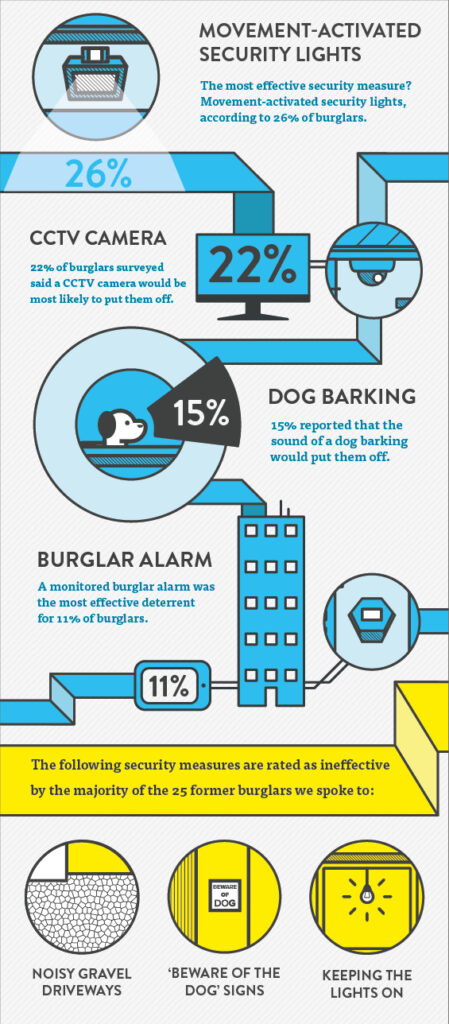

There are many ways that homeowners protect their homes but which safety precautions actually work? To get behind the perspective of a criminal, we interviewed 25 former burglars with help from Unlock – a charity that supports those with criminal convictions rebuilding their lives. We managed to get their opinions on which are the best methods theft deterrents to protect your home and which aren’t effective at preventing theft. It disproves common security misconceptions and the recommendations will hopefully make your homes safer.

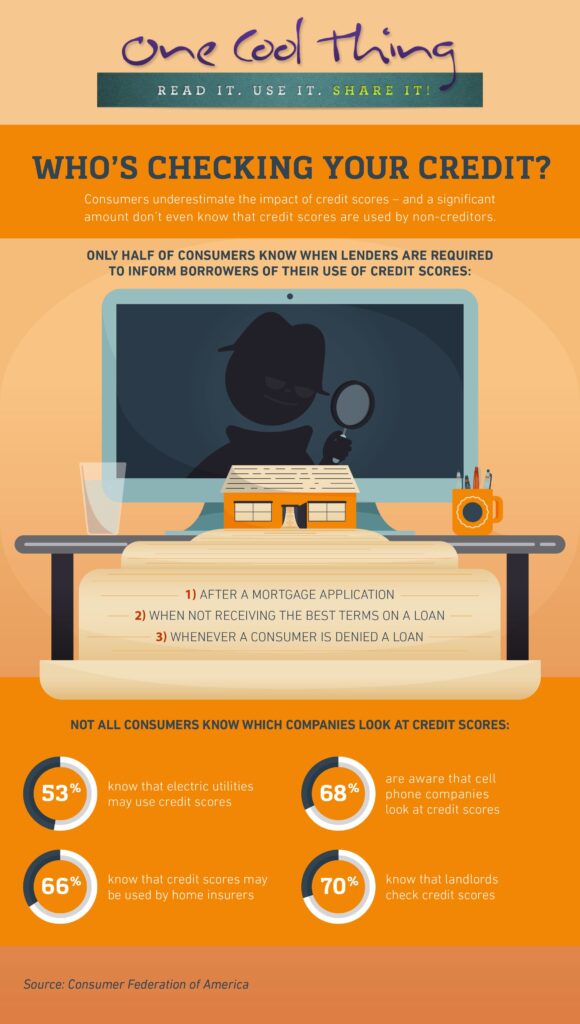

That small balance you keep on your credit card? Not helping at all

Forty percent of us think our credit score will climb if we carry a small balance (nope), and 52% don’t realize bad credit can increase the amount needed for deposits on utilities (it does!), according to a NerdWallet survey.

“There are quite a few myths and misinformation about credit scores,” says Ryan Greeley, author of the “Better Credit Blog.” “This stuff isn’t taught anywhere, so it’s something you have to dig into yourself.” The worst time to find out you’ve got a going-nowhere credit score is when you’re trying to buy a home.

Unless you have us to dig for you, that is. Here are seven top credit score myths, and the reality behind them.

Myth #1: Always carry a small balance on your credit card. Reality: The credit score gods want to know two main things: that you pay your bills on time, and that you don’t constantly max out the credit you have. And yes, one of the items they like to see you pay is your credit card bill — all of it. The only thing a running balance increases is the interest you owe. That’s why Erin Lowry, who writes the “Broke Millennial” blog, believes banks and credit card companies probably perpetuated this myth to boost their profits.

Myth #2: It’s OK to pay credit cards a day late if you pay them off in full. Reality: ”Missing a payment is the biggest way to hit your credit score,” Lowry says. “If you pay a student loan a day late, your score can go down as much as 100 points.” So much for that degree making you smarter. To maximize your score, always pay your installment loans (like car loans and mortgages) on time and in full. You know, like you’re supposed to. But also note that actual humans work for financial companies; if you need to pay late for a legit reason, call your lender — before the due date — and have a frank conversation. They’ll often help out.

Myth #3: Closing old cards will erase any negative history. Reality: If it was that easy, we’d all be driving Teslas. Credit-reporting companies keep information on your file for seven years, no matter what. And actually, the longer you’ve responsibly used a particular credit card, the better effect it has on your credit score. Remember, you’re judged by how much of your credit you’re using. Closing a credit card makes that percentage change for the worse.

Hand sketching Myths or Facts concept with white chalk on blackboard.

Myth #4: If you’ve never had credit, you have a perfect credit score. Reality: There’s no reason to save your credit virginity for that special something. If you’ve never used credit, it’s anyone’s guess how well you’ll handle it once you do. Credit reporting agencies call it a “thin file,” meaning there’s not enough information on you to create a credit score. So if you’re a newbie, get an itty-bitty card or loan, and starting fattening up that file.

Myth #5: Checking your credit score frequently will hurt your score. Reality: How else are you supposed to keep track of the darn thing? It’s true that several “hard” checks by companies can ding your score a few points. Hard checks generally happen when you are actually seeking a loan or line of credit, such as a mortgage or credit card.

If you check your own, it’s called a “soft” check, and it doesn’t hurt your score. So for Pete’s sake, check your score and credit report at least annually. It’s super easy these days, especially with websites like creditkarma.com, or use a banking app that lets you easily monitor your score. A sudden, unexplained dip could be a sign that identity theft or mistakes are hurting your credit (and keep hard checks to one or two a year).

Myth #6: Paying off a student loan or car loan early will hurt your credit. Reality: Ah, no. Credit report companies definitely do not punish you for paying off loans early. They might even throw you a parade. (Not really. Put away your princess wave.) While responsibly paying installment loans may be good, paying off those loans is way better.

Myth #7: Your age, sex, and other non-money issues affect your credit score. Reality: What century is it again? Federal law protects you from credit discrimination based on non-credit issues, like race, color, national origin, or sex. Sure, credit card companies or lenders can ask, but they can’t deny you credit based on your answers. Income, expenses, debts, and credit history are what matters.

Myth #8: My credit score can hurt/help my chances of landing a job.Reality: Actually, this one is partially true, depending on how fancy your job is. If it requires a security clearance or using a company credit card, an employer will want to know how you use credit, or if you’re in a financial mess that may make you bribe-able, Lowry says. But don’t worry, the employer will ask your permission before pulling your credit report, which is considered a soft pull and won’t hurt your score.

The Metro Council took a look around greater Portland and saw two things: Thousands of acres of vacant, developable land, and thousands of units of apartments under construction in Portland. That look combined an analysis by experts and computers showed that the region had enough land within its urban growth boundary to handle 20 years of growth.

Tired of your home looking off-trend and out of touch? Or investing in an older home and want to update it? You don’t need deep pockets to do either. In fact, upgrading your home can be quite affordable with the right projects.

Here are five ways to make a big impact without spending a lot:

Repaint. Paint trends come and go, so if your walls are still the same color or have the same wallpaper from 1950, they’re likely out of date. Consider giving the walls a new look with a more modern tone.

Change light fixtures. It’s time to kick out-of-style light fixtures to the curb. Pendant lighting, Edison bulbs and simple recessed lighting are what’s hot with today’s designers and buyers.

Update your hardware. You’d be surprised at how easily doorknobs, drawer pulls, locks and handles can start to look aged. Take a good look at your existing hardware, and consider upgrading to newer models. And don’t forget the hinges.

Reface your appliances. Have an old, yellowing appliance but don’t want to replace what’s not broken? Just use peel-and-stick stainless steel or marble contact paper, and reface those appliances instantly.

Install a kickplate. If you want to upgrade your curb appeal but can’t afford a new door, consider installing a kickplate. It’s an instant, affordable way to add visual appeal to any existing entryway.

These upgrades may seem minor, but when done properly, they can have a serious impact on your home’s aesthetic.

If you’re considering more extensive updates, let’s get together to discuss ways to increase your home’s marketability and long-term value.