The housing market has gone through a lot of change recently, and much of that was a result of how quickly mortgage rates rose last year.

Continue reading “Experts Forecast a Turnaround in the Housing Market in 2023”

Stuff About Portland, Oregon Real Estate Stuff

The housing market has gone through a lot of change recently, and much of that was a result of how quickly mortgage rates rose last year.

Continue reading “Experts Forecast a Turnaround in the Housing Market in 2023”

If you’re a homeowner ready to make a move, you may be thinking about using your current house as a short-term rental property instead of selling it. A short-term rental (STR) is typically offered as an alternative to a hotel, and they’re an investment that’s gained popularity in recent years. According to a Harris Poll survey, 28% of homeowners have considered using a rental service to temporarily rent out their home for additional income.

Continue reading “Should You Rent Your House or Sell It?”When exploring mortgage options, many potential homebuyers turn to the Federal Housing Administration (FHA) loan program for its accessible credit requirements and low down payment options. FHA loans are particularly popular among first-time homebuyers and individuals with limited financial resources. However, like any financial decision, it’s crucial to be well-informed before committing to an FHA loan. In this article, we’ll highlight several key factors to keep in mind when considering an FHA loan, empowering you to make an informed decision that aligns with your long-term financial goals.

1. FHA Loan Basics

FHA loans were established by the U.S. Department of Housing and Urban Development (HUD) to facilitate homeownership for low to moderate-income borrowers. These loans are insured by the FHA, allowing approved lenders to offer favorable terms and lower interest rates to borrowers with less-than-perfect credit histories. The primary advantage of an FHA loan is its low down payment requirement, often as low as 3.5% of the home’s purchase price, making it an attractive option for buyers with limited savings.

2. Mortgage Insurance Premium (MIP)

One essential aspect of FHA loans is the Mortgage Insurance Premium (MIP). Unlike conventional loans, FHA loans require borrowers to pay both an upfront MIP at closing and an annual MIP over the life of the loan. The upfront MIP is typically 1.75% of the loan amount, while the annual MIP amount varies based on factors such as loan term, loan-to-value ratio, and loan amount. It’s essential to consider these additional costs when evaluating the overall affordability of an FHA loan.

3. Credit Requirements

FHA loans are renowned for their lenient credit requirements, often accommodating borrowers with credit scores as low as 580. However, a lower credit score may result in a higher down payment, potentially up to 10% for individuals with scores between 500 and 579. Although FHA loans provide flexibility, it’s crucial to remember that a higher credit score can still lead to more favorable terms and lower interest rates.

4. Property Eligibility

The property being purchased must meet certain eligibility criteria to qualify for an FHA loan. These requirements are in place to ensure the property’s safety, habitability, and marketability. Properties must be used as primary residences, and certain types of properties, such as fixer-uppers, may require additional inspections and appraisal conditions. Before selecting a property, it is advisable to verify its eligibility to avoid any surprises during the loan application process.

5. Debt-to-Income Ratio

FHA loans consider both your housing expenses and overall debt obligations when determining eligibility. Generally, the debt-to-income (DTI) ratio should not exceed 43%, including the projected mortgage payment. Lenders may have additional overlays, which are stricter requirements on top of FHA guidelines, so it’s essential to check with the lender for specific DTI requirements.

6. Loan Limits

FHA loan limits vary by region and are subject to change annually. These limits determine the maximum loan amount a borrower can obtain with an FHA loan in a specific area. It’s crucial to stay informed about the current loan limits to avoid disappointment if your desired property exceeds the FHA loan cap.

FHA loans offer a viable pathway to homeownership for individuals who may not qualify for conventional loans due to credit or financial constraints. Understanding the key aspects of FHA loans, such as the MIP, credit requirements, property eligibility, DTI ratio, and loan limits, is vital in making an informed decision about this type of mortgage. As with any significant financial commitment, potential borrowers should thoroughly evaluate their financial situation and consider seeking guidance from a qualified mortgage professional to determine if an FHA loan aligns with their homeownership goals. By doing so, aspiring homeowners can embark on their homeownership journey with confidence and clarity.

As mortgage rates rose last year, activity in the housing market slowed down. And as a result, homes started seeing fewer offers and stayed on the market longer. That meant some homeowners decided to press pause on selling.

Now, however, rates are beginning to come down—and buyers are starting to reenter the market. In fact, the latest data from the Mortgage Bankers Association (MBA) shows mortgage applications increased last week by 7% compared to the week before.

So, if you’ve been planning to sell your house but you’re unsure if there will be anyone to buy it, this shift in the market could be your chance. Here’s what experts are saying about buyers returning to the market as we approach spring.

“Mortgage rates are now at their lowest level since September 2022, and about a percentage point below the peak mortgage rate last fall. As we enter the beginning of the spring buying season, lower mortgage rates and more homes on the market will help affordability for first-time homebuyers.”

“The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.”

“We expect the labor market to remain robust, wages to continue to rise—maybe not at the pace that they did during the pandemic, but that will open up some opportunity for folks to enter homeownership as interest rates stabilize a bit.”

“Homebuyers are waiting for rates to decrease more significantly, and when they do, a strong job market and a large demographic tailwind of Millennial renters will provide support to the purchase market.”

If you’ve been thinking about making a move, now’s the time to get your house ready to sell. Let’s connect so you can learn about buyer demand in our area the best time to put your house on the market.

Before you buy a home, it’s important to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home, you need to understand what closing costs are and how much you should budget for.

People are sometimes surprised by closing costs because they don’t know what they are. According to Bankrate:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”

In other words, your closing costs are a collection of fees and payments involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical, too. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $366,900. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $7,500 and $18,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

Work with a team of trusted real estate professionals to understand exactly how much you’ll need to budget for closing costs. An agent can help connect you with a lender, and together your expert team can answer any questions you might have.

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process.

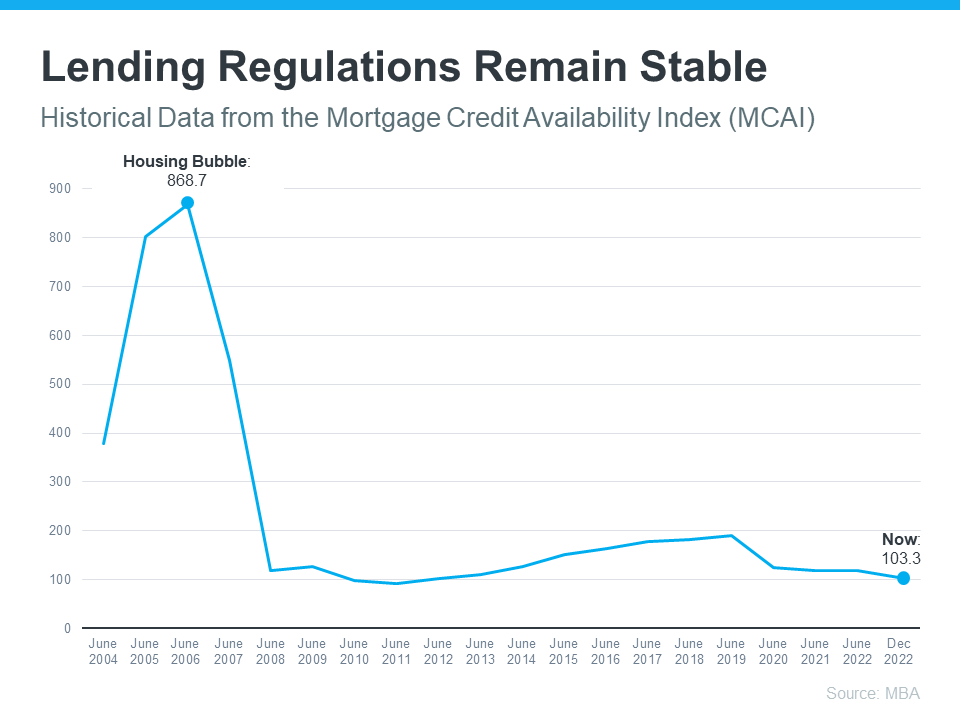

67% of Americans say a housing market crash is imminent in the next three years. With all the talk in the media lately about shifts in the housing market, it makes sense why so many people feel this way. But there’s good news. Current data shows today’s market is nothing like it was before the housing crash in 2008.

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance an existing one.

As a result, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

The graph below uses data from the Mortgage Bankers Association (MBA) to help tell this story. In this index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards have helped prevent a situation that could lead to a wave of foreclosures like the last time.

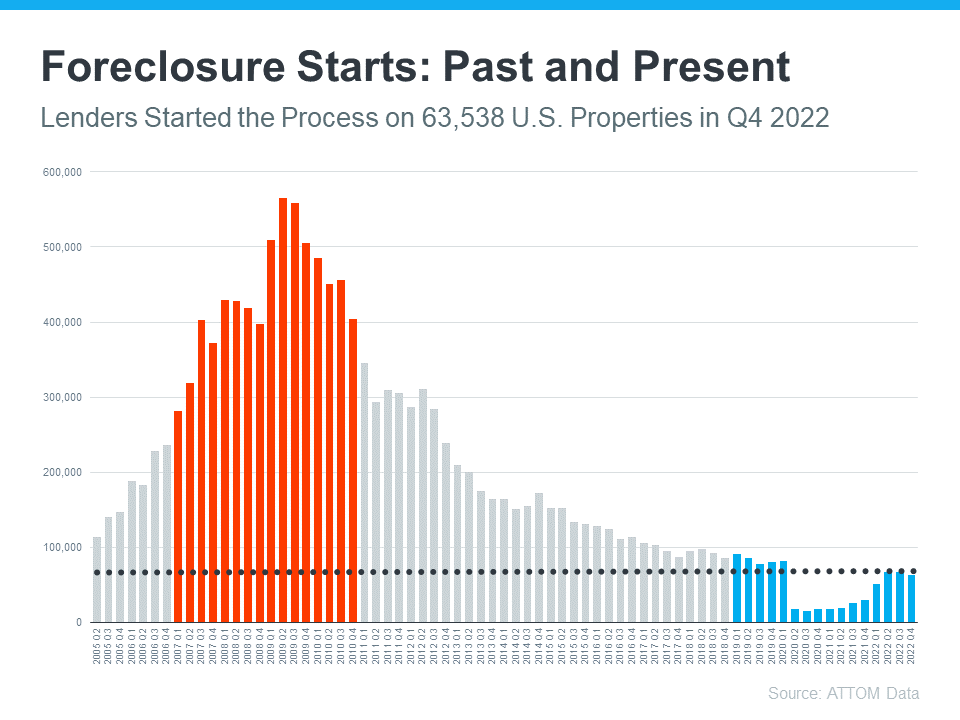

Another difference is the number of homeowners that were facing foreclosure when the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM to show the difference between last time and now:

So even as foreclosures tick up, the total number is still very low. And on top of that, most experts don’t expect foreclosures to go up drastically like they did following the crash in 2008. Bill McBride, Founder of Calculated Risk, explains the impact a large increase in foreclosures had on home prices back then – and how that’s unlikely this time.

“The bottom line is there will be an increase in foreclosures over the next year (from record level lows), but there will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.”

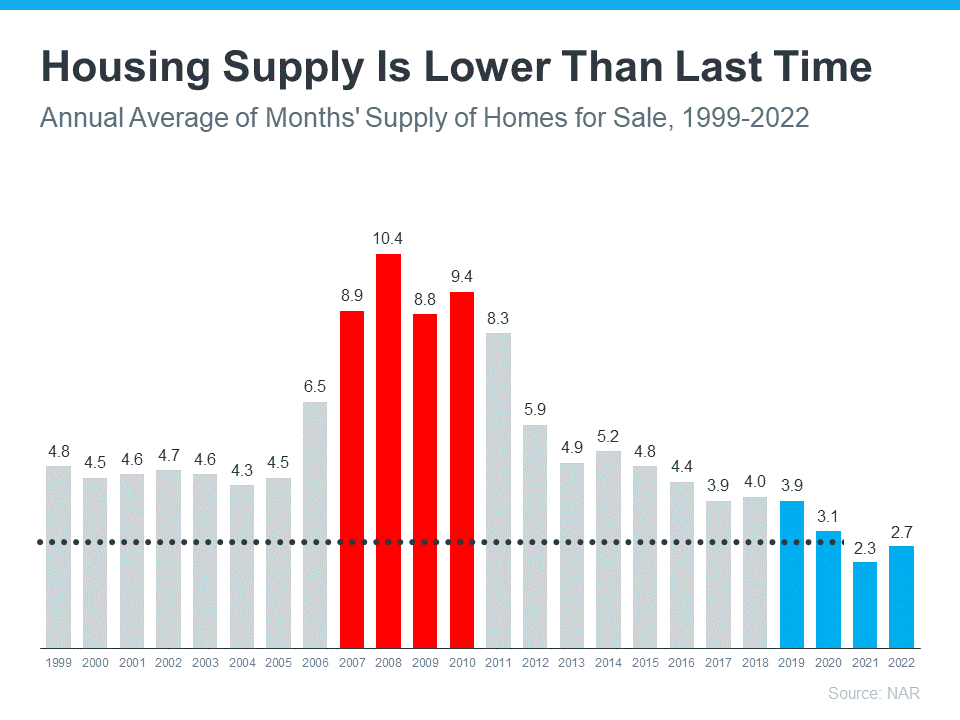

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just 2.7-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

If recent headlines have you worried we’re headed for another housing crash, the data above should help ease those fears. Expert insights and the most current data clearly show that today’s market is nothing like it was last time.

![How To Win as a Buyer in Today’s Housing Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/02/10132146/Resize-UPDATED-MEM_Homeownership-Builds-Your-Wealth-In-The-Over-Time-MEM.png)

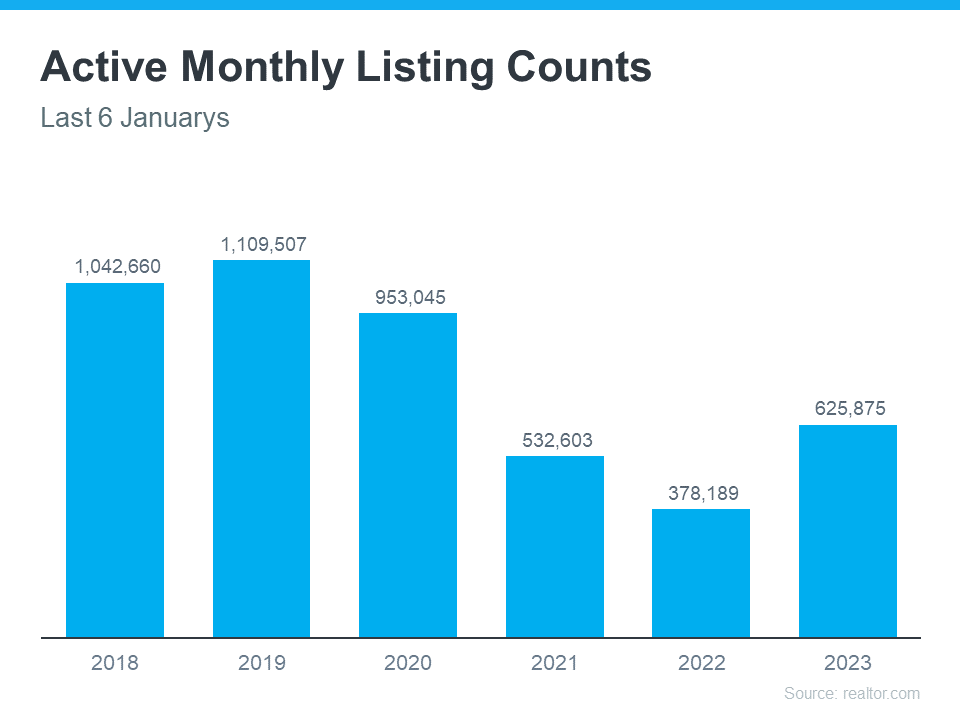

The biggest challenge in the housing market right now, and likely for years to come, is how few homes there are for sale compared to the number of people who want to buy. That’s why, if you’re thinking about selling your house, this is a great time to do so. Your house would be welcome in a market that has fewer homes for sale than it did in the years leading up to the pandemic.

According to the latest Monthly Housing Market Trends Report from realtor.com:

“There were 65.5% more homes for sale in January compared to the same time in 2022. This means that there were 248,000 more homes available to buy this past month compared to one year ago. While the number of homes for sale is increasing, it is still 43.2% lower than it was before the pandemic in 2017 to 2019. This means that there are still fewer homes available to buy on a typical day than there were a few years ago.”

The graph below shows how today’s inventory of homes for sale compares to recent years:

Fewer homes for sale means buyers have fewer choices than they did prior to the pandemic—and that frustration is leading some to give up on the homebuying process altogether. But with mortgage rates sitting lower than they were at the peak last fall, more buyers are willing to come back into the process—they just need to find homes to buy. This is welcome activity for the spring market, especially if you’re thinking of selling your house.

With a renewed interest in buying a home for many, the New York Times (NYT) reports:

“Home buyers are edging back into the market after being sidelined last year . . .”

So, if you want to take advantage of a sweet spot in the market, this spring could be your shot.

The housing market needs more homes for sale to meet the demand of today’s buyers. If you’ve thought about selling, now’s the time for us to connect and get ready for you to make a move this spring.

Many of today’s homeowners bought or refinanced their homes during the pandemic when mortgage rates were at history-making lows. Since rates doubled in 2022, some of those homeowners put their plans to move on hold, not wanting to lose the low mortgage rate they have on their current house. And while today’s rates have started coming down from last year’s peak, they’re still higher than they were a couple of years ago.

Today, 93% of outstanding mortgages have a rate at or below 6%. That means a strong majority of homeowners with mortgages have a rate below what they’d get if they moved right now. But if you’re a homeowner in that position, remember that mortgage rates aren’t the only thing to consider when making a move. Your mortgage rate is important, but there are plenty of reasons you may still need or want to move. RealTrends explains:

“Sellers who don’t have to move won’t be moving. The most common sellers will be: Homeowners downsizing . . . people moving to get more space, [households] looking for better schools…etc.”

So, if you’re on the fence about selling your house, consider the other reasons homeowners are choosing to make a move. A recent report from the National Association of Realtors (NAR) breaks down why homeowners have decided to sell over the past year:

As the visual shows, the most commonly cited reasons for selling were the desire to move closer to loved ones, followed by moving due to retirement, and their neighborhood becoming less desirable. Additionally, the need for more space factored in, as did a change in household structure.

If you also find yourself wanting a change in location or needing space your current house just can’t provide, it may be time to sell.

What you want and need in a home can be reason enough to move. To find out what’s right for you, work with a trusted real estate professional who will offer advice and expert guidance throughout the process. They’ll be able to lay out all your options – giving you what you need to make a confident decision.

When deciding whether or not to move, you have a lot to consider. There are plenty of non-financial reasons to factor in. Let’s connect today to weigh the benefits of selling your house.

![You May Not Need as Much as You Think for Your Down Payment [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/02/01164441/You-May-Not-Need-As-Much-As-You-Think-For-Your-Down-Payment-MEM-1046x1917.png)