Media coverage about what’s happening with home prices can be confusing. A large part of that is due to the type of data being used and what they’re choosing to draw attention to. For home prices, there are two different methods used to compare home prices over different time periods: year-over-year (Y-O-Y) and month-over-month (M-O-M). Here’s an explanation of each.

Year-over-Year (Y-O-Y):

This comparison measures the change in home prices from the same month or quarter in the previous year. For example, if you’re comparing Y-O-Y home prices for April 2023, you would compare them to the home prices for April 2022.

Y-O-Y comparisons focus on changes over a one-year period, providing a more comprehensive view of long-term trends. They are usually useful for evaluating annual growth rates and determining if the market is generally appreciating or depreciating.

Month-over-Month (M-O-M):

This comparison measures the change in home prices from one month to the next. For instance, if you’re comparing M-O-M home prices for April 2023, you would compare them to the home prices for March 2023.

Meanwhile, M-O-M comparisons analyze changes within a single month, giving a more immediate snapshot of short-term movements and price fluctuations. They are often used to track immediate shifts in demand and supply, seasonal trends, or the impact of specific events on the housing market.

The key difference between Y-O-Y and M-O-M comparisons lies in the time frame being assessed. Both approaches have their own merits and serve different purposes depending on the specific analysis required.

Why Is This Distinction So Important Right Now?

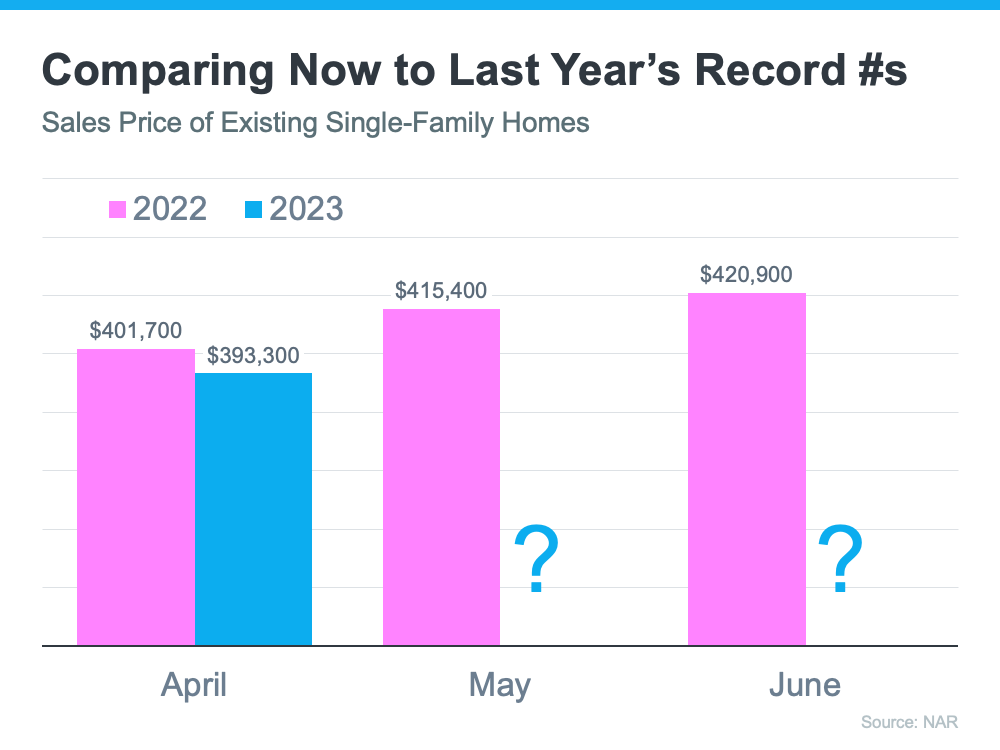

We’re about to enter a few months when home prices could possibly be lower than they were the same month last year. April, May, and June of 2022 were three of the best months for home prices in the history of the American housing market. Those same months this year might not measure up. That means, the Y-O-Y comparison will probably show values are depreciating. The numbers for April seem to suggest that’s what we’ll see in the months ahead (see graph below):

That’ll generate troubling headlines that say home values are falling. That’ll be accurate on a Y-O-Y basis. And, those headlines will lead many consumers to believe that home values are currently cascading downward.

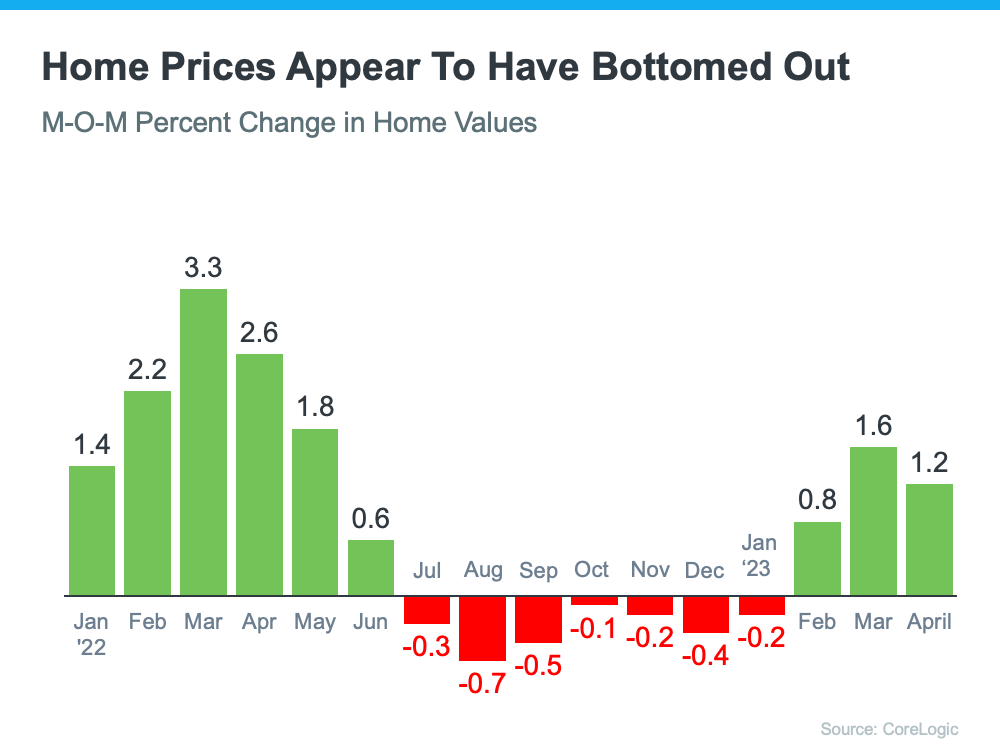

However, on a closer look at M-O-M home prices, we can see prices have actually been appreciating for the last several months. Those M-O-M numbers more accurately reflect what’s truly happening with home values: after several months of depreciation, it appears we’ve hit bottom and are bouncing back.

Here’s an example of M-O-M home price movements for the last 16 months from the CoreLogic Home Price Insightsreport (see graph below):

Why Does This Matter to You?

So, if you’re hearing negative headlines about home prices, remember they may not be painting the full picture. For the next few months, we’ll be comparing prices to last year’s record peak, and that may make the Y-O-Y comparison feel more negative. But, if we look at the more immediate, M-O-M trends, we can see home prices are actually on the way back up.

There’s an advantage to buying a home now. You’ll buy at a discount from last year’s price and before prices start to pick up even more momentum. It’s called “buying at the bottom,” and that’s a good thing.

Bottom Line

If you have questions about what’s happening with home prices, or if you’re ready to buy before prices climb higher, let’s connect.

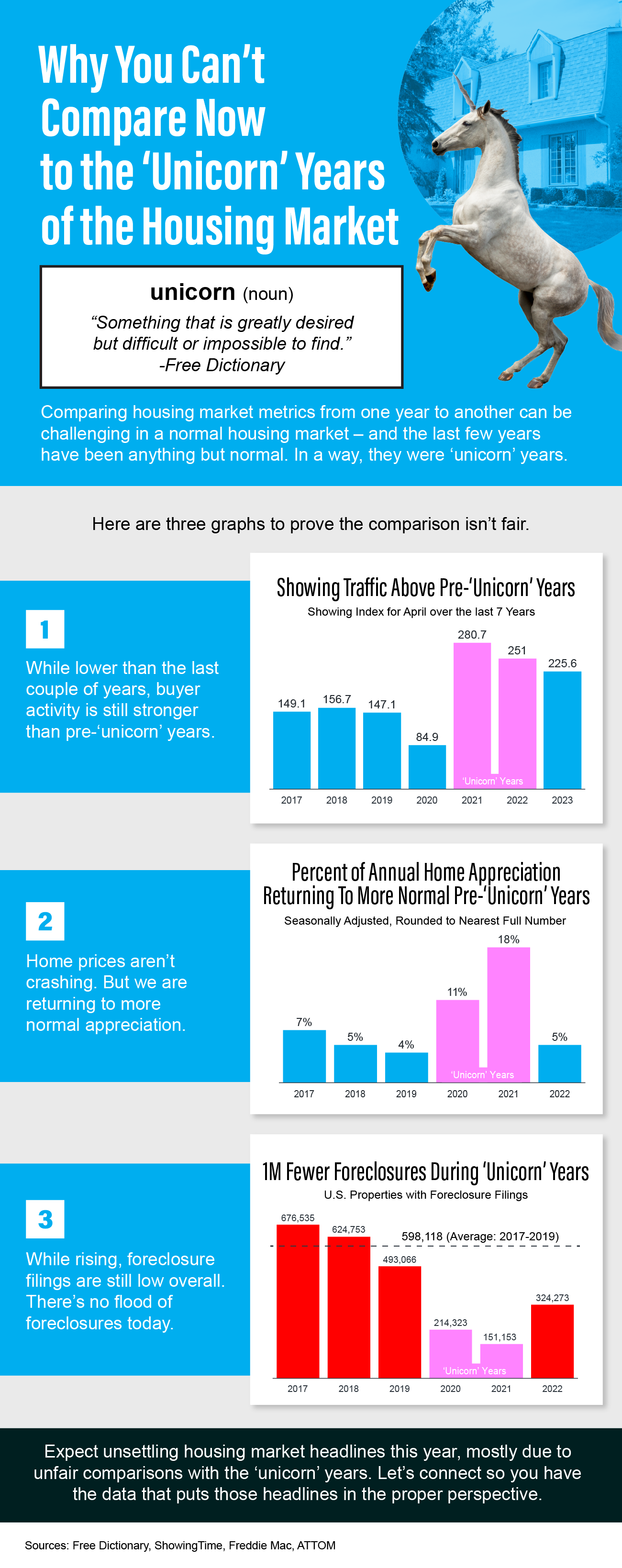

Comparing housing market metrics from one year to another can be challenging in a normal housing market – and the last few years have been anything but normal. In a way, they were ‘unicorn’ years.

When you look at the numbers today, the one thing that stands out is the strength of this housing market. We can see this is one of the most foundationally strong housing markets of our lifetime – if not the strongest housing market of our lifetime. Here are two fundamentals that prove this point.

1. The Current Mortgage Rate on Existing Mortgages

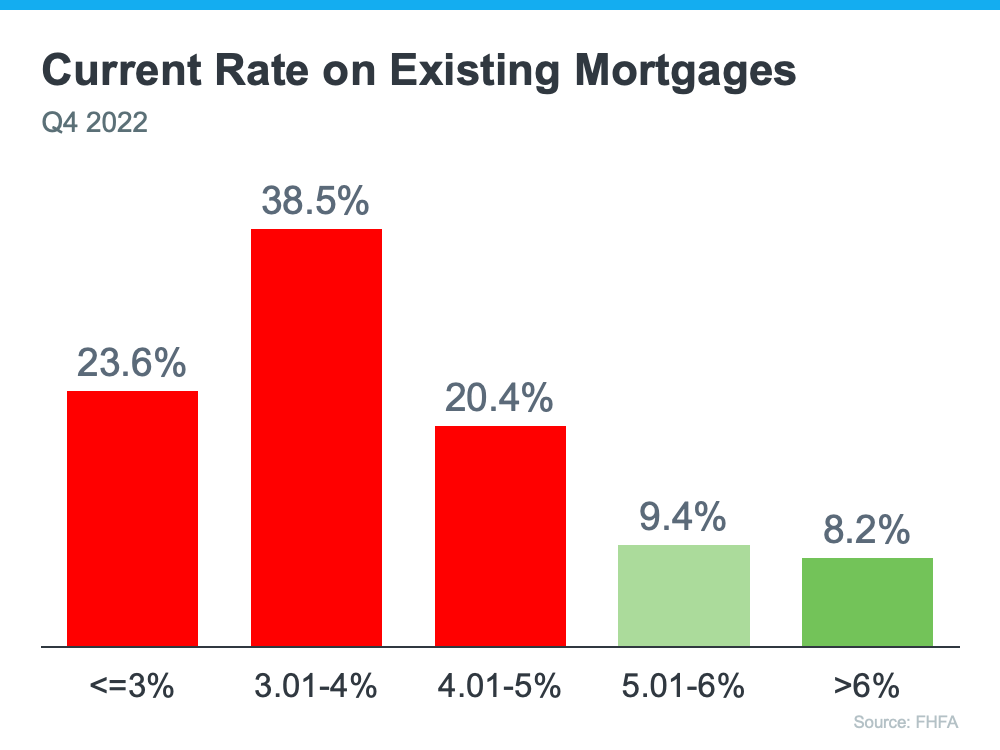

First, let’s look at the current rate on existing mortgages. According to the Federal Housing Finance Agency (FHFA), as of the fourth quarter of last year, over 80% of existing mortgages have a rate below 5%. That’s significant. And, to take that one step further, over 50% of mortgages have a rate below 4% (see graph below):

Now, there’s a lot of talk in the media about a potential foreclosure crisis or a rise of homeowners defaulting on their loans, but consider this. Homeowners with such good mortgage rates are going to work as hard as they can to keep that mortgage and stay in their homes. That’s because they can’t go out and buy another house, or even rent an apartment, and pay what they do today. Their current mortgage payment is more affordable. Even if they downsize, with today’s higher mortgage rates, it could cost more.

Here’s why this gives the housing market such a solid foundation today. Having so many homeowners with such low mortgage rates helps us avoid a crisis with a flood of foreclosures coming to market like there was back in 2008.

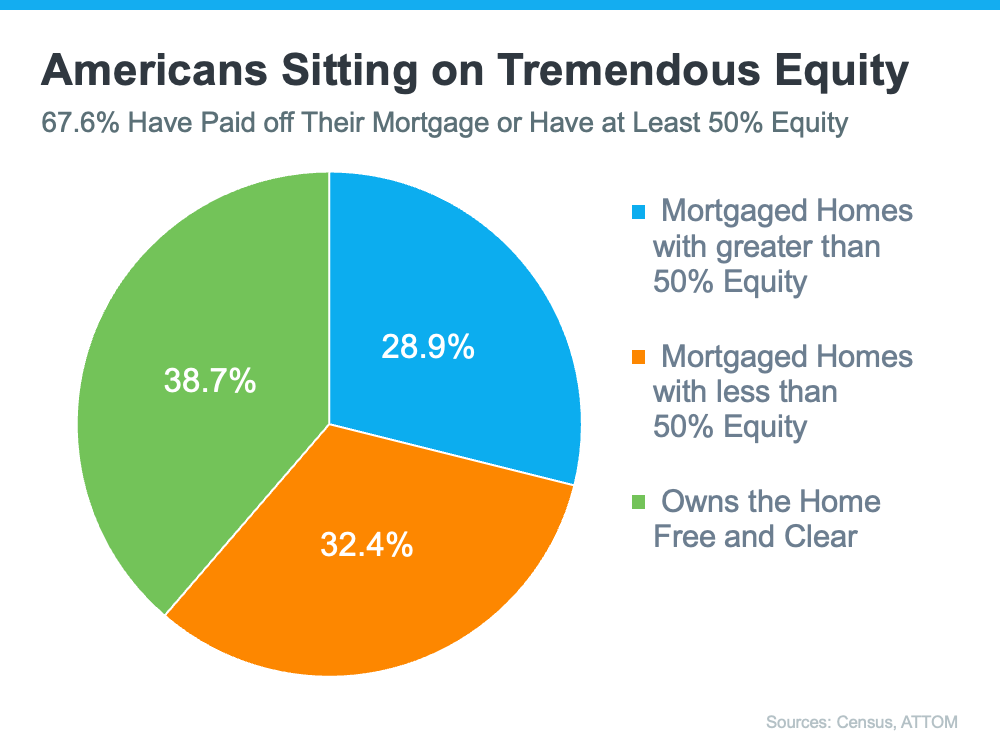

2. The Amount of Homeowner Equity

Second, Americans are sitting on tremendous equity right now. According to the Censusand ATTOM, roughly two-thirds (around 68%) of homeowners have either paid off their mortgage or have at least 50% equity (see chart below):

In the industry, the term for this is equity rich. This is significant because if you think back to 2008, some people had to make the difficult decision to walk away from their homes because they owed more on the home than it was worth.

But this time, things are different because homeowners have built up so much equity over the past few years alone. And, when homeowners have that much equity, it helps us avoid another wave of distressed properties coming onto the market like we saw during the crash. It also creates an extremely strong foundation for today’s housing market.

Bottom Line

We are in one of the most foundationally strong housing markets of our lifetime because homeowners are going to fight to keep their current mortgage rate and they have a tremendous amount of equity. This is yet another reason things are fundamentally different than in 2008.

Today’s mortgage rates are top-of-mind for many homebuyers right now. As a result, if you’re thinking about buying for the first time or selling your current house to move into a home that better fits your needs, you may be asking yourself these two questions:

Why Are Mortgage Rates So High?

When Will Rates Go Back Down?

Here’s context you need to help answer those questions.

1. Why Are Mortgage Rates So High?

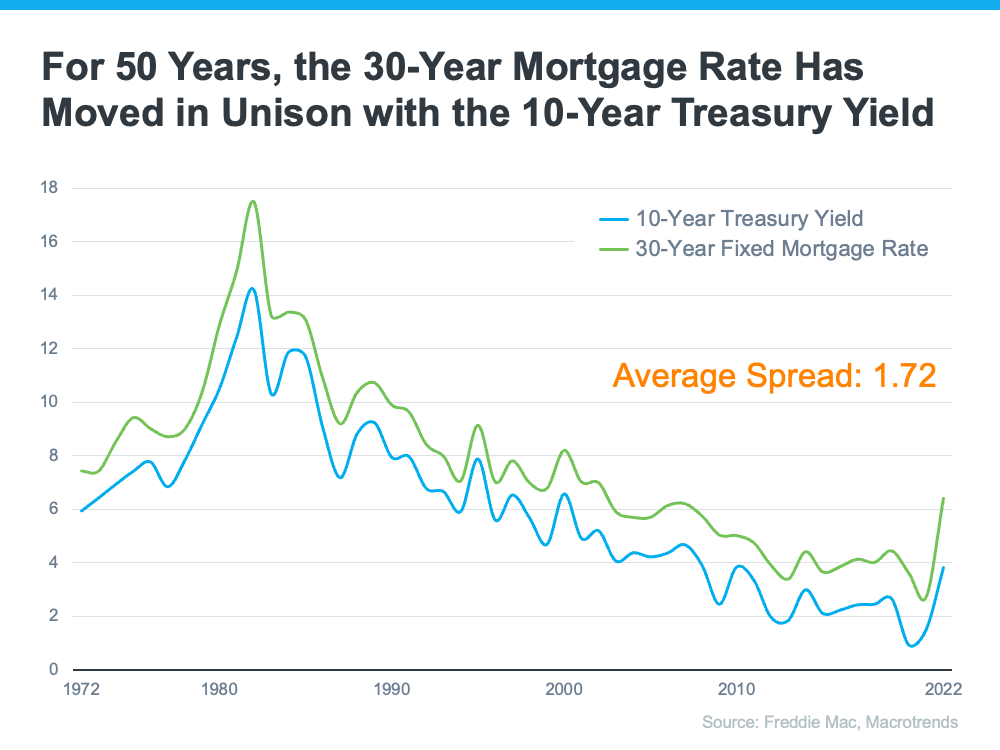

The 30-year fixed-rate mortgage is largely influenced by the supply and demand for mortgage-backed securities (MBS). According to Investopedia:

“Mortgage-backed securities (MBS) are investment products similar to bonds. Each MBS consists of a bundle of home loans and other real estate debt bought from the banks that issued them . . . The investor who buys a mortgage-backed security is essentially lending money to home buyers.”

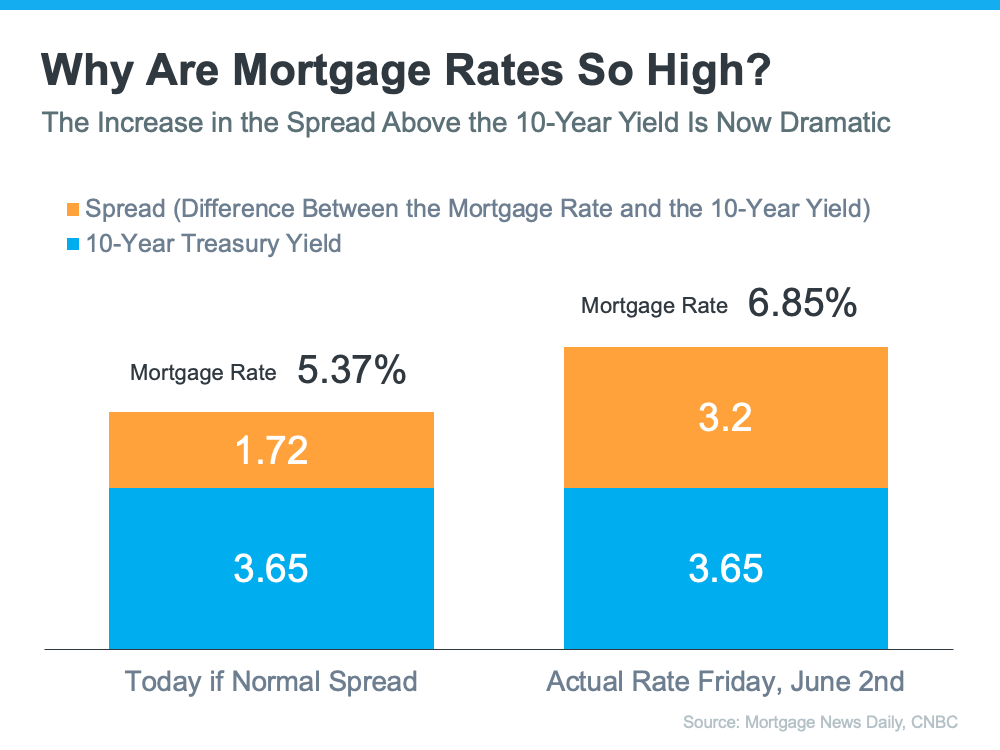

Demand for MBS helps determine the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate. Historically, the average spread between the two is 1.72 (see chart below):

Last Friday morning, the mortgage rate was 6.85%. That means the spread was 3.2%, which is almost 1.5% over the norm. If the spread was at its historical average, mortgage rates would be 5.37% (3.65% 10-Year Treasury Yield + 1.72 spread).

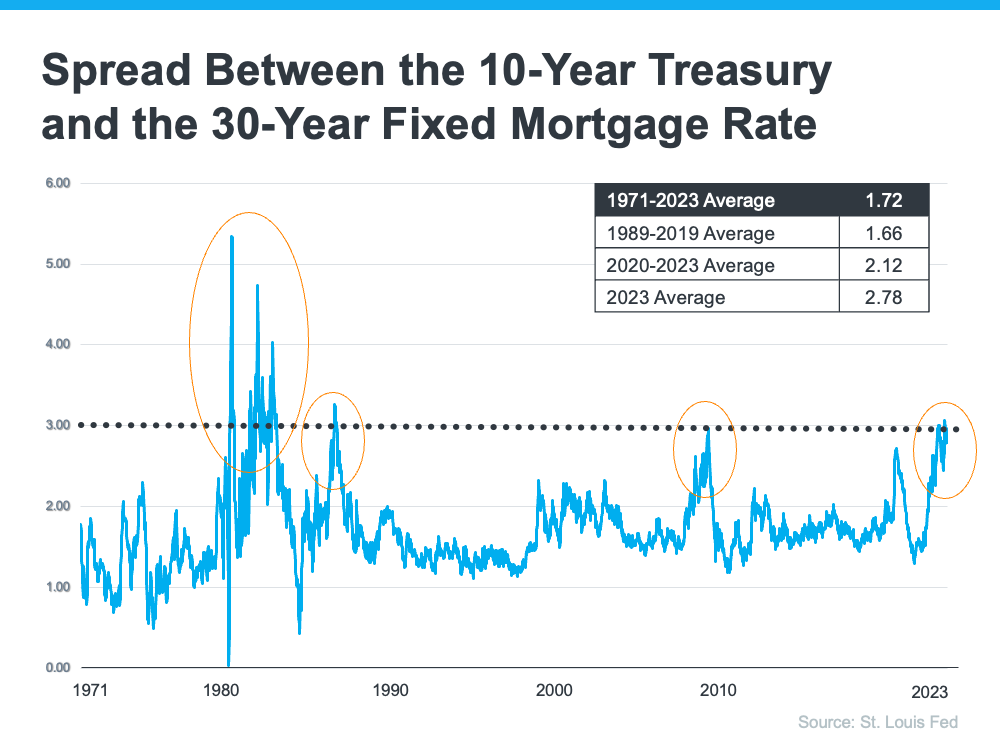

This large spread is very unusual. As George Ratiu, Chief Economist at Keeping Current Matters (KCM), explains:

“The only times the spread approached or exceeded 300 basis points were during periods of high inflation or economic volatility, like those seen in the early 1980s or the Great Financial Crisis of 2008-09.”

The graph below uses historical data to help illustrate this point by showing the few times the spread has increased to 300 basis points or more:

The graph shows how the spread has come down after each peak. The good news is, that means there’s room for mortgage rates to improve today.

So, what’s causing the larger spread and making mortgage rates so high today?

The demand for MBS is heavily influenced by the risks associated with investing in them. Today, that risk is impacted by broader market conditions like inflation and fear of a potential recession, the Fed’s interest rate hikes to try to bring down inflation, headlines that create unnecessarily negative narratives about home prices, and more.

Simply put: when there’s less risk, demand for MBS is high, so mortgage rates will be lower. On the other hand, if there’s more risk with MBS, demand for MBS will be low, and we’ll see higher mortgage rates as a result. Currently, demand for MBS is low, so mortgage rates are high.

2. When Will Rates Go Back Down?

Odeta Kushi, Deputy Chief Economist at First American, answers that question in a recent blog:

“It’s reasonable to assume that the spread and, therefore, mortgage rates will retreat in the second half of the year if the Fed takes its foot off the monetary tightening pedal and provides investors with more certainty. However, it’s unlikely that the spread will return to its historical average of 170 basis points, as some risks are here to stay.”

Bottom Line

The spread will shrink when the fear investors feel is eased. That’ll mean we should see mortgage rates moderate as the year goes on. However, when it comes to forecasting mortgage rates, no one can know for sure exactly what will happen.

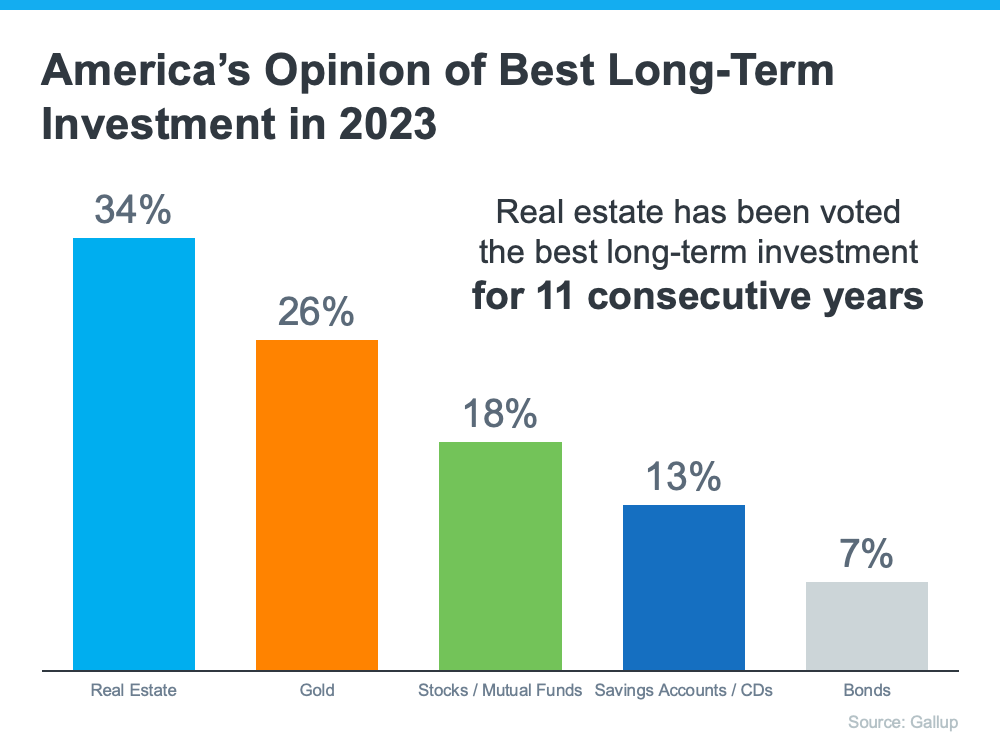

With all the headlines circulating about home prices and rising mortgage rates, you may wonder if it still makes sense to invest in homeownership right now. A recent poll from Gallup shows the answer is yes. In fact, real estate was voted the best long-term investment for the 11th consecutive year, consistently beating other investment types like gold, stocks, and bonds (see graph below):

If you’re thinking about purchasing a home, let this poll reassure you. Even with everything happening today, Americans recognize owning a home is a powerful financial decision.

Why Do Americans Still Feel So Positive About the Value of Investing in a Home?

Purchasing real estate has typically been a solid long-term strategy for building wealth in America. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“. . . homeownership is a catalyst for building wealth for people from all walks of life. A monthly mortgage payment is often considered a forced savings account that helps homeowners build a net worth about 40 times higher than that of a renter.”

That’s because owning a home grows your net worth over time as your home appreciates in value and as you pay down your mortgage. And, since building that wealth takes time, it may make sense to start as soon as you can. If you wait to buy and keep renting, you’ll miss out on those monthly housing payments going toward your home equity.

Bottom Line

Buying a home is a powerful decision. So, it’s no wonder so many people view real estate as the best long-term investment. If you’re ready to start on your own journey toward homeownership, let’s connect today.

“Buckle in. Assuming rates remain near their current 6.5% and the economy skirts recession, then national house prices will fall almost 10% peak-to-trough. Most of those declines will happen sooner rather than later. And house prices will fall 20% if there is a typical recession.”

“Housing is already cooling in the U.S., according to July data that was reported last week. As interest rates climb steadily higher, Goldman Sachs Research’s G-10 home price model suggests home prices will decline by around 5% to 10% from the peak in the U.S. . . . Economists at Goldman Sachs Research say there are risks that housing markets could decline more than their model suggests.”

The Bad News: It Rattled Consumer Confidence

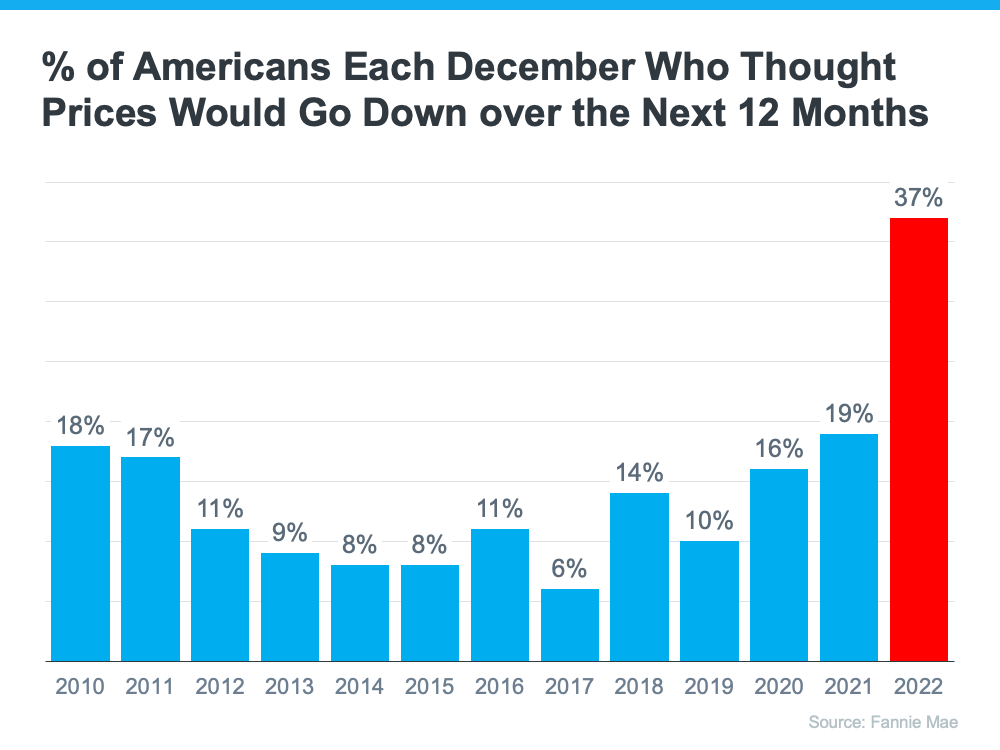

These forecasts put doubt in the minds of many consumers about the strength of the residential real estate market. Evidence of this can be seen in the December Consumer Confidence Survey from Fannie Mae. It showed a larger percentage of Americans believed home prices would fall over the next 12 months than in any other December in the history of the survey (see graph below). That caused people to hesitate about their homebuying or selling plans as we entered the new year.

The Good News: Home Prices Never Crashed

However, home prices didn’t come crashing down and seem to be already rebounding from the minimal depreciation experienced over the last several months.

In a report just released, Goldman Sachsexplained:

“The global housing market seems to be stabilizing faster than expected despite months of rising mortgage rates, according to Goldman Sachs Research. House prices are defying expectations and are rising in major economies such as the U.S.,. . . ”

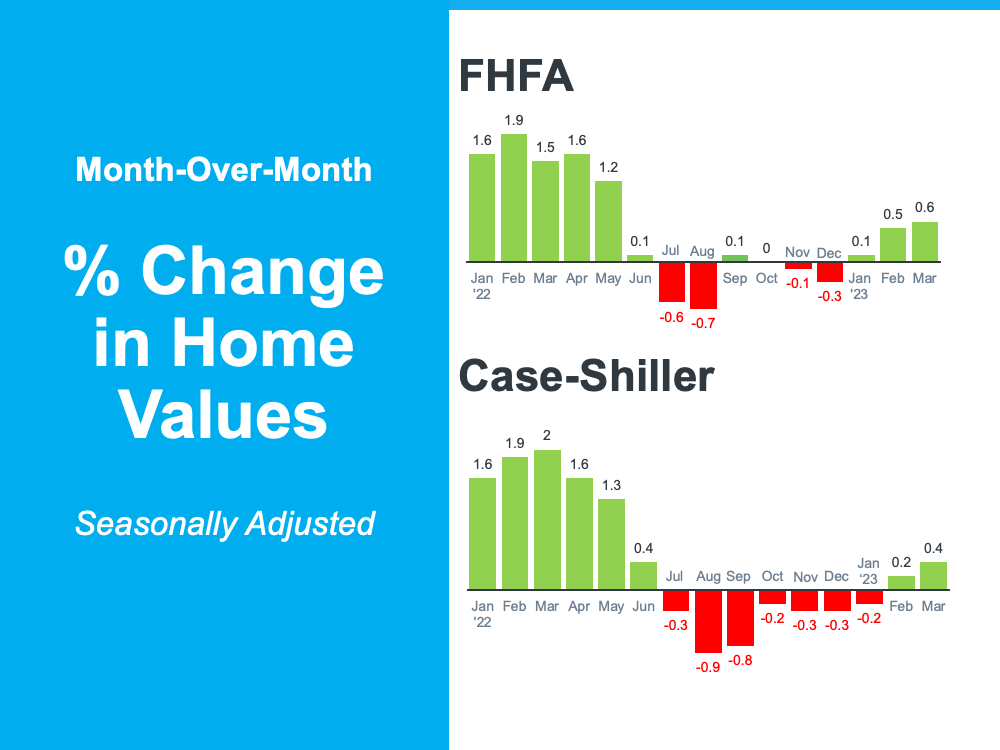

Those claims from Goldman Sachs were verified by the release last week of two indexes on home prices: Case-Shiller and the FHFA. Here are the numbers each reported:

Home values seem to have turned the corner and are headed back up.

Bottom Line

When the forecasts of significant home price depreciation were made last fall, they were made with megaphones. Mass media outlets, industry newspapers, and podcasts all broadcasted the news of an eminent crash in prices.

Now, forecasters are saying the worst is over and it wasn’t anywhere near as bad as they originally projected. However, they are whispering the news instead of using megaphones. As real estate professionals, it is our responsibility – some may say duty – to correct this narrative in the minds of the American consumer.

Buying and owning your home can make a big difference in your life by bringing you joy and a sense of belonging. And with June being National Homeownership Month, it’s the perfect time to think about all the benefits homeownership provides.

Of course, there are financial reasons to buy a house, but it’s important to consider the non-financial benefits that make a home more than just where you live.

Here are three ways owning your home can give you a sense of accomplishment, happiness, and pride.

You May Feel Happier and More Fulfilled

Owning a home is associated with better mental health and well-being. Gary Acosta, CEO and Co-Founder at the National Association of Hispanic Real Estate Professionals (NAHREP), explains:

“Studies have shown the emotional and psychological benefits that homeownership has on a person’s health and self-esteem . . .”

“Residential stability among homeowners is related to improved life satisfaction, . . . along with better physical and mental health.”

So, according to the experts, owning a home can improve your psychological wellness by making you feel happier and more accomplished.

You Can Engage in Your Neighborhood and Grow Your Sense of Community

Your home connects you to your community. Homeowners tend to stay in their homes longer than renters, and that can help you feel more connected to your community because you have more time to build meaningful relationships. And, as Acosta says, when people stay in the same area for a longer period of time, it can lead to them being more involved:

“Homeowners also tend to be more active in their local communities . . .”

After all, it makes sense that someone would want to help improve the area they’re going to be living in for a while.

You Can Customize and Improve Your Living Space

Your home is a place that’s all yours. When you own it, unless there are specific homeowner’s association requirements, you’re free to customize it however you see fit. Whether that’s small home improvements or full-on renovations, your house can be exactly what you want and need it to be. As your tastes and lifestyle change, so can your home. As Investopediatells us:

“One often-cited benefit of homeownership is the knowledge that you own your little corner of the world. You can customize your house, remodel, paint, and decorate without the need to get permission from a landlord.”

Renting can limit your ability to personalize your living space, and even if you do make changes, you may have to undo them before your lease ends. The ability homeownership gives you to customize and improve where you live creates a greater sense of ownership, pride, and connection with your home.

Bottom Line

Owning your home can change your life in a way that gives you greater satisfaction and happiness. Let’s connect today if you’re ready to explore homeownership and all it has to offer.

Does your current home no longer serve your needs?

If so, you may be torn between relocating to a new home or renovating your existing one. This can be a difficult choice, and there’s a lot to consider—including potential costs, long-term financial implications, and quality of life.

A major remodel can be a major commitment. From hiring contractors to selecting materials to managing a budget, it can take a tremendous amount of time and energy—not to mention the ordeal of living through construction or relocating to a temporary residence.

On the other hand, moving is notoriously taxing. In fact, in one survey, 40% of respondents viewed buying a new home as ”the most stressful event in modern life.”1

So which is the better option for you? Let’s take a closer look at some of the factors you should consider before you decide.

1. What Are Your Motivations for Making a Change?

It’s possible that some of the limitations of your current home can be addressed with a renovation, but others may require a move.

Renovate

Certain issues, like dated kitchens and bathrooms, are fairly easy to remedy with a remodel—and the results can be dramatic. In many cases, a relatively minor renovation can significantly increase your enjoyment of your home.

Other shortcomings can be more challenging to fix but are worth exploring so that you know your options. For example, if your home feels cramped or it lacks certain rooms, you might be able to make changes like installing an extra bathroom, adding a dedicated office, or finishing an attic or basement. You may even be able to build an accessory dwelling unit or extension to accommodate a multi-generational family.

In fact, many Americans have remodeled their homes to meet changing needs since the start of the pandemic. According to the National Association of the Remodeling Industry, 90% of their members reported increased demand for renovations starting in 2020, and 60% reported that the scale of remodeling projects has grown.2

However, the feasibility and cost of these larger changes will depend on factors ranging from zoning and permitting to your home’s current layout. Speaking with an architect or a contractor can help you make an informed decision. Let us refer you to one of our trusted partners to ensure you receive the best possible service.

Relocate

Of course, sometimes, even rebuilding your home from the ground up wouldn’t solve the problem. For example, moving may be the only solution if you’ve switched jobs and now face a lengthy commute or if you need to live closer to an aging family member.

Conversely, if the shift to remote work has opened up your location options, you may wish to seize the opportunity to relocate to a new locale. A 2022 study found that nearly five million Americans had already moved since the start of the COVID-19 pandemic due to increased flexibility from remote work, and nearly 19 million more were planning to move in the near future for the same reasons.3

Moving may also be the best option, even when you’re happy with your geographic location. A local move may make sense if you’re looking for a larger backyard or significantly more space. Similarly, some frustrations—like living on a busy street or a long way from a grocery store—can’t be addressed with a renovation. We are well-versed in this area and can help you determine whether another neighborhood might suit you and your family better.

2. Which Option Makes the Most Financial Sense?

Renovating and relocating both come with costs, and it’s wise to explore the financial implications of each choice before you move forward.

Renovate

The costs of a renovation can vary widely, so it’s vital to get several estimates from contractors upfront to understand what it might take to achieve your dream home.

Be sure to consider all of the potential expenditures, from materials and permits to updates to your electrical and plumbing systems. It’s also prudent to add 10-20% to your total budget to account for unexpected issues.4 If you plan to DIY all or part of your renovation, don’t forget to factor in the value of your time.

Renovations can also come with hidden expenses. These might include:

Additional home insurance

Short-term rental or hotel if you need to move out during the renovation

Storage unit for possessions that need to be out of the way

Dining out, laundry service, and other essentials if you can’t access appliances at home

Remodeling choices can also impact the long-term value of your home. Some projects may increase your home’s value enough to outweigh your investment, while others could actually hurt your home’s resale potential.

For example, although you may enjoy the additional living space, garage conversions aren’t typically popular with buyers.5 Refinishing hardwood floors, on the other hand, brings an average return of 147% at resale.2 The specific impact of a renovation will depend on a number of factors, including the quality of work, choice of materials, and buyer preferences in your area. We can help you assess how a planned project is likely to affect the value of your home.

Relocate

The cost of a new home, of course, will vary significantly depending on the features you’re seeking. However, you may find that it’s cheaper to move to a home that has everything you want than it is to make major changes to your existing one.

For example, adding a downstairs bedroom suite or opening up a closed floor plan could cost you more than it would to buy a home that already has those features. On the other hand, simpler changes and updates probably won’t outweigh the expense of a relocation.

If you’re considering a move, speak with a real estate agent early in the process. We can assess your current home’s value and estimate the price of a new home that meets your needs. This will help you set an appropriate budget and expectations.

It’s important to remember that the cost of buying a new home doesn’t end with the purchase price. You’ll also need to account for additional expenditures, including closing and moving costs and the fees involved with selling your current home. And don’t forget to compare current mortgage rates to your existing one to understand how a different rate could impact your monthly payment.

However, keep in mind that the interest rate on a mortgage is typically lower than the rate on other loan types—so you could pay less interest on a new home purchase than you would on remodel.6 We’re happy to refer you to a lending professional who can help you explore your financing options.

3. Which Option Will Be the Least Disruptive to Your Life?

A final—but critical—consideration is the time and hassle involved with each option since both renovating and relocating involve a significant amount of each.

Renovate

Don’t underestimate the time and effort involved in a large-scale renovation, even if you choose to hire a general contractor. You will still need to consider and make a number of decisions. For example, even a fairly basic kitchen remodel can involve a seemingly-endless selection of cabinets, tile, countertops, paint colors, fixtures, hardware, and appliances.

And don’t assume that you will get out of packing and unpacking if you stay in your current home. Most renovations—from kitchens to bathrooms to flooring replacement—require you to remove your belongings during the construction process.

The time frame for a remodel is another consideration. High demand for contractors and ongoing material shortages can mean a long wait to get started. And once the project is in progress, you can expect that it will take a couple of weeks to several months to complete.7

Contemplate whether you will be able to live in your home while it’s being renovated and how that would impact your routine. For example, being without a functional kitchen for months can be frustrating, inconvenient, and expensive (since you’ll need to purchase prepared food). Remember that delays are inevitable with construction, and consider what additional challenges they could present.

Relocate

Of course, finding a new home and selling your current one also takes a significant amount of time and energy. According to the National Association of Realtors’ 2022 Profile of Home Buyers and Sellers, the average buyer searched for 10 weeks and toured a median of five homes.8

However, in many cases, the timeline can still be shorter than a major renovation. Once you find a home that works for you, it typically takes between 30 and 60 days to close if you’re taking on a mortgage—and the process is even faster if you’re paying with cash.9 Plus, you can look for your dream home without the inconvenience of living in a construction zone.

However, a move comes with its own stress and disruptions. If you’re selling your current home, you’ll need to prep it for the market and keep it ready and available for showings. Once you’ve found a place, the packing and moving process takes time and work, as does settling into a new home—especially if it’s in a different neighborhood.

Fortunately, we are here to help make the moving process as easy as possible, if you choose to pursue that route. We can help you find a property that meets all your needs, sell your current one for top dollar, and refer you to some excellent moving companies that can help pack and transport your belongings.

WHATEVER YOU DECIDE, WE CAN HELP

The decision to renovate or relocate can be overwhelming—but this choice also presents a powerful opportunity to improve your quality of life.

There’s a lot to consider, from how renovations could impact your home’s resale value down the road to your neighborhood’s current market dynamics. We’re happy to help you think through your options. Get in touch for a free consultation!

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.