As we enter the middle of 2021, many are wondering if we’ll see big changes in the housing market during the second half of this year. Here’s a look at what some experts have to say about key factors that will drive the industry and the economy forward in the months to come.

“. . . homes continue to sell quickly in what’s normally the fastest-moving time of the year. This is in contrast with 2020 when homes sold slower in the spring and fastest in September and October. While we expect fall to be competitive, this year’s seasonal pattern is likely to be more normal, with homes selling fastest from roughly now until mid-summer.”

“Sellers who have been hesitant to list homes as part of their personal health safety precautions may be more encouraged to list and show their homes with a population mostly vaccinated by the mid-year.”

“Surveys showed that seller confidence continued to rise in April. Extra confidence plus our recent survey finding that more homeowners than normal are planning to list their homes for sale in the next 12 months suggest that while we may not see an end to the sellers’ market, we might see the intensity of the competition diminish as buyers have more options to choose from.”

“We forecast that mortgage rates will continue to rise through the end of next year. We estimate the 30-year fixed mortgage rate will average 3.4% in the fourth quarter of 2021, rising to 3.8% in the fourth quarter of 2022.”

Bottom Line

Experts are optimistic about the second half of the year. Let’s connect today to talk more about the conditions in our local market.

Today’s housing market is full of unprecedented opportunities. High buyer demand paired with record-low housing inventory is creating the ultimate sellers’ market, which means it’s a fantastic time to sell your house. However, that doesn’t mean sellers are guaranteed success no matter what. There are still some key things to know so you can avoid costly mistakes and win big when you make a move.

1. Price Your House Right

When inventory is low, like it is in the current market, it’s common to think buyers will pay whatever we ask when setting a listing price. Believe it or not, that’s not always true. Even in a sellers’ market, listing your house for the right price will maximize the number of buyers that see your house. This creates the best environment for bidding wars, which in turn are more likely to increase the final sale price. A real estate professional is the best person to help you set the best price for your house so you can achieve your financial goals.

2. Keep Your Emotions in Check

Today, homeowners are living in their houses for a longer period of time. Since 1985, the average time a homeowner owned their home, or their tenure, has increased from 5 to 10 years (See graph below):This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you purchased or the house where your children grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from that sentimental value.

For some homeowners, that connection makes it even harder to separate the emotional value of the house from the fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

3. Stage Your House Properly

We’re generally quite proud of our décor and how we’ve customized our houses to make them our own unique homes. However, not all buyers will feel the same way about your design and personal touches. That’s why it’s so important to make sure you stage your house with the buyer in mind.

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. Stage, clean, and declutter so they can visualize their own dreams as they walk through each room. A real estate professional can help you with tips to get your home ready to stage and sell.

Bottom Line

Today’s sellers’ market might be your best chance to make a move. If you’re considering selling your house, let’s connect today so you have the expert guidance you need to navigate through the process and prioritize these key elements.

For the eighth year in a row, real estate maintained its position as the preferred long-term investment among Americans.

Real estate has been gaining ground against stocks, gold, and savings accounts over the last 11 years and now stands at its highest rating in survey history.

Let’s connect if you’re ready to make real estate your best investment this year.

The level of equity homeowners have is at an all-time high. According to the U.S. Census, over 38% of owner-occupied homes are owned free and clear, meaning they don’t have a mortgage. Those with a mortgage are seeing their equity skyrocket too. Every time real estate values increase, homeowners get a dollar-for-dollar gain in their home equity.

“17.8 million residential properties in the United States were considered equity-rich, meaning that the combined estimated amount of loans secured by those properties was 50 percent or less of their estimated market value.

The count of equity-rich properties in the first quarter of 2021 represented 31.9 percent, or about one in three, of the 55.8 million mortgaged homes in the United States. That was up from 30.2 percent in the fourth quarter of 2020, 28.3 percent in the third quarter and 26.5 percent in the first quarter of 2020.”

This surge in home equity has given most homeowners the opportunity to use that equity in one of two ways:

Refinance to cash out some of the equity or lower their current payment

Move to a home that better fits their current needs

Let’s break down the possibilities.

1. Refinance

An abundance of equity and record-low mortgage rates can make refinancing a home very easy. Some homeowners choose to refinance so they can lower their payments. Others convert a portion of the equity to cash while keeping their monthly payment the same.

There are many homeowners who could take advantage of lower rates and higher levels of equity, but they haven’t yet. According to an Economic & Housing Research Note from earlier this month, there were over five million homeowners with a loan funded by Freddie Mac who would benefit by refinancing their loan. As of January 2021, there were:

452,122 loans with an average mortgage rate of 6.17%

1,027,834 loans with an average mortgage rate of 4.39%

3,687,780 loans with an average mortgage rate of 4.21%

With mortgage rates currently hovering around 3%, any of these homeowners would benefit from refinancing. They could lower their payments by hundreds of dollars per month or cash out large sums of equity while keeping their monthly payment the same.

Example:

If a homeowner has a $200,000 fixed-rate mortgage with a 6% interest rate and refinances that loan to a 3% interest rate, their monthly mortgage payment (principal and interest) will go from $1,199 per month to $843 per month – a savings of $356 a month, or $4,272 each year.

On the other hand, if they keep their mortgage payment the same, they could cash out a significant amount of their equity.

2. Move into your dream home

The past year prompted many households to redefine what a dream home really means, and it’s something different to everyone. Those who have a high mortgage rate could use their equity as a down payment and perhaps buy their next home without significantly raising their mortgage payment.

Example:

Suppose a person bought a house for $216,000 at the height of the market in 2006. (The median home price in May of 2006). If they put 10% down and took out a mortgage of $194,400 at 6.41% (the average rate in 2006), the monthly mortgage payment (principal and interest) would have been $1,217.

According to the National Association of Realtors (NAR), a typical single-family home has grown in value by approximately $150,000 over the last fifteen years. That means the $216,000 house would be worth about $366,000 today.

After deducting selling expenses, they would be left with about $130,000 ($150,000 minus approximately $20,000 in selling expenses).

A seller could take that equity and use it as a down payment on a new house. Let’s assume they purchased a home for $450,000 (roughly $80,000 more than the value of their current home). If they put the $130,000 down, they could take out a mortgage of $320,000 with a 3% interest rate. The monthly mortgage payment (principal and interest) would be $1,349. Therefore, they could buy a home worth $80,000 more than the one they have today and only spend an extra $132 per month.

Bottom Line

Whether you’re refinancing your house or moving to a new home, your current mortgage rate and your level of equity are crucial in your decision-making process. Look at your mortgage documentation to find out your interest rate, and then let’s connect to determine the potential equity in your home. You may be surprised by the opportunities you have.

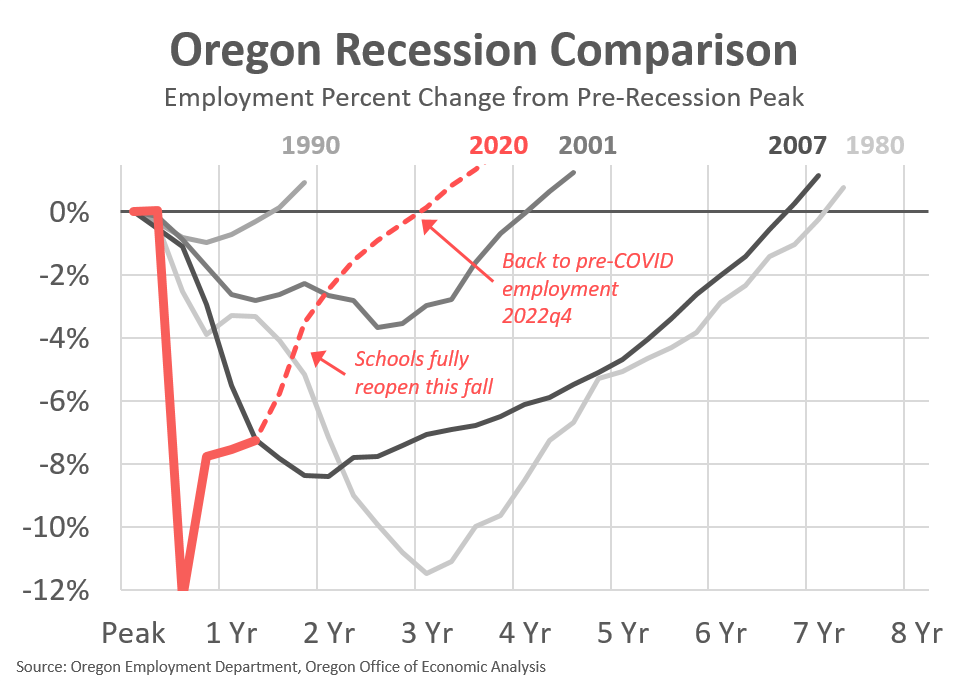

This afternoon the Oregon Office of Economic Analysis released the latest quarterly economic and revenue forecast. For the full document, slides and forecast data please see our main website. Below is the forecast’s Executive Summary and a copy of our presentation slides.

Economic growth is surging as the pandemic wanes. Thanks to federal fiscal policy, consumers have higher incomes today than before COVID-19 hit. Now they are increasingly allowed to and feel comfortable resuming pandemic-restricted activities like going out to eat, on vacations, getting haircuts and the like. The outlook for near-term economic growth is the strongest in decades, if not generations.

Oregon’s labor market is expected to return to full health during the upcoming 2021-23 biennium. With the strong near-term outlook for consumer spending, job growth is front-loaded such that the largest employment gains will occur this summer and fall. Total employment in Oregon will surpass pre-pandemic levels in late 2022 with the unemployment rate returning to near 4 percent in 2023.

While a jobs hole remains in the labor market, the same cannot be said for household incomes. Currently incomes in Oregon are 20 percent higher than before COVID-19 hit, thanks in larger part due to the temporary federal measures put in place. Excluding the direct federal aid, incomes are back to pre-pandemic levels and expected to grow 6-7% this year and next.

However, with such a strong consensus near-term outlook, the risks do primarily lie to the downside. The risk is that supply cannot keep pace with demand. The path forward may be bumpier than expected, even if the trajectory is up. Already supply constraints have emerged in semiconductors, lumber, and rental cars to name a few. More bottlenecks are likely on the horizon. Furthermore, running through all of these issues is labor. Attracting and retaining workers is already much more challenging than expected given the economy went through a severe recession last year. There are a variety of simultaneous factors impacting the number of available workers including strong household finances, the virus itself, and lack of childcare or in-person schooling. While the temporary pandemic-related constraints will ease in the months ahead, the labor market is expected to remain tight for the foreseeable future in large part due to demographics and the large number of Baby Boomers retiring.

With the prospect of strong growth and near-term supply constraints, the possibility of an overheating economy has quickly replaced fears of a long-lasting, demand-driven recession like the past few cycles have been. Undoubtedly inflation will pick up in the months ahead. Production costs are rising quickly in part due to capacity constraints and bottlenecks. However these price pressures are coming off of a low base and are largely expected to be transitory. The Federal Reserve so far has indicated it will only become concerned should price pressures turn persistent. Given the overall economy is not at full employment, and generally strong wage growth is needed for persistent inflation, almost by definition the current bout of inflation is transitory.

In May of odd-numbered years, the revenue forecast takes on added importance. With the legislature in session, the May forecast determines the size of General Fund resources available for the upcoming budget, and sets the bar for Oregon’s unique kicker law.

Oregon’s state revenue outlook continues to brighten as the income tax season unfolds. Personal and corporate tax collections are booming despite the job losses and business woes brought on by the COVID pandemic. Tax collections based on consumer spending are also posting large gains. With the near-term economic outlook looking very strong, healthy growth in tax collections is expected to continue into the 2021-23 budget period.

In a typical year, the income tax filing season is winding down when the May forecast is produced. At that point, the vast majority of payments have been processed, and we have a good idea of how the tax season turned out. This year, the tax filing deadline was extended to May 17th due to the pandemic, leaving many returns yet to be processed. This injects added uncertainty into the outlook. In particular, there is the potential for a significant revenue surprise (up or down) in the final weeks of the biennium. That suggests that leaving a large ending balance would be wise. Also, it is possible that the size of the kicker credit for next year will change significantly from the current estimate when the kicker is certified this fall.

So far, with around half of payments having come in, the tax season is turning out to be a healthy one. Payments are expected to reach an all-time high by the end of the fiscal year. While there is still a large amount of payments outstanding, most of this season’s refunds have already been issued. Taxpayers who are expecting refunds tend to file returns earlier than those making payments. Refunds are significantly lower than they were last year, due largely to the kicker credit issued in 2020. This year, refunds include $81 million in automatic adjustments sent to 164,000 taxpayers who paid taxes on unemployment insurance benefits. In March, the federal government exempted the first $10,200 in unemployment benefits from taxation. The Oregon Department of Revenue has sent refunds to taxpayers who filed before the exemption was announced.

In light of massive job losses, Oregon’s General Fund revenue outlook for the current biennium was revised downward by around $2 billion immediately following the onset of the COVID-19 pandemic. As of the May 2021 forecast, this hole has more than been filled, with the outlook now calling for significantly more revenue than was expected before the recession began.

Many factors are playing into the unexpectedly strong revenue collections, but two reasons stand out. First, an unprecedented amount of federal aid has far outstripped the size of economic losses. As a result, personal income is up sharply in Oregon despite job cuts. Second, during the typical recession, Oregon has lost a tremendous amount of revenue associated with sharp declines in investment and business income. This time around, asset markets and profits have remained at or near record highs. The baseline outlook prior to the recession called for income growth to slow. A tight labor market was expected to weigh on growth, and asset prices and profits were expected to return to sustainable levels. None of this came to pass, leading to an expected personal income tax kicker of $1.4 billion and a corporate tax kicker of $664 million.

Looking forward into the 2021-23 biennium, the increasingly rosy economic outlook suggests healthy tax collections will persist. A broad consensus of economic forecasters is calling for near-term output growth to be the strongest seen in decades. Given Oregon’s unique kicker law, a booming economic outlook requires an equally aggressive revenue outlook to match it. Taxable income is expected to continue to post healthy gains, showing no evidence of the economic shock we are living through. The outlook for General Fund tax collections has been revised up by around 5% over the next few years. This translates into significantly more resources for policymakers.

Although budget writers have a lot more to work with, a good deal of caution is required and savings are a must. The kicker law dictates that we stick our necks out with an aggressive revenue outlook, exposing us to the risk of a large budget shortfall should growth stall. Of primary concern are nonwage forms of income including profits and the return on investments. With a healthy underlying economy, economic forecasters are calling for continued growth in stock prices, profits and the like. Although valuations are unsustainably high right now, forecasters predict underlying economic activity will catch up over time. Unfortunately, this does not mesh well with our past experience. Profits and capital gains often evaporate overnight, which always puts Oregon’s budget in a hole.

See our full website for all the forecast details. Our presentation slides for the forecast release to the Legislature are below.

According to the National Association of Realtors, after recording the quickest recovery in the nation’s history in the wake of the COVID-19 pandemic, the U.S. economy is expected to kick into higher gear in 2021.

With the number of vaccinated Americans increasing and new coronavirus cases on the decline, NAR Chief Economist Lawrence Yun anticipates the economy will grow 4.5% in 2021.

“Consumers will begin to spend massive savings, and do more shopping, restaurant dining, traveling and in-person house hunting,” he said.

While home sales continue to be an economic bright spot, unemployment remains an issue. Eight million jobs that were lost during the pandemic have not yet been recaptured. Yun maintains that job recovery is taking longer due to some friction in the labor market, including workers being unable to return to their jobs, where work-from-home is not an option for many. As economic growth strengthens, 4 million jobs are projected to be gained this year.

Despite high unemployment, the economic recovery – propelled by favorable monetary and fiscal policies – has created the hottest housing market in nearly 50 years. The marketplace has surpassed pre-pandemic levels in terms of sales, but the fast-paced recovery has contributed to historic home price growth. In fact, an NAR report released this past week found that 89% of metros saw prices climb at double-digit rates on a year-over-year basis during the first quarter of 2021.

Thursday’s presentation noted that the economic recovery, both in the U.S. and globally, has raised inflationary pressures which will ultimately lead to an increase in the 30-year fixed mortgage to an average of 3.2% in 2021. Consumer price inflation is accelerating due to higher costs for a number of goods and commodities, including oil, gasoline, lumber, moving and storage fees, household appliances, rents, and houses, which have reached record-highs.

“As mortgage rates increase, the frenzied multiple-offer situation will become less prevalent by year’s end, as affordability challenges squeeze out some buyers and more inventory reaches the market,” Yun said.

Although the low supply of housing has played a significant role in home price surges, Yun expects more home construction, a growing willingness among homeowners to list properties due to an increase in vaccinations, and a gradual decline in mortgage forbearance.

In addition to homebuilders’ intentions to ramp-up construction, a recent NAR report – Case Studies on Repurposing Vacant Hotels/Motels into Multifamily Housing – details the idea of remodeling underutilized hotels and motels in order to help replenish the supply of affordable multifamily housing.

“With more inventory and some easing in demand, home prices are expected to shift to mid-single-digit appreciation by the fourth quarter and in 2022,” Yun said.

Yun predicts that the median existing-home sales price will increase at a slower pace of 7% in 2021.

As more homes reach the market, NAR anticipates existing-home sales to grow by 10% and forecasts new home sales to jump by 20%.

So far, bond markets are taking the prospect of Fed tapering of monthly purchases of $40B in mortgage-backed securities and $80B in Treasuries in stride

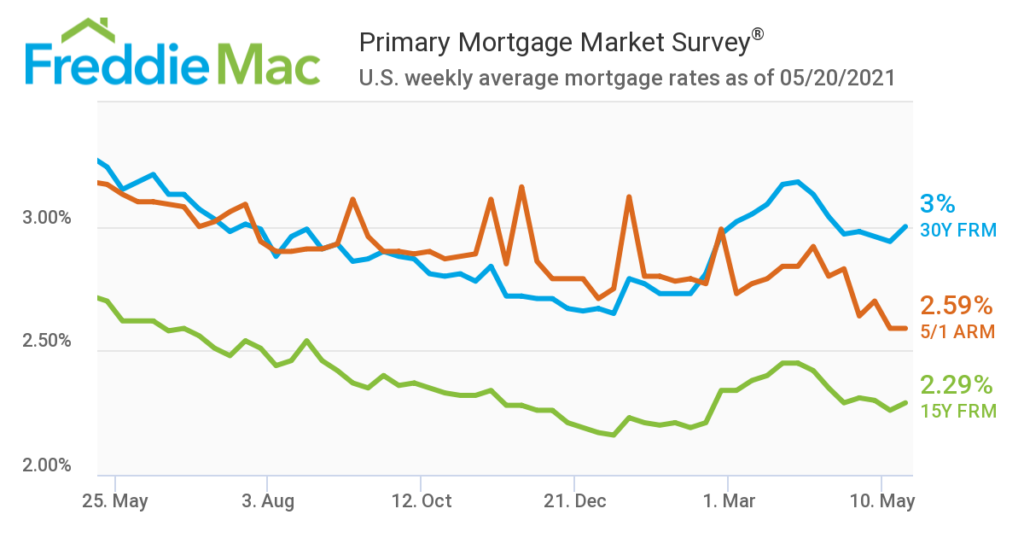

Mortgage rates were up slightly during the week ending May 20, as borrowers with excellent credit putting 20 percent down were offered rates averaging 3.00 percent on 30-year fixed-rate purchase mortgages.

That’s according to the latest weekly rate survey from Freddie Mac, which showed rates registering their first weekly increase in May. The survey, which records rates going back to 1971, showed 30-year, fixed-rate mortgages hitting an all-time low of 2.65 percent during the week ending Jan. 7, before heading back up to 3.18 percent in March.

“After a run up over the first few months of the year, rates have paused and hovered around three percent since March,” said Freddie Mac Chief Economist Sam Khater, in a statement. “Despite this favorable rate climate, there remains a shortage of homes for sale. The lack of housing supply has been compounded by labor disruptions and expensive building materials that are driving up the cost of new housing, making it difficult for homebuyers to find homes to purchase.”

Freddie Mac reported average rates for the following mortgage types for the week ending May 20:

Rates on 30-year fixed-rate mortgages averaged 3.00 percent with an average 0.6 point, up from 2.94 percent last week but down from 3.24 percent a year ago.

For 15-year fixed-rate mortgages, rates averaged 2.29 percent with an average 0.7 point, up from 2.26 percent last week but down from 2.70 percent a year ago.

Rates on 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) loans averaged 2.59 percent with an average 0.3 point, unchanged from last week and down from 3.17 percent a year ago.

In a new forecast this week, Fannie Mae economists said they expect a gradual rise in rates this year and next, with 30-year fixed-rate mortgages averaging 3.5 percent by the final quarter of 2022. But inflation worries could drive steeper rate increases, they warned.

Minutes from the April 27-28 meeting of the Federal Reserve’s Federal Open Market Committee published Wedensday revealed that some Fed officials are open to debating whether to taper the Fed’s monthly purchases of $40 billion in mortgage-backed securities and $80 billion in Treasuries.

Those purchases help keep long-term interest rates low, and word that the Fed might consider tapering in the months ahead initially sent yields on 10-year Treasurys, a benchmark for mortgage rates, to soar. But 10-year Treasury yields were down Thursday, as investors continued to weigh the likelihood of the Fed tapering its bond purchases.

Even small moves in mortgage rates can have a big impact on homebuying power. A recent analysis by First American concluded that higher mortgage rates in March contributed to a $13,000 decline in homebuying power nationally.

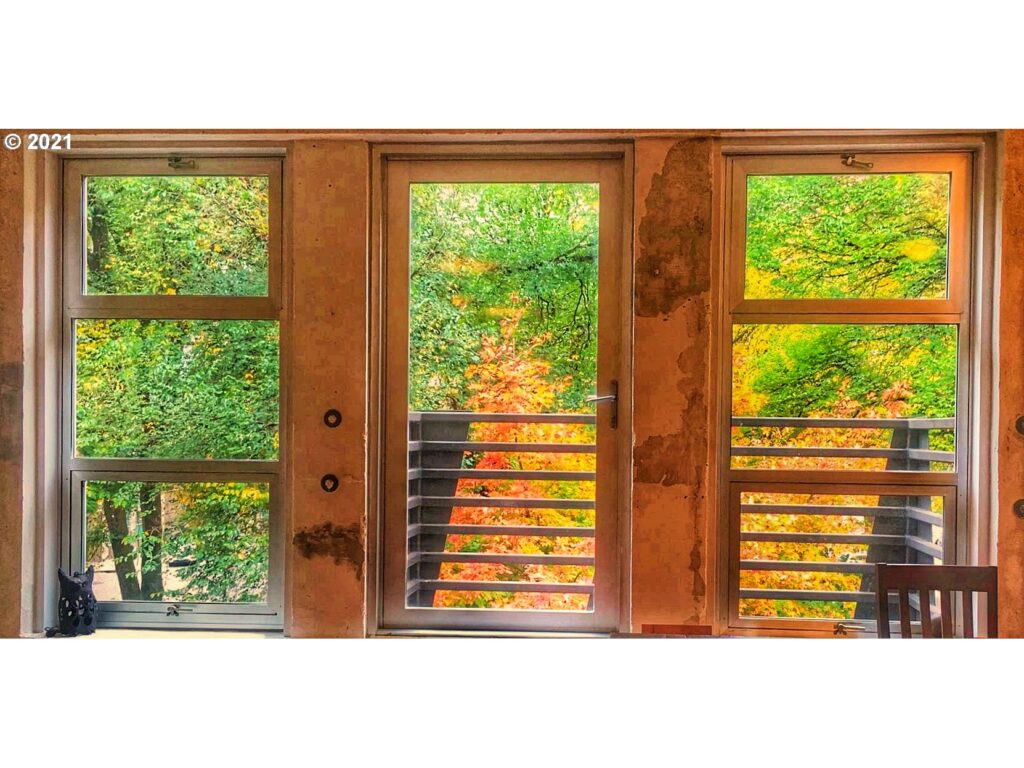

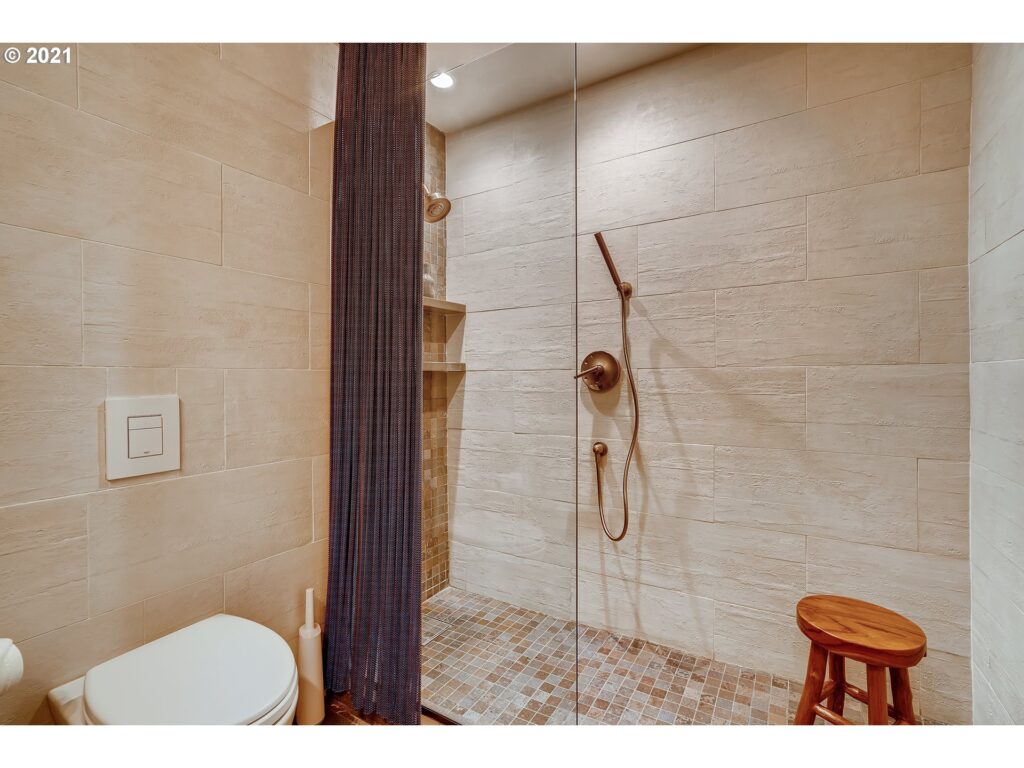

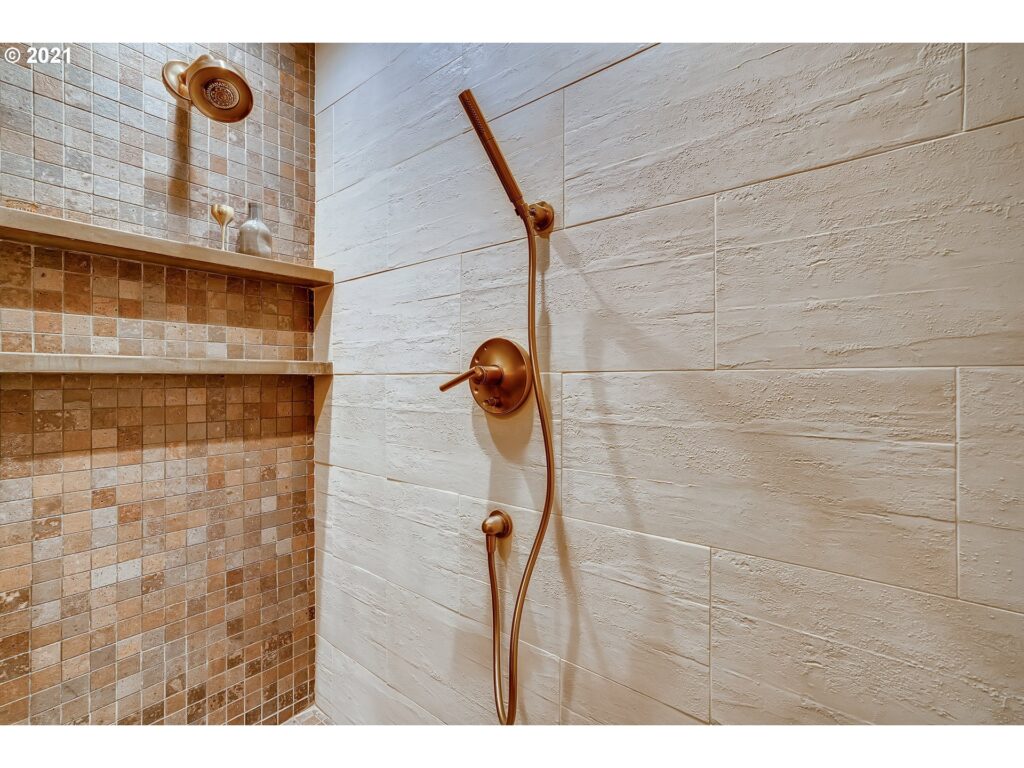

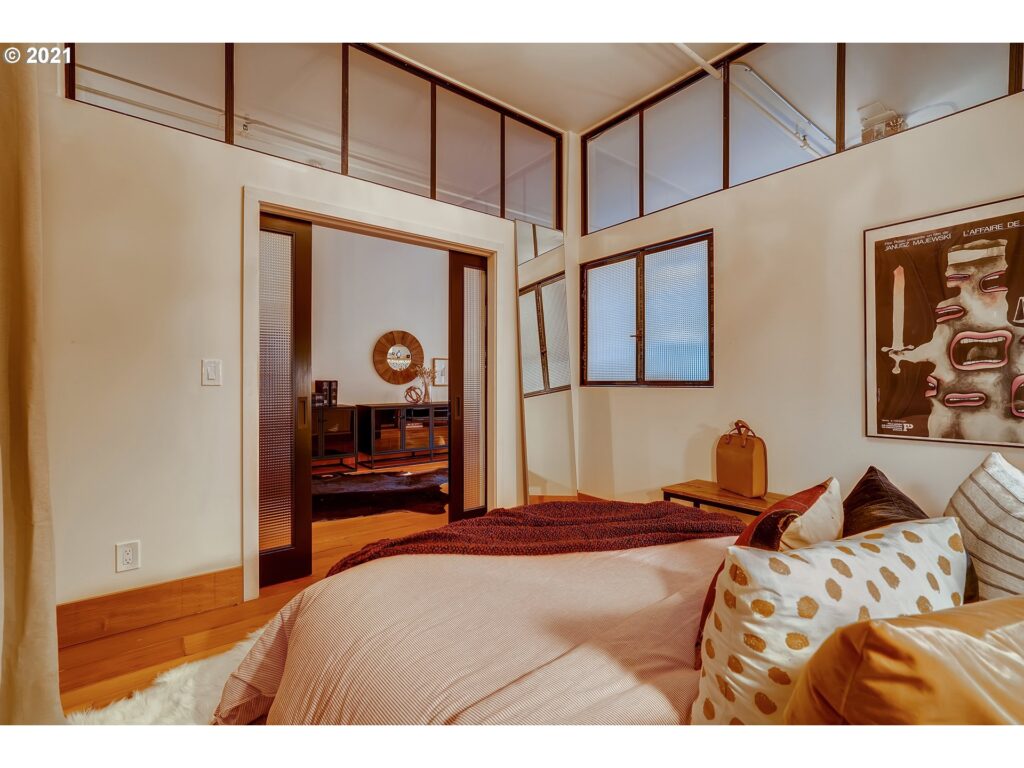

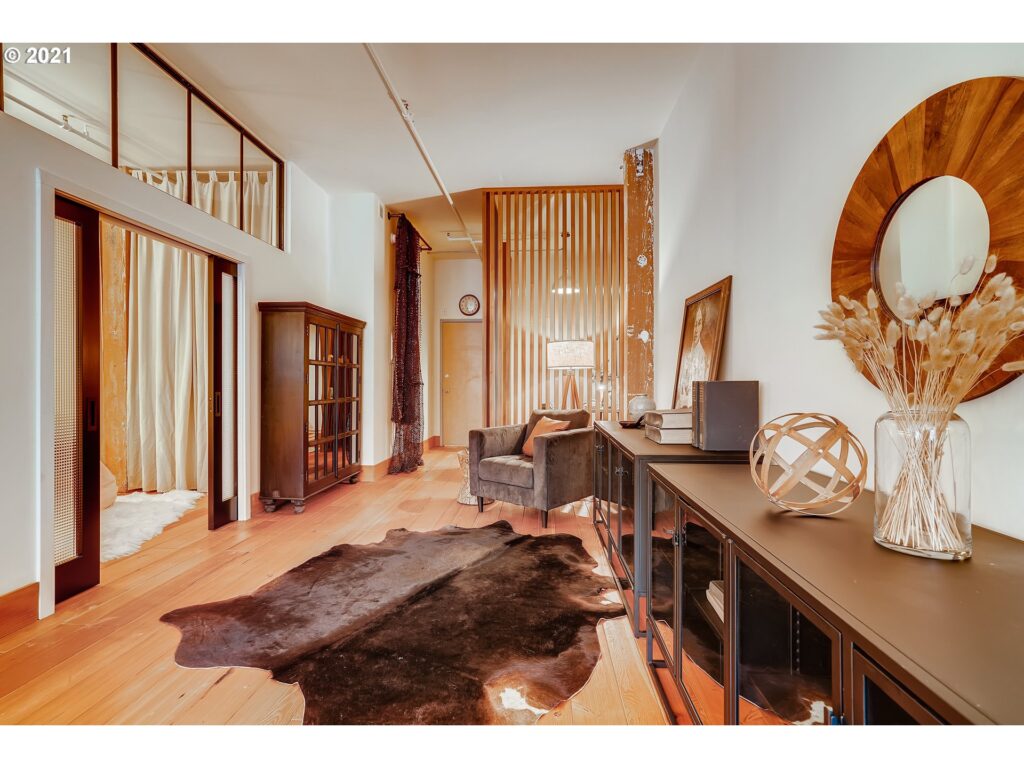

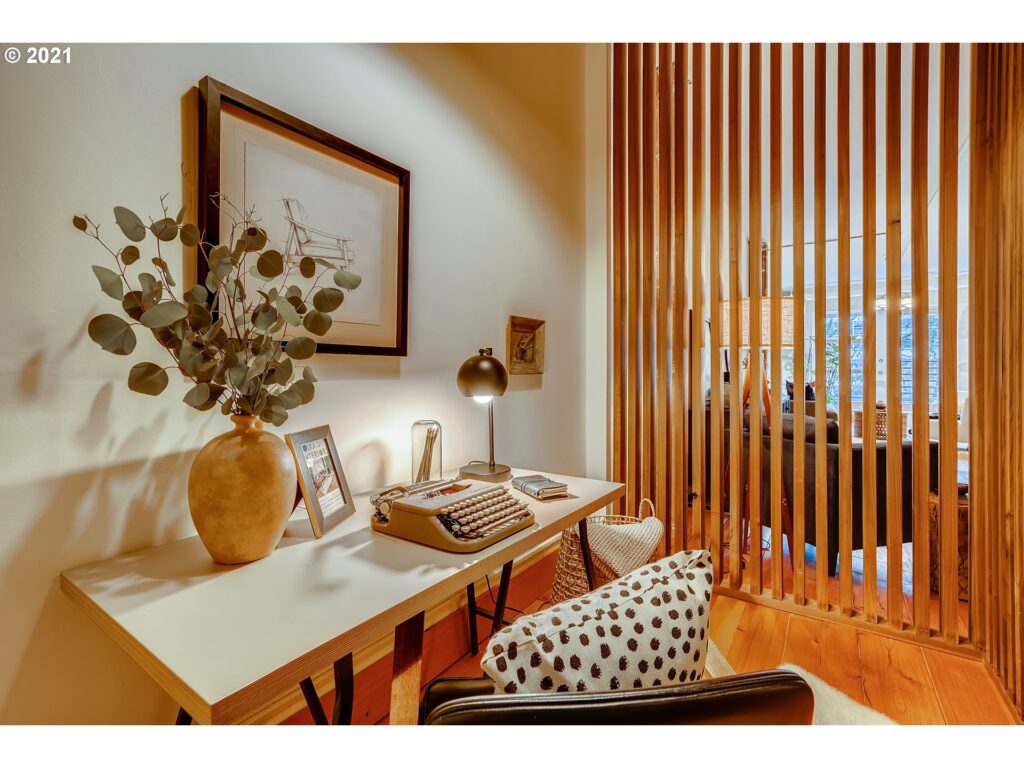

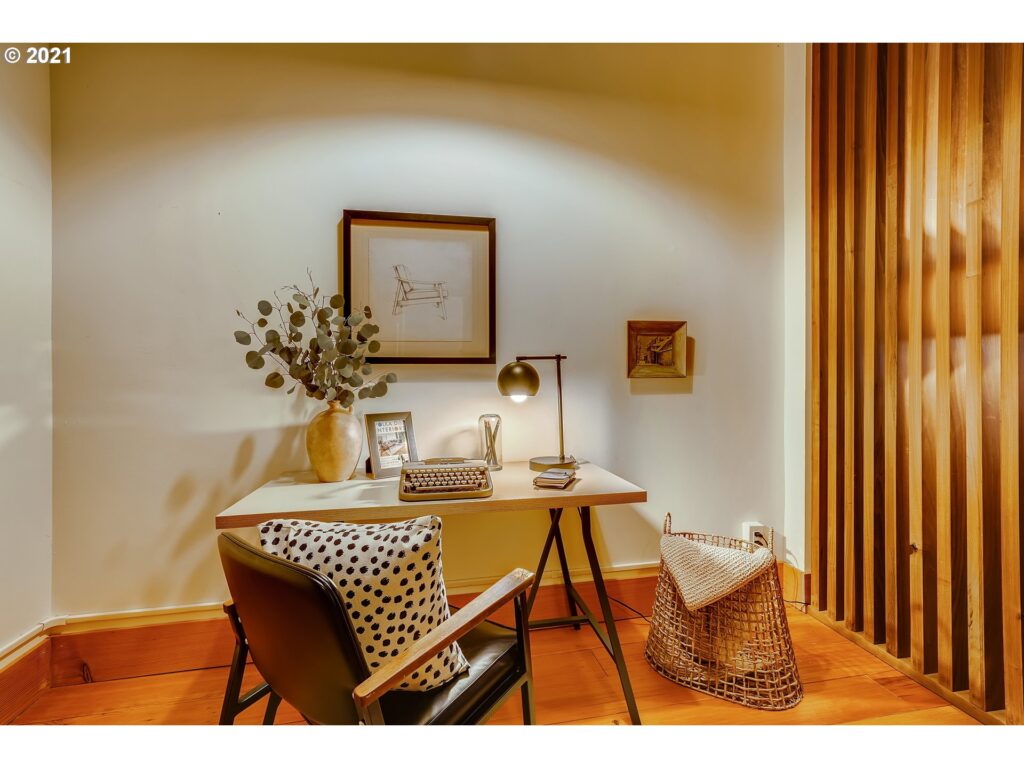

725 NW FLANDERS ST Portland, OR 97209 1bed/1bath 1037 sqft $450,000 Have you seen this show-stopping loft in the Pearl w/ A+ designer finishes. Stunning reclaimed wood floors. 10 foot ceilings. Balcony & huge windows to tree canopy bring nature & light in. Kitchen w/ gas stove, custom counters/shelves. Designer lighting. Bedroom w/ transom windows, unique glass pocket door & cool steel window. Office w/ smoked poplar louvered slat wall. Bathroom: designer tile, reclaimed wood counter, carved natural stone sink. Easy access to Galleries, Whole Foods, Restaurants, Theater, Transport. No rental cap. Minimum 7 day rental. Mixed-use building allows Residential & Many Studio/Professional/Office uses. W/D included. Walk/Transit/Bike scores 99/92/99. New high-efficiency mini-split heat pump & tankless hot water heater in 2017. New commercial building across park blocks. MLS#: 21548144 CALL ME BEFORE IT’S GONE!

4625 SW 55TH PL Portland, OR 97221 $480,000 3bd/2ba 1348 sqft Rare find on large lot in Bridlemile. Private back yard w/ awesome deck atop sloping natural greenery & small creek. Enjoy the low-maintenance nature setting while water ripples & birds chirp. Great floorplan w/ hardwoods & skylights in common areas. Vaulted ceilings with exposed wood beams & fireplace in living room. Large, versatile Office/Den/Bonus space facing greenery. 2-car garage. Newer roof & exterior paint. Double paned windows & sliders. Perfectly located between Downtown & Tech Park. Call me before it’s gone! MLS#: 21147670

Jordan Cohen, the top RE/MAX agent in the world, calls the luxury Ojai ranch – complete with 35 miles of hiking trails, an auto museum and private lake – a groundbreaking listing.

Hold on to your hats: This $100 million luxury ranch is unlike any other.

Black Mountain Ranch in Ojai, California, is a prestigious 3,600-acre working cattle and horse ranch that consists of 63 consecutive parcels of land. Called an “absolute epic one-of-a-kind property” by listing agent Jordan Cohen, Black Mountain Ranch features a 13,250-square-foot main residence in addition to a 6,203-square foot carriage house, 1,965-square-foot caretaker cottage and 1,800-square-foot guest cottage. For anyone keeping track, that’s already 23,218 square feet of living space on the mountain-view property.

Additional features include an automobile museum, multiple barns, private fishing lake, shooting range and 35 miles(!) of serene nature trails.

“This is truly the very best Southern California has to offer,” said Cohen, the No. 1 RE/MAX agent in the world, in an Instagram post highlighting the property. “This is my most groundbreaking listing and I could not be more excited!!”

![Americans Choose Real Estate as the Best Investment [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/05/20143944/20210521-MEM-1046x2001.png)