The housing market has gone through a lot of change recently, and much of that was a result of how quickly mortgage rates rose last year.

Continue reading “Experts Forecast a Turnaround in the Housing Market in 2023”The housing market has gone through a lot of change recently, and much of that was a result of how quickly mortgage rates rose last year.

Continue reading “Experts Forecast a Turnaround in the Housing Market in 2023”

If you’re a homeowner ready to make a move, you may be thinking about using your current house as a short-term rental property instead of selling it. A short-term rental (STR) is typically offered as an alternative to a hotel, and they’re an investment that’s gained popularity in recent years. According to a Harris Poll survey, 28% of homeowners have considered using a rental service to temporarily rent out their home for additional income.

Continue reading “Should You Rent Your House or Sell It?”When exploring mortgage options, many potential homebuyers turn to the Federal Housing Administration (FHA) loan program for its accessible credit requirements and low down payment options. FHA loans are particularly popular among first-time homebuyers and individuals with limited financial resources. However, like any financial decision, it’s crucial to be well-informed before committing to an FHA loan. In this article, we’ll highlight several key factors to keep in mind when considering an FHA loan, empowering you to make an informed decision that aligns with your long-term financial goals.

1. FHA Loan Basics

FHA loans were established by the U.S. Department of Housing and Urban Development (HUD) to facilitate homeownership for low to moderate-income borrowers. These loans are insured by the FHA, allowing approved lenders to offer favorable terms and lower interest rates to borrowers with less-than-perfect credit histories. The primary advantage of an FHA loan is its low down payment requirement, often as low as 3.5% of the home’s purchase price, making it an attractive option for buyers with limited savings.

2. Mortgage Insurance Premium (MIP)

One essential aspect of FHA loans is the Mortgage Insurance Premium (MIP). Unlike conventional loans, FHA loans require borrowers to pay both an upfront MIP at closing and an annual MIP over the life of the loan. The upfront MIP is typically 1.75% of the loan amount, while the annual MIP amount varies based on factors such as loan term, loan-to-value ratio, and loan amount. It’s essential to consider these additional costs when evaluating the overall affordability of an FHA loan.

3. Credit Requirements

FHA loans are renowned for their lenient credit requirements, often accommodating borrowers with credit scores as low as 580. However, a lower credit score may result in a higher down payment, potentially up to 10% for individuals with scores between 500 and 579. Although FHA loans provide flexibility, it’s crucial to remember that a higher credit score can still lead to more favorable terms and lower interest rates.

4. Property Eligibility

The property being purchased must meet certain eligibility criteria to qualify for an FHA loan. These requirements are in place to ensure the property’s safety, habitability, and marketability. Properties must be used as primary residences, and certain types of properties, such as fixer-uppers, may require additional inspections and appraisal conditions. Before selecting a property, it is advisable to verify its eligibility to avoid any surprises during the loan application process.

5. Debt-to-Income Ratio

FHA loans consider both your housing expenses and overall debt obligations when determining eligibility. Generally, the debt-to-income (DTI) ratio should not exceed 43%, including the projected mortgage payment. Lenders may have additional overlays, which are stricter requirements on top of FHA guidelines, so it’s essential to check with the lender for specific DTI requirements.

6. Loan Limits

FHA loan limits vary by region and are subject to change annually. These limits determine the maximum loan amount a borrower can obtain with an FHA loan in a specific area. It’s crucial to stay informed about the current loan limits to avoid disappointment if your desired property exceeds the FHA loan cap.

FHA loans offer a viable pathway to homeownership for individuals who may not qualify for conventional loans due to credit or financial constraints. Understanding the key aspects of FHA loans, such as the MIP, credit requirements, property eligibility, DTI ratio, and loan limits, is vital in making an informed decision about this type of mortgage. As with any significant financial commitment, potential borrowers should thoroughly evaluate their financial situation and consider seeking guidance from a qualified mortgage professional to determine if an FHA loan aligns with their homeownership goals. By doing so, aspiring homeowners can embark on their homeownership journey with confidence and clarity.

CEO, RE/MAX Caribbean & Central America (CCA) Region. Investor. Mentor. Educator. Public Speaker

January 7, 2023

High inflation is a problem for mainstream investors in the United States. Inflation is a portfolio killer because it wreaks havoc on the stock market.

The knee-jerk reaction is to put money in fixed-income assets with a guaranteed return. This is a terrible strategy considering inflation was last clocked at 7.11% – after five rate hikes by the FED in 2022. A guaranteed return doesn’t mean you’re guaranteed to make a profit – especially if you’re considering putting your money in a CD, Money Market Account (MMA), high-yield savings account (HYSA), treasuries, or any other fixed-income asset. When considering the current inflation rate, fixed-income assets will lose you money.

Putting money in a CD, MMA, HYSA, or treasury that pays at best 4.6% (5-year CD, according to nerdwallet.com) results in an annual loss of 2.5% annual loss.

Fixed-income assets are not the way to deal with inflation.

Banking is the right idea to deal with inflation, but it’s not the traditional type of banking that will save your portfolio; it’s land banking. What is land banking? It’s exactly as its name implies. It’s an investment strategy where you buy land and then sell when the value increases. Because property values – especially in high-demand, high-growth locales – typically outpace inflation, it’s a great strategy for battling inflation.

Besides acting as a buffer against inflation, land banking can also be a lucrative real estate investment strategy. Think of it as a buy-and-hold strategy without the tenant and broken air conditioner issues. It’s a strategy that’s been around for more than 500 years and one that has made millionaires for countless investors.

John Jacob Astor became America’s first multi-millionaire using this strategy. He purchased large tracts of land in New York. Today, that area is known as Manhattan. Aston saw the potential of that tract of land and was one of the few people at the time to see land banking as a great opportunity. If John Astor’s net worth resulting from the sale of that land was measured in the present day, it would amount to over $100 billion.

Land banking is not the first strategy that comes to mind when investors consider real estate, but it’s a valuable strategy investors should consider – especially in offshore locales.

Land banking requires patience (minimum holding periods of at least five years). Still, it’s entirely headache free because land requires no maintenance, which is a distinct advantage over traditional real estate investments. Land costs nearly nothing to own. Compared to commercial and residential properties that require maintenance and upkeep, land banking is becoming more and more appealing to savvy investors.

Investors considering land banking should consider investing offshore. That’s because of the relatively low property tax rates. In Belize, the property tax rate for unoccupied land is 1%. In Mexico, it’s 1/10th of 1%. The low property tax rates can only improve the bottom line and rate of return when it comes time to sell the property.

Real estate investing without having to deal with deadbeat tenants and toilet and plumbing repairs? Yes, please!

The ultra-wealthy have been using land banking to build and insulate wealth for years. While mainstream investors have been stressing over their up-and-down 401k’s in a volatile stock market, smart investors have been sitting back and watching their land values go up while the rest of the market goes on a roller coaster ride.

While many investors rush to fixed-income assets to “preserve” their assets, ultra-wealthy investors have been diversifying with offshore land to insulate their portfolios against uncertainty, downturns, and inflation. Even as they’re protecting their portfolios with land banking, these savvy investors are also watching their wealth grow as the value of their land holdings grow. And in hot offshore markets, their wealth only accelerates that much more.

With its hot growth and growing popularity as a tourist and retirement destination, Belize is ideal for land banking. With booming development activity, acquiring a piece of land in Belize or any other offshore locale with subdivision potential and then holding that land to eventually break it up into smaller titles and selling them off for a profit can be a highly lucrative strategy.

Land banking has long been used by smart investors not only for wealth building but also for portfolio protection. In addition, this strategy is ideal in a stable and quickly developing offshore locale with low tax rates and laws favorable to foreign investors. That’s why investors interested in land banking should consider Belize.

![Tips To Reach Your Homebuying Goals in 2023 [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/05124509/Tips-To-Reach-Your-Homebuying-Goals-in-2023-MEM-1046x2405.png)

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.

A great way to ease some of those emotions and ensure you’re feeling confident in your decision is to keep these three best practices in mind.

The housing market shifted in 2022 as mortgage rates rose, buyer demand eased, and the number of homes for sale grew. As a seller, you’ll want to recognize things are different now and price your house appropriately based on where the market is today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Price your home realistically. This isn’t the housing market of April or May, so buyer traffic will be substantially slower, but appropriately priced homes are still selling quickly.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be.

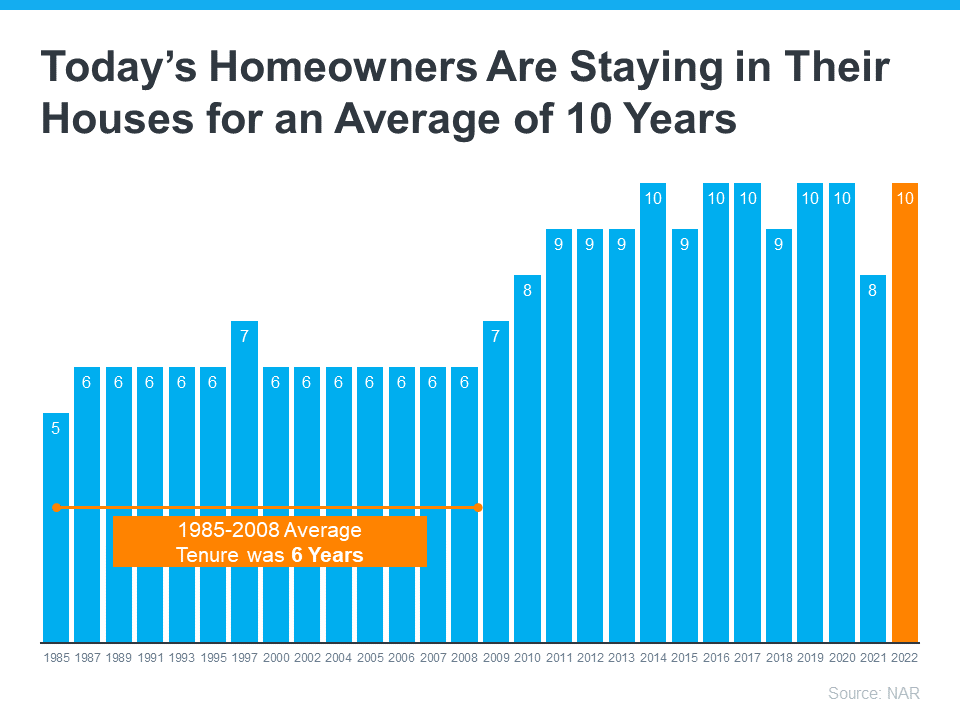

Today, homeowners are living in their houses longer. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 5 to 10 years (see graph below):

This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even harder to negotiate and separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

While you may love your decor and how you’ve customized your home over the years, not all buyers will feel the same way about your design. That’s why it’s so important to make sure you focus on your home’s first impression so it appeals to as many buyers as possible. As NAR says:

“Staging is the art of preparing a home to appeal to the greatest number of potential buyers in your market. The right arrangements can move you into a higher price-point and help buyers fall in love the moment they walk through the door.”

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. A real estate professional can help you with tips to get your house ready to sell.

If you’re considering selling your house, let’s connect so you have the help you need to navigate through the process while prioritizing these best practices.

If you’re a renter, you likely face an important decision every year: renew your current lease, start a new one, or buy a home. This year is no different. But before you dive too deeply into your options, it helps to understand the true costs of renting moving forward.

In the past year, both current renters and new renters have seen their rent go up based on information from realtor.com:

“Three out of four renters (74.2%) who have moved in the past 12 months reported seeing their rent increase. The strain from recent rent hikes isn’t exclusive to renters who have recently moved. Nearly two-thirds of renters (63.2%) who have lived in their current rental between 12 and 24 months, and likely renewed their lease, have also reported increases in their rent.”

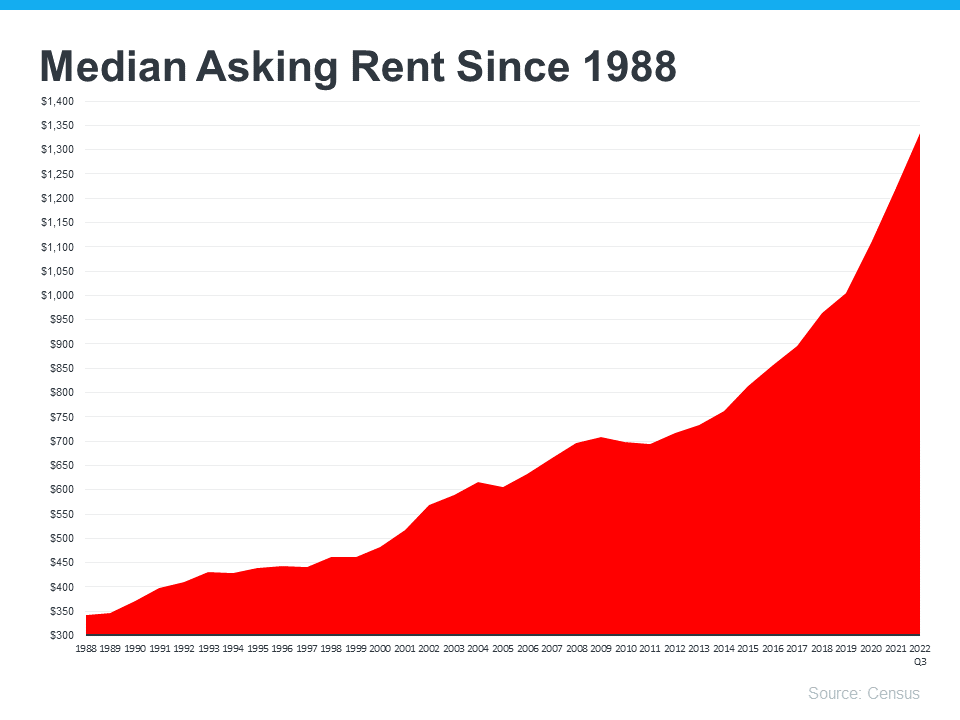

And if you look back at historical data, that shouldn’t come as surprise. That’s because, according to the Census, rents have been rising fairly consistently since 1988 (see graph below):

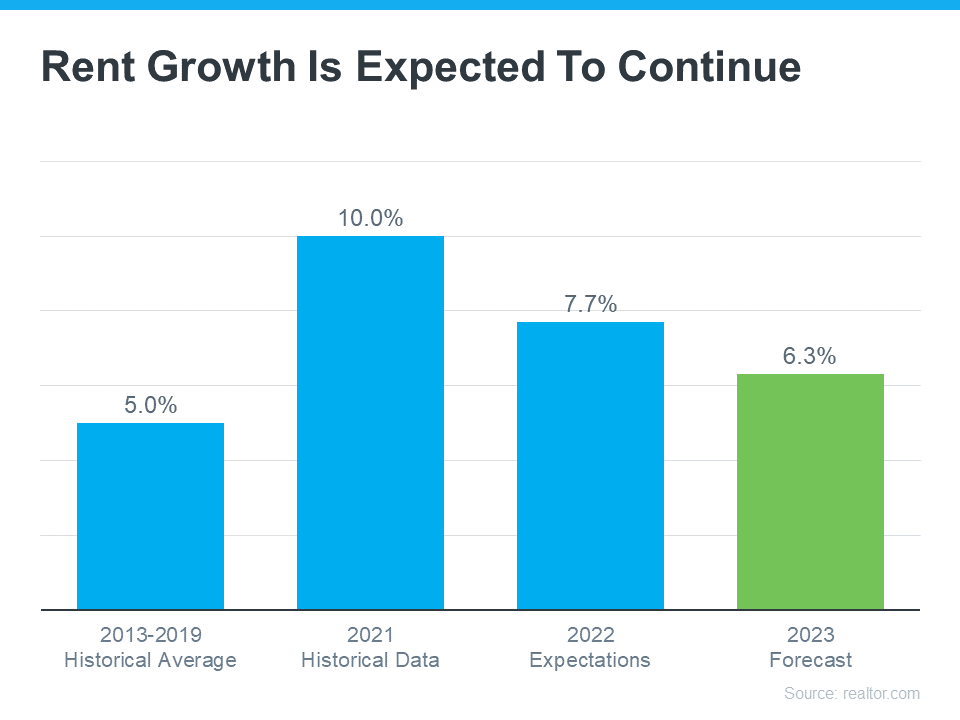

So, if you’re considering renting as an option in 2023, it’s worth weighing whether this trend is likely to continue. The 2023 Housing Forecast from realtor.com expects rents will keep climbing (see graph below):

That forecast projects rents will increase by 6.3% in the year ahead (shown in green). When compared to the blue bars in the graph, it’s clear that the 2023 projection doesn’t call for an increase as drastic as the ones renters have seen over the past two years, but it’s still above the historical average for rent hikes between 2013-2019.

That means, if you’re planning to rent again this year and you’ve not yet renewed your lease, you may pay more when you do.

These rising costs may make you reconsider what other alternatives you have. If you’re looking for more stability, it could be time to prioritize homeownership. One of the many benefits of owning your own home is it provides a stable monthly cost that you can lock in for the duration of your loan. As Freddie Mac says:

“Monthly rent payments may increase over time, but a fixed-rate mortgage will ensure that you’re paying the same amount each month. With a fixed-rate mortgage, your interest rate is locked in for the life of loan. Steady payments allow you to budget wisely and make plans for the future.”

If you’re planning to make a move this year, locking in your monthly housing costs for the duration of your loan can be a major benefit. You’ll avoid wondering if you’ll need to adjust your budget to account for annual increases like you would if you left your housing payment up to your landlord and their renewal cycle.

Homeowners also enjoy the added benefit of home equity, which has grown substantially. In fact, the latest Homeowner Equity Insight report from CoreLogic shows the average homeowner gained $34,300 in equity over the last 12 months. As a renter, your rent payment only covers the cost of your dwelling. When you pay your mortgage on a house, you grow your wealth through the forced savings that is your home equity.

If you’re thinking of renting this year, it’s important to keep in mind the true costs you’ll face. Let’s chat to see how you can begin your journey to homeownership today.

If you’re getting ready to buy your first home, you’re likely focused on saving up for everything that purchase involves. One cost that’s likely top of mind is your down payment. But don’t let a common misconception about how much you need to save make the process harder than it could be.

Freddie Mac explains:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

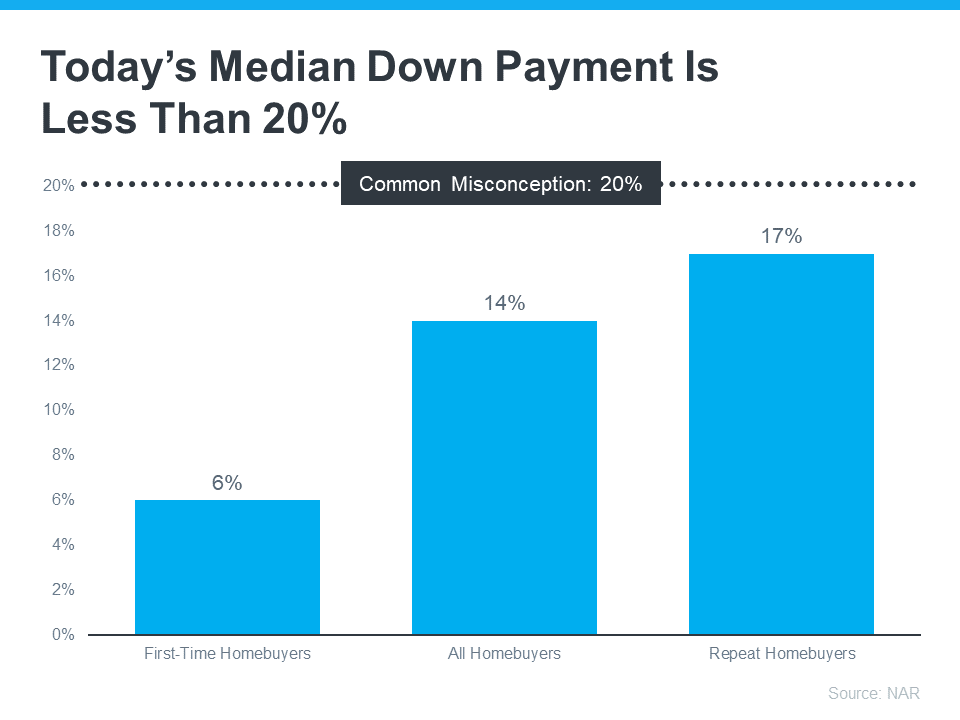

Unless specified by your loan type or lender, it’s typically not required to put 20% down. This means you could be closer to your homebuying dream than you realize. According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, the median down payment today is only 14%. And it’s even lower for first-time homebuyers at just 6% (see graph below):

If saving for a down payment still feels like a challenge, know that there’s help available. A real estate professional and trusted lender can show you options that could help you get closer to your down payment goal. According to latest Homeownership Program Index from Down Payment Resource, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments.

Plus there are even loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

To understand your options, be sure to do your homework. If you’re interested in learning more about down payment assistance programs, information is available through sites like Down Payment Resource. Then, partner with a trusted lender to learn what you qualify for on your homebuying journey.

Remember, a 20% down payment isn’t always required. If you want to purchase a home this year, let’s connect. You’ll also want to make sure you have a trusted lender so you can explore your down payment options.

If buying or selling a home is part of your dreams for 2023, it’s essential for you to understand today’s housing market, define your goals, and work with industry experts to bring your homeownership vision for the new year into focus.

In the last year, high inflation had a big impact on the economy, the housing market, and likely on your wallet too. That’s why it’s critical to have a clear understanding of not just the market today, but also what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few questions you can start thinking through as you fine tune your goals for 2023.

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time and have a space that’s truly your own. Use what’s motivating you as a guidepost in partnership with an expert advisor to help make sure your move will give you a lasting sense of accomplishment.

You know you want to move, but how would you describe your dream home? The available supply of homes for sale has grown, and that could mean more options to choose from when you buy. Just be sure to keep your budget in mind and work with a trusted real estate professional to balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it can be to find the home that’s right for you.

Getting clear on your budget and savings is essential before you get too far into the process. Working with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if your move involves selling your existing house.

Buying or selling a home is a big process that takes expertise to navigate. If that feels a bit overwhelming, you aren’t alone. According to a recent Harris Poll survey, one in five respondents see a lack of information or knowledge about the homebuying process as a barrier from owning a home. Don’t let uncertainty hold you back from your goals this year. A trusted expert can bridge that gap and give you the best advice and information about today’s market.

Let’s connect to plan how your dreams for 2023 can become a reality.

While it’s exciting to start thinking about moving in and decorating after you’ve applied for your mortgage, there are some key things to keep in mind before you close. Here’s a list of things you may not realize you need to avoid after applying for your home loan.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgage. Resist the temptation to make any large purchases, even for furniture or appliances.

When you cosign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

It doesn’t matter whether it’s a new credit card or a new car, when you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those aspects of your score.

Be upfront about any changes that occur or you’re expecting to occur when talking with your lender. Blips in income, assets or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.