Portland area housing market even more cutthroat for buyers as new listings drop

Updated: Nov. 22, 2021, 9:43 a.m. | Published: Nov. 19, 2021, 5:12 p.m.

By Jayati Ramakrishnan | The Oregonian/OregonLive

Homebuyers found an even smaller supply of homes to choose from in October as new listings dropped in the Portland metro area.

New numbers from the regional listing service RMLS show that homes are staying on the market for a shorter time, with fewer sellers entering the market even as the demand for homes goes up. The number of new listings dropped 8% from a year ago.

Meanwhile, the median home price climbed 12% since last October, hitting $516,000.

For the month of October, RMLS reported a 0.9-month supply of homes, meaning that if sales continued at the current pace, it would take just under a month to sell everything already on the market. An inventory of less than six months is historically considered a seller’s market.

But some agents predict things are only going to get more difficult for buyers. Dustin Miller, a real estate broker with Windermere predicts that there could soon be just half a month’s worth of inventory on the market — a number said he’s never seen.

Even in the long run, Miller said he’s not sure things will return to the days of 4 to 6 months of inventory on the market.

“Unless something drastic happens like huge amounts of housing being built to handle the supply/demand issue,” he said. “I would say it looks like we have a new normal.”

Eduardo Reyes, a broker with John L. Scott Real Estate, said he’s observed a slowdown from the surge of competition he saw for homes this summer.

“There were instances where there were up to 20 or 30 offers per house,” he said of the summer. “I’ve never had as many offers or had houses selling as fast as they did.”

When he takes clients out now, he said, there are fewer homes to tour, but he’s not seeing quite the same rush of competing buyers he did in June or July.

The report shows that homes are selling faster than they did at the same time last year, but the pace slowed somewhat from last month. The typical home sold in October was on the market for 26 days before it attracted an winning offer, according to RMLS, about two days slower than homes sold in September. The data showed a 2-day increase in total market time since September.

The short supply of houses has changed the way buyers approach the process, Miller said. Many may have to adjust their idea of what’s “non-negotiable” in a home, such as buying a home with a kitchen they don’t like, in order to live in a neighborhood they do.

“Everything has become new territory for us as agents,” Miller said. “We’re trying to get creative in hunting down houses for our buyers, and giving sellers new expectations of what could happen in the marketplace.”

—Jayati Ramakrishnan; 503-221-4320; jramakrishnan@oregonian.com; @JRamakrishnanOR

Home Sales About To Surge? We May See a Winter Like Never Before.

Like most industries, residential real estate has a seasonality to it. For example, toy stores sell more toys in October, November, and December than they do in any other three-month span throughout the year. More cars are sold in the U.S. during the second quarter (April, May, and June) than in any other quarter of the year.

Real estate is very similar. The number of homes sold in the spring is almost always much greater than at any other time of the year. It’s even labeled as the spring buying season. Historically, the number of buyers and listings for sale significantly increase in the spring and remains strong throughout the summer. Once fall sets in, the number of buyers and sellers typically drops off.

Last year, however, that seasonality didn’t happen. The outbreak of the virus and subsequent slowing of the economy limited sales during the spring market. These sales were pushed back later in the year, and last fall and winter saw a dramatic increase in home sales over previous years. The only thing that held the market back was the extremely limited supply of homes for sale.

What About This Winter?

Some experts thought we’d return to the industry’s normal seasonality this winter with both the number of purchasers and houses available for sale falling off. However, data now shows that neither of those situations will likely occur. Buyer demand is still extremely strong, and it appears we may soon see a somewhat uncharacteristic increase in the number of homes coming to the market.

Buyer Demand Remains Strong

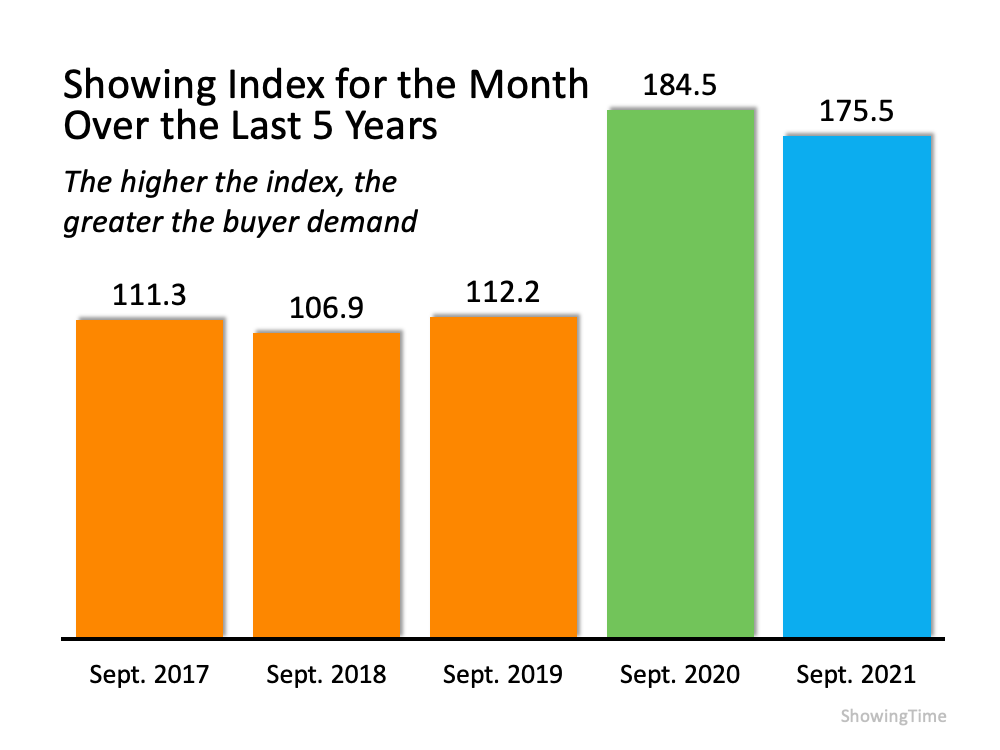

The latest Showing Index from ShowingTime, which tracks the average number of monthly showings on available homes, indicates buyer activity was slightly lower than at the same time last year but much higher than any of the three previous years (see chart below):A report from realtor.com confirms buying activity remains strong in the existing home sales market:

“New housing data shows 2021’s feverish home sales pace broke a yearly record in October, . . . with last month marking the eighth straight month of buyers snatching up homes more quickly than the fastest pace in previous years. . . .”

Buyer activity for newly constructed homes is also very strong. Ali Wolf, Chief Economist for Zonda, recently reported that Stuart Miller, the Executive Chairman of Lennar, one of the nation’s largest home builders, said this about demand:

“There is still a great deal of demand at our sales centers with people lining up and not enough supply.”

The only question heading into this winter is whether the number of listings available could come close to meeting this buyer demand. We may have just received the answer to that question.

Sellers Are About To List – Right Now

Instead of waiting for the normal spring buying market, new research indicates that homeowners thinking about selling are about to put their homes on the market this winter.

Speaking to the release of a report on this recent research, George Ratiu, Manager of Economic Research for realtor.com, said:

“The pandemic has delayed plans for many Americans, and homeowners looking to move on to the next stage of life are no exception. Recent survey data suggests the majority of prospective sellers are actively preparing to enter the market this winter.”

Here are some highlights in the report:

Of homeowners planning to enter the market in the next year:

- 65% – Have just listed (19%) or plan to list this winter

- 93% – Have already taken steps toward listing their home, including working with an agent (28%)

- 36% – Have researched the value of their home and others in their neighborhood

- 36% – Have started making repairs or decluttering

The report also discusses the reasons sellers want to move:

- 33% – Have realized they want different home features

- 37% – Say their home no longer meets their family’s needs

- 32% – Want to move closer to friends and family

- 23% – Are looking for a home office

Data shows buyer demand remains unusually strong going into this winter. Research indicates the supply of inventory is about to increase. This could be a winter real estate market like never before.

Bottom Line

If you’re thinking of buying or selling, now is the time to have a heart-to-heart conversation with a real estate professional in your market, as things are about to change in an unexpected way.

Retirement May Be Changing What You Need in a Home

The past year and a half brought about significant life changes for many of us. For some, it meant entering retirement earlier than expected. Recent data shows more people retired this year than anticipated. According to the Schwartz Center for Economic Policy Analysis, 2021 saw a retirement boom:

“At least 1.7 million more older workers than expected retired due to the pandemic recession.”

If you’ve recently retired, your home may not fit your new lifestyle. The good news is, you’ve likely built-up significant equity that can fuel your next move. According to the latest Homeowner Equity Insights report from CoreLogic, homeowners gained more than $50,000 in equity over the past 12 months alone. That, plus today’s sellers’ market, presents a great opportunity to sell your house and address your evolving needs.

You Can Move Closer to the Ones You Love

The 2021 Home Buyers and Sellers Generational Trends report from the National Association of Realtors (NAR) provides a look at the reasons people buy homes. For those reaching retirement age, the number one reason to buy is the opportunity to be closer to loved ones, friends, or relatives.

If you find yourself farther from your loved ones than you’d like to be, retirement and the equity you’ve built in your home may enable you to move closer to the people in your life who matter most.

You Can Find the Right Home for Your Needs

Not only can your equity power a move to a new location, but it can also help you purchase the right size home. Lawrence Yun, Chief Economist at NAR, says many homebuyers 55 and older choose to downsize – or buy a smaller home – when they make a purchase:

“Clearly from the age patterns, young people want to upsize, and the older generation is looking to downsize. . . .”

Whatever your home goals are, a trusted real estate advisor can help you to find the best option for your situation. They’ll help you sell your current home and guide you as you buy your next one while you move into this new phase of life.

Bottom Line

If you’ve recently retired and your needs are changing, you’re not alone. Let’s connect so you can get a better sense of how to find a home that will match your situation.

Mortgage rates climb back up, to 3.10%

The 30-year fixed-rate mortgage increased 12 basis points in one week to 3.10%, shows Freddie Mac

November 18, 2021, 10:00 am By Flávia Furlan Nunes

Mortgage rates strongly increased above 3% in the week ending November 18, according to the latest Freddie Mac PMMS mortgage report.

The 30-year fixed-rate mortgage hit 3.10%, up 12 basis points from 2.98% the week prior. A year ago at this time, the average 30-year fixed-rate loan averaged just 2.72%.

Sam Khater, Freddie Mac’s chief economist, said the combination of rising inflation and consumer spending is driving mortgage rates higher. “Shoppers looking to buy a home are fueling strong demand while ongoing inventory shortages are not improving in the presence of higher home prices,” he said in a statement.

The survey focuses on conventional, conforming, and fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Economists at Freddie Mac said the 15-year fixed-rate mortgage averaged 2.39% last week, up from 2.27% the week prior. It’s also higher than it was a year ago, at 2.28%. Meanwhile, the five-year ARM dropped slightly to 2.49%, down three basis point from last week. A year ago, 5-year ARMs averaged 2.85%.

Mortgage rates tend to move in concert with the 10-year Treasury yield, which reached 2% on Nov. 15, up from 1.89% a week before.

The increase in rates is impacting mainly refi activity. Refinance mortgage loan applications dipped 31% year-to-year on the week ending Nov. 12, according to the Mortgage Bankers Association (MBA). By contrast, purchase applications declined 6% in the same period.

Joel Kan, associate vice president of economic and industry forecasting at the MBA, said refi applications decreased for the seventh time in eight weeks, as mortgage rates increased following two weeks of declines. The MBA projects that by the end of 2022, mortgage rates will approach 4%. The trade organization believes the heavy refi activity that drove the market in 2020 and much of 2021 will give way to purchase business over the next two years.

Mortgage rates surge higher as inflation pressures grow

Last Updated: Nov. 18, 2021 at 12:15 p.m. ETFirst Published: Nov. 18, 2021 at 10:14 a.m. ETBy Jacob Passy2

A boost in the number of homes listed for sale could be a silver lining for buyers facing an affordability crunch

The benchmark interest rates for home loans jumped back above 3% as inflation-related concerns prevailed.

The 30-year fixed-rate mortgage averaged 3.1% for the week ending Nov. 18, up 12 basis points from the previous week, Freddie Mac FMCC, -2.93% reported Thursday.

The 15-year fixed-rate mortgage also increased by 12 basis points to an average of 2.39%. The 5-year Treasury-indexed adjustable-rate mortgage averaged 2.49%, down four basis points from the previous week.

“The combination of rising inflation and consumer spending is driving mortgage rates higher,” Freddie Mac chief economist Sam Khater said in the report.

This week’s increase could be a sign of what’s to come further down the road. The most recent data on retail sales was strong in spite of record-breaking price increases, which suggests that the economic recovery from the pandemic continues to have momentum, said Paul Thomas, vice president of capital markets at Zillow Z, +0.78% ZG, +1.41%.

“If the economic recovery holds, this continuing inflation trend may increase the probability of the Federal Reserve instituting several rate hikes in 2022,” Thomas said, adding that in the near term supply chain-related issues could put upward pressure on interest rates.

For home buyers, the increase in mortgage rates comes at a time when home prices continue to rise at a steady pace. But marginal relief may be in sight.

Survey data from Realtor.com showed that the share of existing homeowners who plan to sell their homes within the next year has increased from 10% this spring to 26% this fall. Should these homeowners follow through with their plans, that could added a much needed boost of supply to the housing market. Buyers would then have more options, and the pace of home-price growth could slow a bit.

“We have seen an uptick in new listings over the last two weeks, and that has helped keep price growth in check,” said George Ratiu, manager of economic research at Realtor.com. “However, demand from buyers continues to be strong, keeping inventory moving quickly, especially for well-priced homes.”

Supply-Side Disruptions Push Single-Family Production Down in October

Filed in Economics, Material Costs, Multifamily on November 17, 2021

Single-family housing production lagged in October due to supply-chain effects for materials and ongoing access issues for labor and lots. Overall housing starts decreased 0.7% to a seasonally adjusted annual rate of 1.52 million units, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau.

The October reading of 1.52 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months. Within this overall number, single-family starts decreased 3.9% to a 1.04 million seasonally adjusted annual rate, and are up 16.7% year-to-date. The multifamily sector, which includes apartment buildings and condos, increased 7.1% to an annualized 481,000 pace.

Due to supply-chain effects, there are 152,000 single-family units authorized but not started construction— up 43.4% from a year ago.

“The rising count of homes permitted but that have not yet started construction is a stark reminder to policymakers to fix the supply chain so that builders can access a steady source of lumber and other building materials to keep projects moving forward,” said NAHB Chairman Chuck Fowke.

“Single-family permit data has been roughly flat on a seasonally adjusted basis since June due to higher development and construction costs,” said NAHB Chief Economist Robert Dietz. “Demand remains solid but housing affordability is likely to decline in 2022 with rising interest rates.”

On a regional and year-to-date basis (January through October of 2021 compared to that same time frame a year ago), combined single-family and multifamily starts are 30.2% higher in the Northeast, 10.7% higher in the Midwest, 15.2% higher in the South and 20.4% higher in the West.

Overall permits increased 4.0% to a 1.65 million unit annualized rate in October. Single-family permits increased 2.7% to a 1.07 million unit rate. Multifamily permits increased 6.6% to an annualized 581,000 pace.

Looking at regional permit data on a year-to-date basis, permits are 14.4% higher in the Northeast, 17.2% higher in the Midwest, 20.4% higher in the South and 23.0% higher in the West.

Access more housing economics data and analysis at nahb.org.

Sellers: You’ll Likely Get Multiple Strong Offers This Season

Are you thinking about selling your house right now, but you’re not sure you’ll have the time to do so as the holidays draw near? If so, consider this: even as the holiday season approaches, there are plenty of buyers out there, and they really want your house. Here’s why selling this winter is a win for you.

Today’s buyers are still dealing with a limited number of homes for sale. Thanks to continued low inventory, those buyers are competing with one another for their dream home. And when that happens, if your house is one of the few on the market, it will rise to the top of the pool – and it will be worth it.

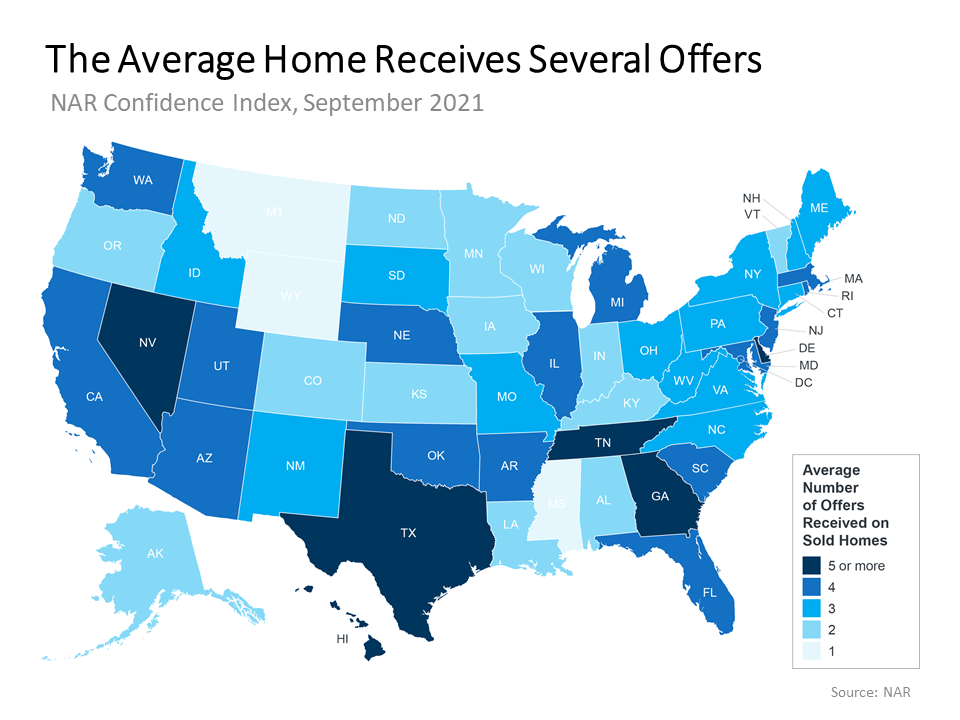

According to the latest data from the National Association of Realtors (NAR), the average seller received 3.7 offers on their house in September. For a view into what’s happening at the state level, take a look at the map below:Nationwide, the average seller today is getting nearly four offers. That number is significant because it means you’ll likely have multiple offers to pick from if you sell your house this season. To put things into perspective, no matter where your state falls, remember that you really only need one good offer to close the deal.

Any offer you receive will likely be from a highly motivated buyer who’s doing everything they can to beat the competition. The stakes for buyers are high. They’ve been looking for a house and they want to lock in their dream home before prices and mortgage rates rise further next year. Chances are, they’ll get creative with the terms of their offer, which could include waiving contingencies and offering over the asking price – both of which are great news for you.

If you’re on the fence about when to sell, remember your house is a hot commodity this season. As other sellers take a break for the holidays with plans to re-list their homes in the new year, you can put your house in front of motivated buyers by making your move today. That means your house will be the center of attention, and likely the center of a bidding war too.

Bottom Line

Selling now gives you even more opportunity to win big as buyers compete for your house in today’s market.

4 Things Every Renter Needs To Consider

As a renter, you’re constantly faced with the same dilemma: keep renting for another year or purchase a home? Your answer depends on your current situation and future plans, but there are a number of benefits to homeownership every renter needs to consider.

Here are a few things you should think about before you settle on renting for another year.

1. Rents Are Rising Quickly

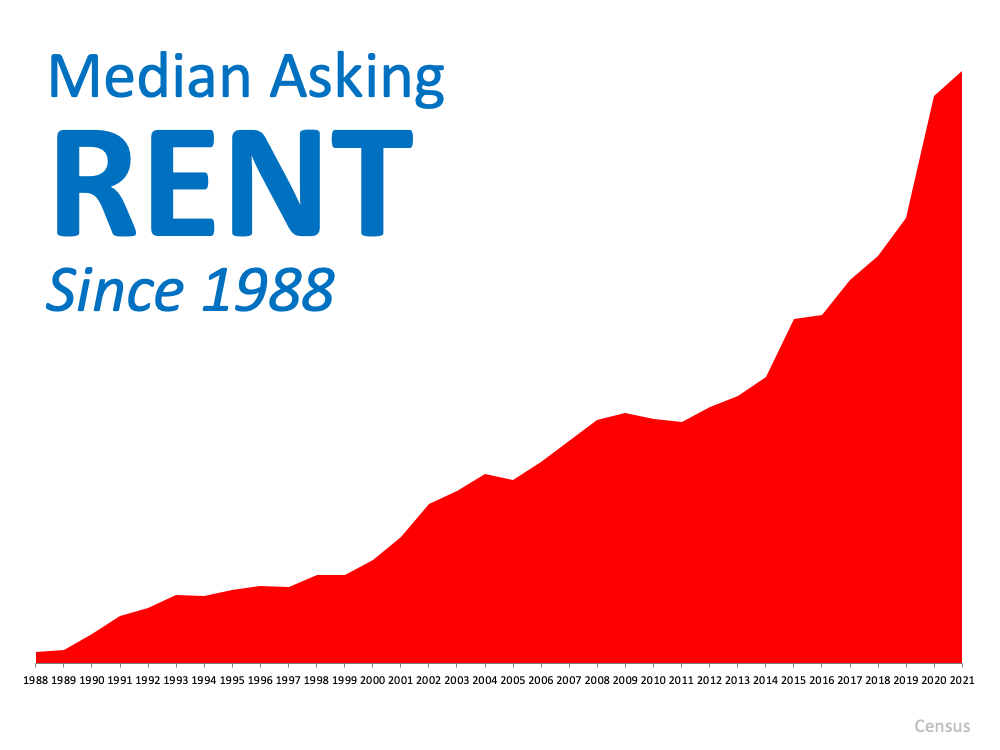

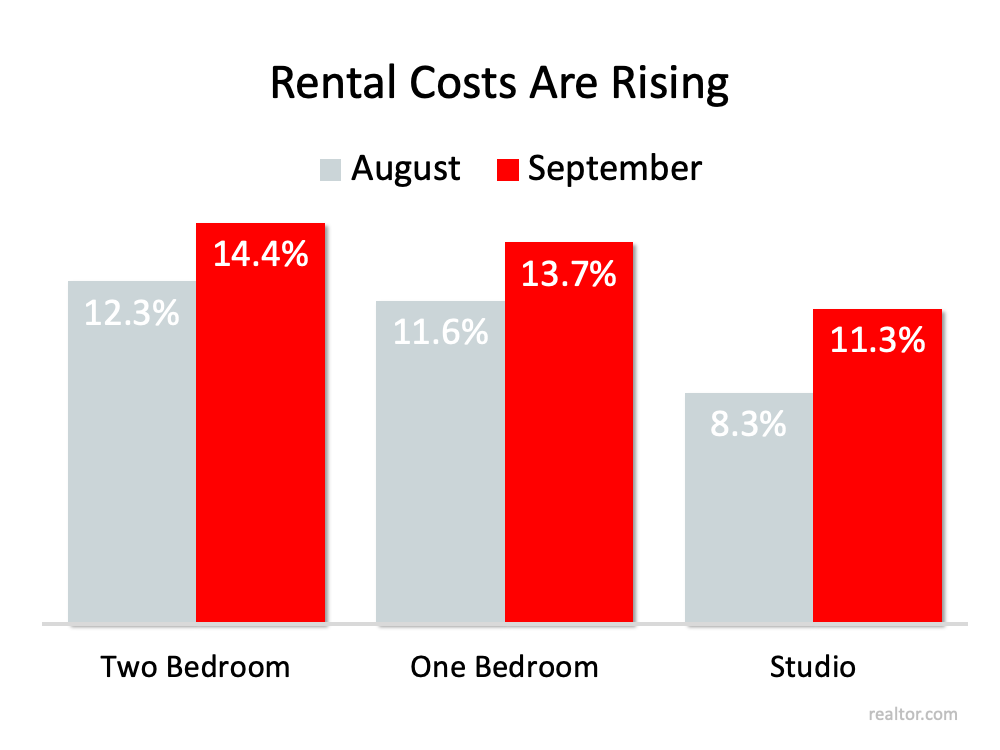

Rent increasing each year isn’t new. Looking back at Census data confirms rental prices have gone up consistently for decades (see graph below):If you’re a renter, you’re faced with payments that continue to climb each year. Realtor.com recently shared the September Rental Report, and it shows price increases accelerating from August to September (see graph below):As the graph shows, rents are still on the rise. It’s important to keep this in mind when the time comes for you to sign a new lease, as your monthly rental payment may increase substantially when you do.

2. Renters Miss Out on Equity Gains

One of the most significant advantages of buying a home is the wealth you build through equity. This year alone, homeowners gained a substantial amount of equity, which, in turn, grew their net worth. As a renter, you miss out on this wealth-building tool that can be used to fund your retirement, buy a bigger home, downsize, or even achieve personal goals like paying for an education or starting a new business.

3. Homeowners Can Customize to Their Heart’s Content

This is a big decision-making point if you want to be able to paint, renovate, and make home upgrades. In many cases, your property owner determines these selections and prefers you don’t alter them as a renter. As a homeowner, you have the freedom to decorate and personalize your home to truly make it your own.

4. Owning a Home May Provide Greater Mobility than You Think

You may choose to rent because you feel it provides greater flexibility if you need to move for any reason. While it’s true that selling a home may take more time than finding a new rental, it’s important to note how quickly houses are selling in today’s market. According to the National Association of Realtors (NAR), the average home is only on the market for 17 days. That means you may have more flexibility than you think if you need to relocate as a homeowner.

Bottom Line

Deciding if it’s the right time for you to buy is a personal decision, and the timing is different for everyone. However, if you’d like to learn more about the benefits of homeownership, let’s connect so you can make a confident, informed decision and have a trusted advisor along the way.